Roundup: Misconceptions About Bitcoin's Performance as a Store of Value

Zack Morris | Research Analyst

Aug 15, 2024

Bitcoin as a Store of Value

Every time there is a volatility event in global financial markets, such as last Monday’s 12.4% crash in the Nikkei 225 (which we covered in depth last week), and bitcoin falls more than most other assets, some try to make the point that bitcoin is empirically failing in its promise to be a store of value. They argue that it behaves more like triple-leveraged NASDAQ than it does gold, the asset it is so often compared to.

During 2022, when inflation was running at a 40-year high of 9% and bitcoin was crashing, people said that it had failed to work as protection against inflation. But what they fail to mention or consider is that gold, an asset with a 2,000 year history of being a good store of value and protection against inflation, also suffered a peak-to-trough drawdown of 17%.

And in 2008 during the GFC, before bitcoin was invented, gold, the canonical “safe-haven” asset, fell 33% … before rebounding 180% over the next three years as quantitative easing was introduced and the dollar was debased.

So what is going on here?

Did 2008 or 2022 invalidate gold’s two-thousand year track record? Of course not. Nor did 2022 or August 5, 2024 invalidate bitcoin’s now 15 year track record. In all of these instances, more variables are at play, and a more nuanced discussion of what actually does drive the price of bitcoin and other assets, over various time periods, gets us closer to a more complete understanding of how bitcoin will perform in various types of acute, or slow-rolling, financial system or market crises.

Zoom Out

Being a “store of value” implicitly means considering the long-term. If you’re fortunate enough to live in a jurisdiction with fiat money that is not suffering from hyperinflation, storing value from today to tomorrow is not a concern. Storing value across years and decades is the concern. As such, store-of-value assets should have their performance measured across years and decades (or, economic cycles), not days and weeks. Oftentimes, disagreements in financial markets can be boiled down to a difference in time horizon.

In a highly leveraged global economy, such as we have, there is not enough fiat money to repay all the fiat denominated debts. The world is short of money, like being short a stock.

When you short a stock, you borrow it and need to pay it back at some point. When you’re “short” fiat money (i.e. you have debts), you borrow it and need to pay it back at some point. It is the same concept.

Everyone once in a while there is a short squeeze on fiat money. This can happen for any number of reasons. Banks can tell borrowers that they’re not going to refinance loans because they doubt the borrower’s ability to repay, and borrowers must come up with the money to repay their loans. Brokers can tell their clients that the value of the assets securing their margin loans has fallen to unacceptable levels, and they must either post more collateral or repay the loans. This is a margin call.

No matter the precise details, it is all fundamentally the same thing: a reduction in the amount of available credit in the economy. When loans must be repaid, borrowers must raise cash to cover their short money positions. This is effectively your “short-squeeze” on fiat.

What does a short squeeze on fiat, the unit of account for everything else, look like? It looks like a drawdown in all other fiat-denominated assets. Including bitcoin.

This is what happened in Japan last week. Traders had borrowed a lot of money, and all of a sudden either decided to or were forced to repay the money they had borrowed. This created a short squeeze on fiat (specifically, Japanese yen), which made all fiat-denominated assets fall in price, in fiat terms. Including bitcoin.

Like a short-squeeze on a stock, these short squeezes on money tend to be short-lived. Call them acute financial or market crises. They are also negative liquidity crises. Think of “liquidity” as the total amount of money sloshing around the global economy, looking for a home. Or, more precisely, global M2 money supply. In a short squeeze on money, money is raised from every available place (by fire-selling assets, for example) to cover shorts (repay debts). So, during these events, there is not enough available money in the system.

Bitcoin, Like All Other Assets, Is Sensitive to Liquidity

Think about it. If the price of everything is denominated in fiat, and the supply of fiat is elastic, then the price of everything should rise when there is more supply of fiat, and should fall when there is less supply of fiat, everything else equal.

