Roundup: Fed Pivot & Fiscal Dominance

Zack Morris | Research Analyst

Aug 29, 2024

Fed (Finally) Pivots

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on the incoming data, the evolving outlook, and the balance of risks.”

That was the quote during Jerome Powell’s speech last Friday at Jackson Hole that all but guaranteed the beginning of a rate cutting cycle in September and sparked a broad-based asset rally, including bitcoin which rose 7.5% on the remarks up to $65k.

Fed funds futures are now pricing in a 100% chance of a rate cut at the Fed’s September meeting, with a 66% chance of 25 bps and a 34% chance of 50 bps:

source: CME FedWatch

Of course, the market has been over-zealous in pricing in rate cuts since the last “Powell Pivot,” which we wrote about all the way back in December of last year.

Sometimes it’s fun, and insightful, to go back in time and see what the market was saying. Here is what that same forecast looked like after the Fed’s December 2023 meeting, when Powell first suggested cuts may be on the table:

source: CME FedWatch

As you can see, back then the market was pricing a better than 50/50 chance of a cut in March, and a 100% chance that we’d have at least one rate cut by July 2024, neither of which happened.

Forecasting the future is hard. As an investor or allocator, one’s job is to attempt to see the present clearly, and prepare their portfolio for various possible futures as well as one can.

So, assuming the Pivot has, indeed, finally arrived, what might it mean for the economy, asset markets, and bitcoin?

Many have pointed out that the beginning of a rate cutting cycle has historically been bearish for stocks and the economy, citing some version of this chart:

source: Michael J. Kramer on X

Since 1955, nearly all federal reserve interest rate cutting cycles have been associated with recessions and bear markets, but I would posit the arrow of causality is where the nuance lies.

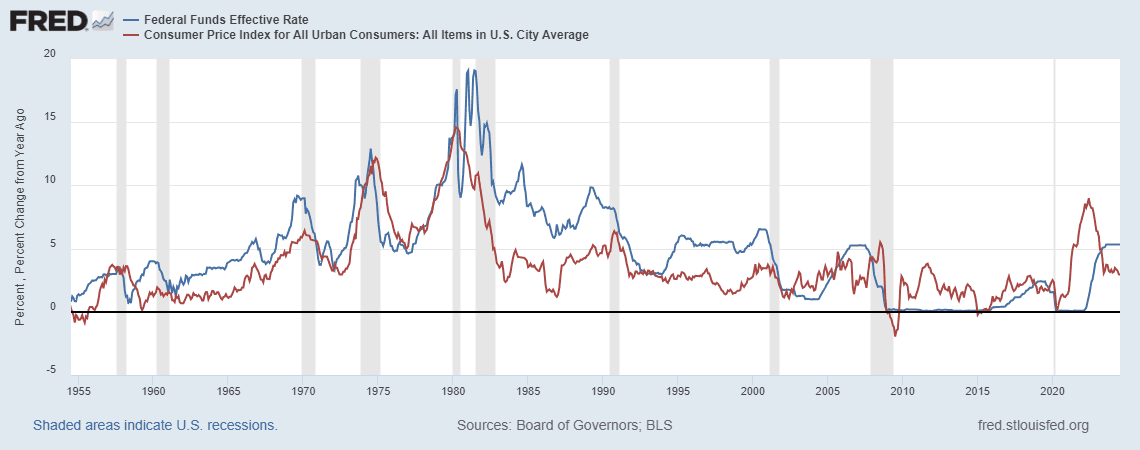

With the exception of Paul Volcker in the early 1980s, in each of these instances where rate cuts were associated with recession, the Fed began cutting before inflation had peaked:

source: FRED

This suggests that the Fed has typically been forced to cut in response to economic weakness, rather than choosing to normalize policy after inflation had come down while the economy was still humming along. Instead of concluding that rate cuts cause recessions and bear markets, one could easily conclude that recessions cause rate cuts and bear markets.

Whether or not we are heading for recession now is up for debate, and we detailed both sides of the argument extensively a few weeks ago here. Again, predicting the future is hard.

Today’s economy has notable differences from the pre-GFC economy, and previous rate-cutting cycles might not have much predictive value given the novel and extraordinary fiscal situation we are now in.