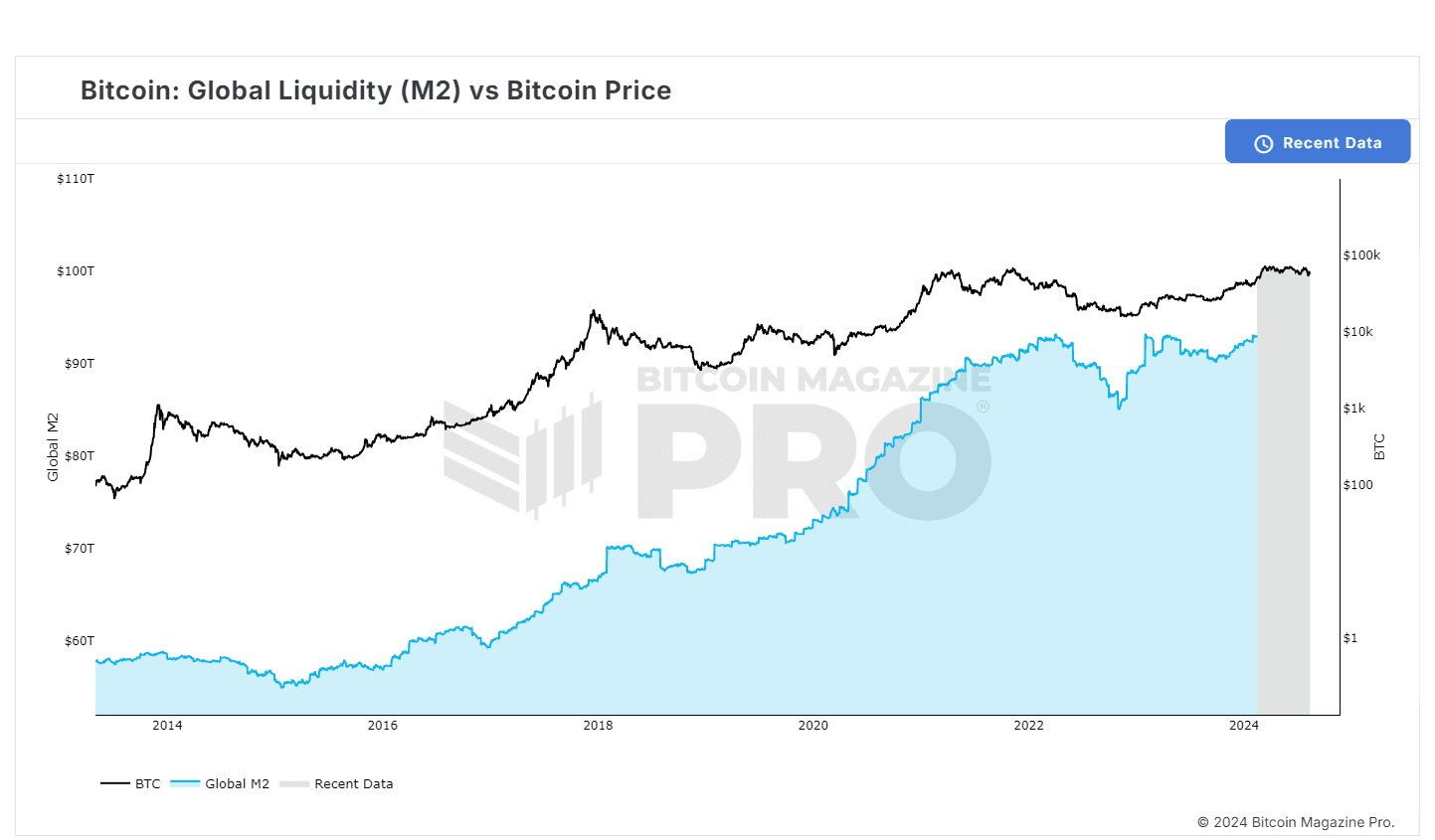

See this chart overlaying the price of bitcoin against global M2, in dollars:

source: Bitcoin Magazine

You can see how sensitive the price of bitcoin is to global liquidity. Of course, over the decade shown on the chart, bitcoin rose by 498x while global liquidity rose “only” 60%, so it is not as if there is a 1:1 relationship here. But, in general, the price of bitcoin will perform well in a pro-liquidity environment and poorly in a negative-liquidity environment.

As such, since most acute market crises are negative-liquidity events, so long as we live in a fiat-denominated world we can expect bitcoin to perform poorly in terms of price during those events. This does not mean whatsoever that bitcoin fails as a store of value.

Again, think about it: we need to store value in something other than fiat money because the supply of fiat money is always growing over time and thus losing its purchasing power over time. If the supply of fiat were constant, then it would store value just fine! And we wouldn’t need to search for other store-of-value assets.

But that is not the world we live in.

As you can see on the chart, there are relatively brief periods of time where global M2 does contract, such as 2022 when central banks were tightening monetary policy to combat inflation. This is why bitcoin performed poorly in 2022. But that is not to say it did not protect investors from inflation.

That inflation was caused, at least in part, by the dramatic increase in global M2 in 2020-2021, a period during which the bitcoin price increased by about 570%. I would say it protected investors from the oncoming inflation admirably, and didn’t just maintain purchasing power through the cycle, but increased it significantly.

I think a better way to think about bitcoin is that it will more directly protect you from monetary debasement (i.e. growth in global M2), rather than inflation. Of course, the two are intimately connected, but they are not quite the same thing. Bitcoin is immediately responsive to debasement, whereas inflation is a lagging side effect, only materializing some period of time after monetary debasement has taken place, and also subject to many other variables.

One of the core aspects of my bitcoin thesis is that every negative-liquidity market crisis must eventually turn into a pro-liquidity market crisis, because the only solution to the problem of not enough money is to print more money, or someone takes a haircut. And haircuts are not a politically palatable solution.

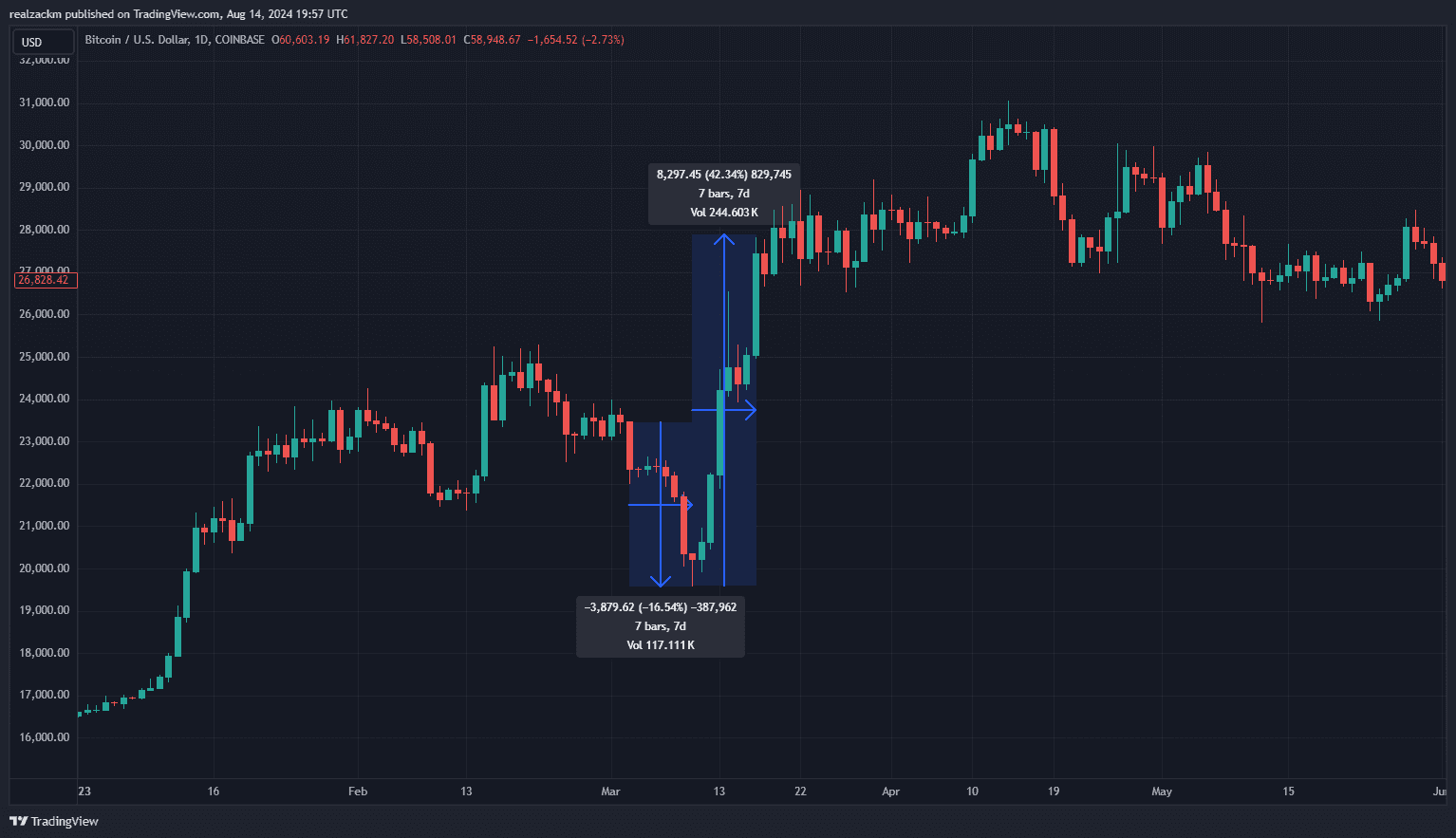

Take the US regional banking crisis in March 2023 set off by Silicon Valley Bank. Silicon Valley Bank did not have enough assets to cover their liabilities, and the bank went bust. Left alone, this is a negative liquidity crisis as money gets destroyed — depositors who thought they had money in their bank accounts suddenly don’t, and are poorer for it. But what happened is the Fed and the FDIC created new money to cover the shortfall and make depositors whole. After all, the only solution for not enough money is to print more money, or someone takes a haircut.