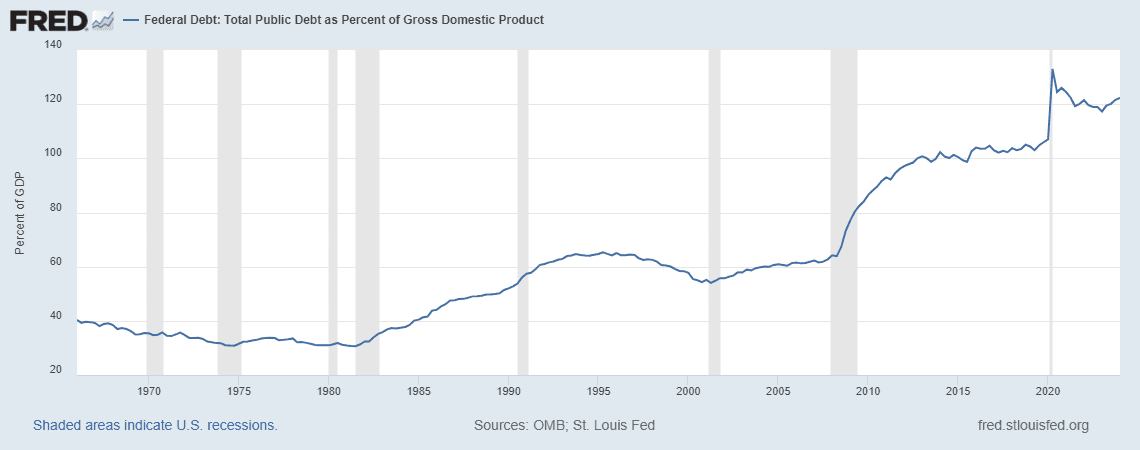

First, debt-to-GDP was between 30-60% for all previous rate cutting cycles, with the exception of COVID. Today it is above 120%:

source: FRED

As Lyn Alden points out, this means that today’s Fed funds rate is actually stimulative to large parts of the economy, as it represents record transfer payments from the public sector to the private sector in the form of higher public debt interest expense. Indeed, interest expense now exceeds military spending and is a large contributor to today’s record fiscal deficits.

These economic conditions — high (>100%) debt-to-GDP, large (>5%) fiscal deficits, high (>5%) interest rates — have never been present in the US in the past. Record debt-to-GDP and fiscal deficits could be a factor for why the US economy was resilient in the face of the rate hiking cycle from 2022-2024 and may not experience a recession as a result of high interest rates this time.

Second, notice how since 1980 every rate cutting cycle has led to a lower low in the Fed funds rate at the bottom of the cycle. Lyn again notes that unless we reach a lower low in interest rates this cycle, spurring a wave of mortgage refinances, the economy similarly might not be very sensitive to rate cuts this cycle, just as it wasn’t very sensitive to rate hikes.

This is fiscal dominance — when fiscal deficits are so large that monetary policy loses its effectiveness.

So if the seemingly imminent rate cutting cycle isn’t likely to impact the US economy except on the margins and in select pockets — such as commercial real estate with floating rate debt that needs to be refinanced, banks who are competing with money market funds for deposits, or new autos which depend on financing rates for affordability — who, and what assets, will it impact?

While monetary policy might not have the same impact on the domestic economy in an era of fiscal dominance, it still has a significant impact on foreign economies and capital flows. As we saw with the yen carry trade unwind, when US rates are 5.5% and Japanese rates are 0% for an extended period of time, imbalances can build up in the system. As interest rates in the US are lowered and catch down to interest rates in the rest of the world, capital is likely to flow out of US assets and into global assets on the margin. Moreover, high rates in the US contributes to a strong dollar, which is an economic headwind for the rest of the world — especially emerging markets with high dollar-denominated debts, like Columbia and Argentina — and a headwind to asset prices. As rates come down, that headwind should turn into a tailwind.