Bitcoin instantly responded to the crisis-averting injection of liquidity. After falling 17% in the week culminating in the bust of SVB, it rebounded by 42% in the following week after officials made it clear that would make depositors at the failed bank whole.

What happened in the span of two weeks in March 2023 was a microcosm of what happened in the span of six months during 2020: an acute short-squeeze on dollars — a deleveraging — accompanied by a fire sale of assets, stymied and solved by the creation of more dollars.

Through both events, and through the events of last week, bitcoin has performed exactly as you should expect it to perform.

And in the next market crisis, however severe or wherever it comes from, you can expect bitcoin will initially fall the hardest, until the remedy of more money creation is certain, and then it will rally the hardest.

Imagine a world in which that wasn’t the case. Imagine a market event in which all assets are crashing except bitcoin. Imagine the panic and fomo of the masses when their stocks are tanking, but bitcoin is somehow rocketing higher?

That would signal a shift much more dramatic than anything we’ve seen so far.

So, yes, bitcoin, for the time being, behaves more like triple-leveraged NASDAQ in a crisis than it does gold. That is because bitcoin and stocks are highly liquidity sensitive assets, and gold is less so. Gold is fully monetized; bitcoin is in the early stages of monetizing, and as such is a more volatile asset. In addition to responding to the vagaries of traditional markets, the probability of bitcoin ultimately fulfilling its promise of first being widely adopted as a store of value, and then a medium of exchange, and finally a unit of account is constantly being weighed and reweighed by the market. Small changes in the probability of bitcoin achieving this outcome can, and should, lead to large price volatility when you consider how large bitcoin’s full potential valuation is.

When and why might bitcoin start behaving more like gold and less like a tech stock? Nobody can know for sure. Perhaps one reasonable answer is when it becomes as monetized as gold is.

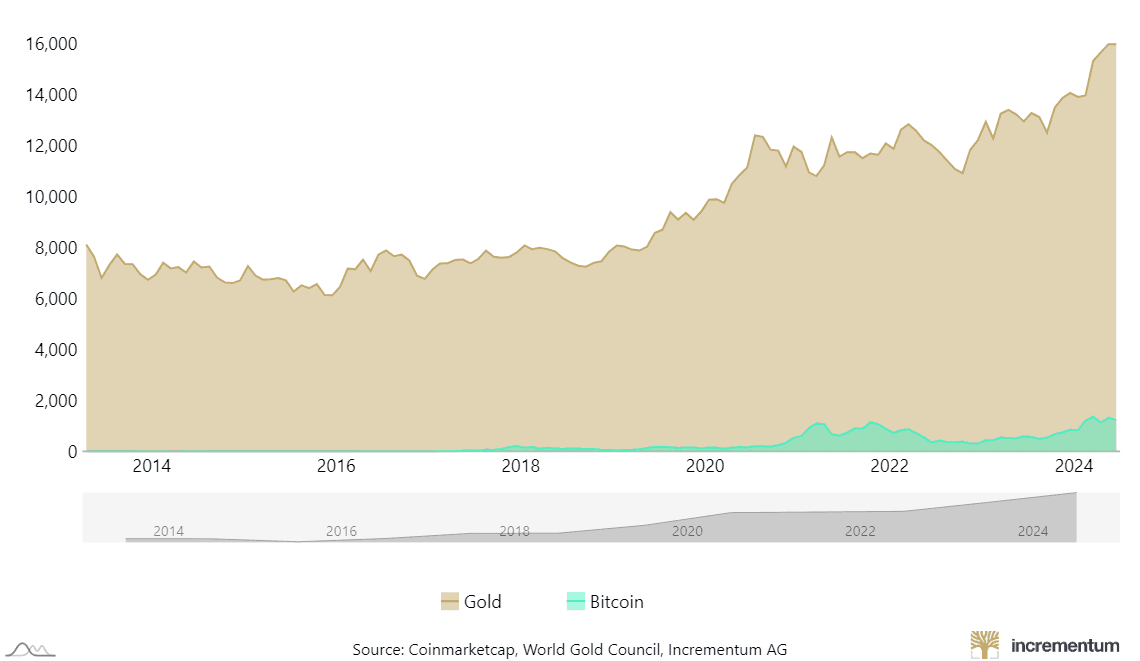

As a reminder, gold is currently at about a $16 trillion market cap while bitcoin is at about $1.24 trillion, a 13x difference.

Maybe if bitcoin achieves a valuation of $845k per BTC it will start behaving more like gold and less like a tech stock.

Until then, expect volatility. Volatility does not equal risk, and volatility does not mean bitcoin is not a good store of value.

source: incrementum

Chart of the Week

source: incrementum

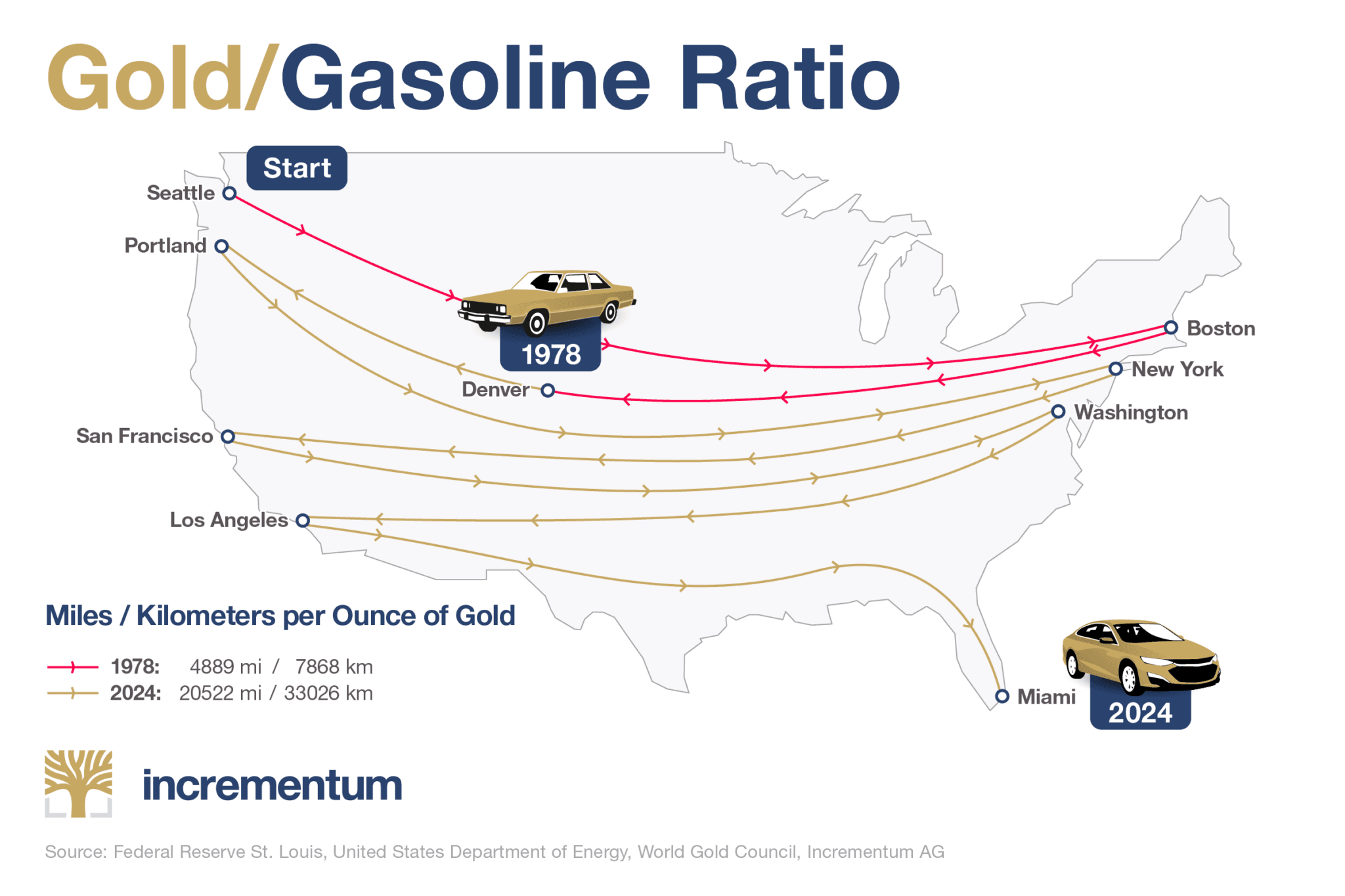

An ounce of gold gets you 15,633 miles further in a car in 2024 than it did in 1978. That’s what comparing a scarce asset (gold) to a non-scarce asset (oil) over a 46 year period looks like. That’s also what technological deflation looks like.

Quote of the Week

“In crises, markets sell what they can, not what they want.

Bitcoin is down because it was the only market open to sell on Sunday night, not because the only fixed supply money we have is now less valuable.

Bitcoin isn’t hedging the broken financial system, it’s replacing it.”

— Jack Mallers, August 5, 2024 on the volatility in bitcoin as the Japanese stock market was crashing on a Sunday night in the US.

Market Update

As of 8/14/2024:

Source: Onramp, Koyfin. 3-, 5-year figures annualized.

Assets continue to bounce back from the swift drawdown last Monday. Bitcoin has led the recovery, up 7.3% in the last week. Stocks have been right behind, led by mega-cap tech and a strong recovery in AI-story stocks. The S&P 500 and NASDAQ have recovered all of their losses since August 1, when a weak employment report initially sent stocks tumbling. The small cap Russell index is still 5% below its August 1 closing level. Gold continues to shine through the current environment, making a new all-time high this week. Oil rose on fears of supply disruptions stemming from Iran’s threats to attack Israel. Bonds continued to fare well as investors digested a second consecutive CPI print that came in below expectations, furthering the case for interest rate cutting cycle.

Podcasts of the Week

The Last Trade E060: Living Through Hyperbitcoinization with Jackson Mikalic

In this episode of The Last Trade, Onramp’s VP of Strategy & Business Development, Jackson Mikalic, joins to discuss leverage & TradFi instability, navigating volatility, nation state adoption, resilience, progress, hope, & more.

The New Frontier E003: Navigating Economic Shifts in the Middle East with Saifedean Ammous

In this episode of The New Frontier, economist Saifedean Ammous explores the benefits of monarchies and how they contribute to the Middle East’s evolving economic landscape. He delves into the region’s shift away from oil dependency, discussing the strategies behind economic diversification. Additionally, Saifedean examines the intersection of Austrian economics with Islamic finance, providing unique insights into how these frameworks can shape the future of the region’s financial systems.

Subscribe to Onramp MENA’s YouTube channel to catch new episodes of The New Frontier podcast!

Wake Up Call (8.12.24): Sander Read & Corey Roun from Lyons Wealth Management

Wake Up Call is a weekly show that will be streamed live on LinkedIn every Monday morning. To catch the premier of each episode, follow Onramp’s LinkedIn page and add Wake Up Call events to your calendar. Hosted by Mark Connors, Onramp’s Head of Global Macro Strategy, and Rich Kerr, Onramp’s President of Managed Wealth, this show seeks to provide financial professionals the “wake up call” they need, prompt them to have an open mind with respect to bitcoin, rethink their prior assumptions, become more educated on the topic, and learn from others who are already farther down this path.

Closing Note

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Find this valuable? Forward it to someone in your personal or professional network.

Until next week,

Zack Morris