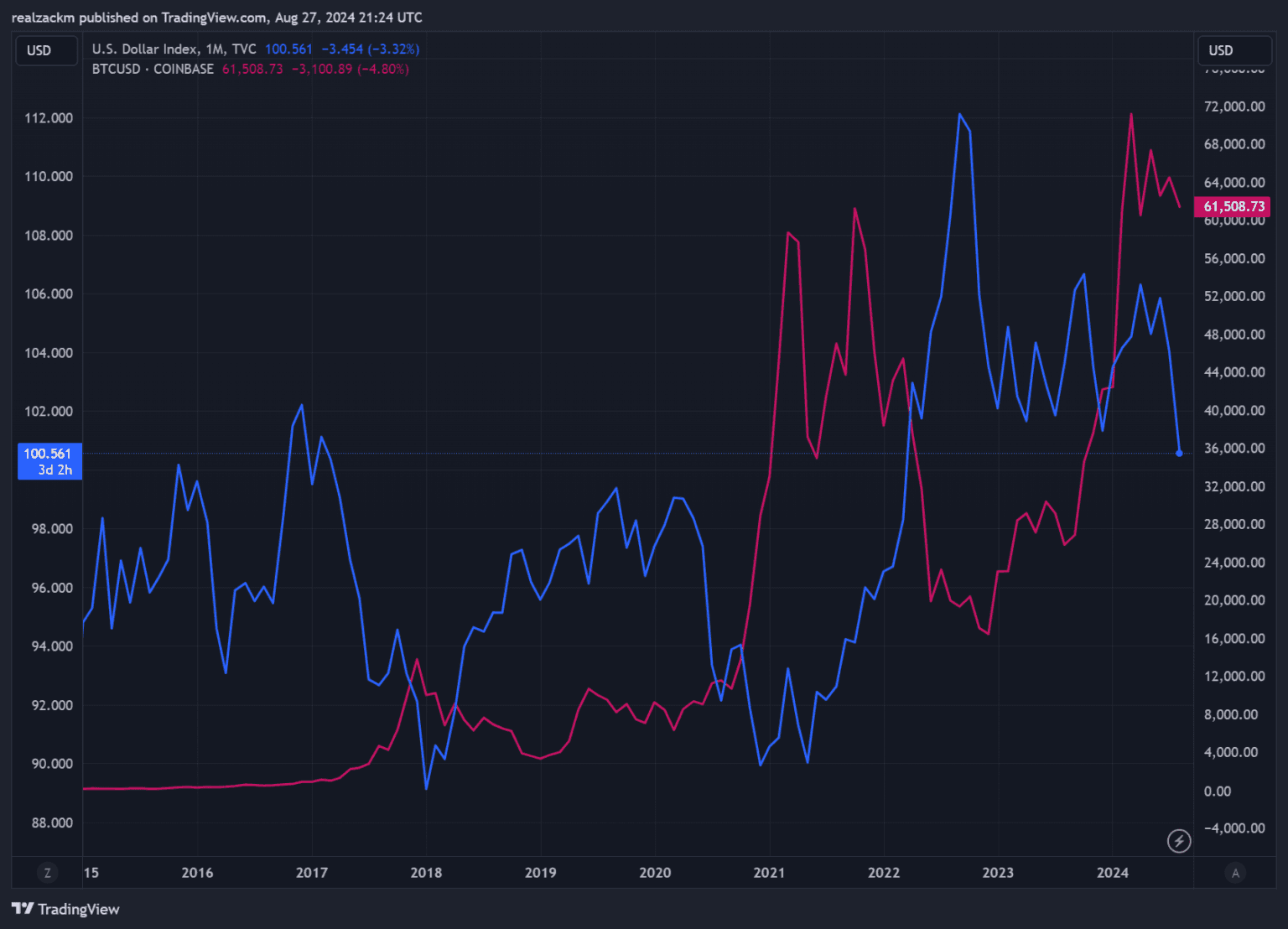

Indeed, in the wake of the yen carry trade unwind, we have already seen the DXY — the dollar index, a measure of dollar strength relative to a basket of foreign currencies — turn lower (blue line):

This has interesting implications for bitcoin.

As the chart shows, bitcoin (red line) has been inversely correlated with the DXY. For as long as bitcoin has existed, every peak in the DXY has kicked off the next bitcoin bull run.

Given the record fiscal deficits in a non-recession economy in the US, past rate cutting cycles might not be prologue for the one we could be entering as it pertains to the economy and the stock market.

But, on the margin, lower rates in the US make dollars less attractive to hold relative to other global assets, including gold and bitcoin.

Instead of watching rates, watch the DXY. If dollar strength has indeed peaked for this cycle and the DXY continues to roll over, the set-up for bitcoin remains constructive.

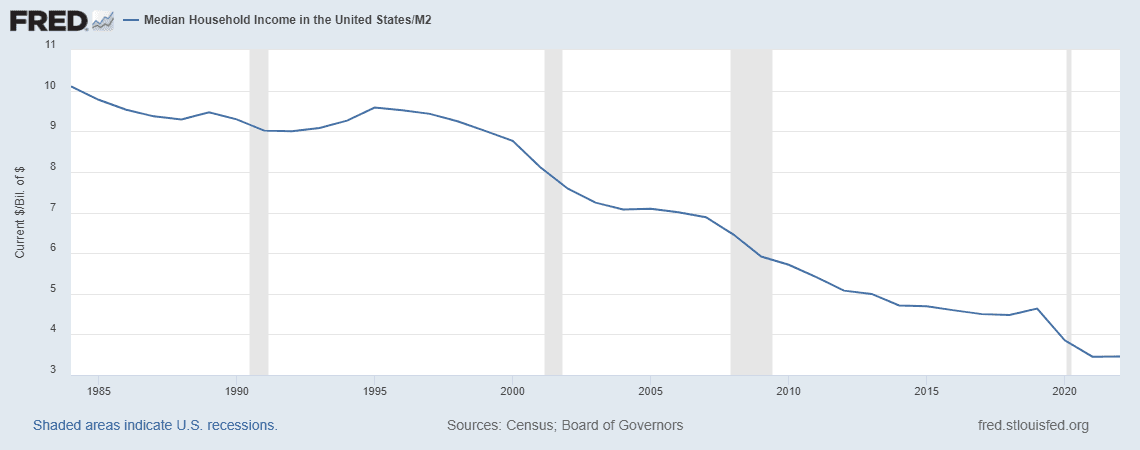

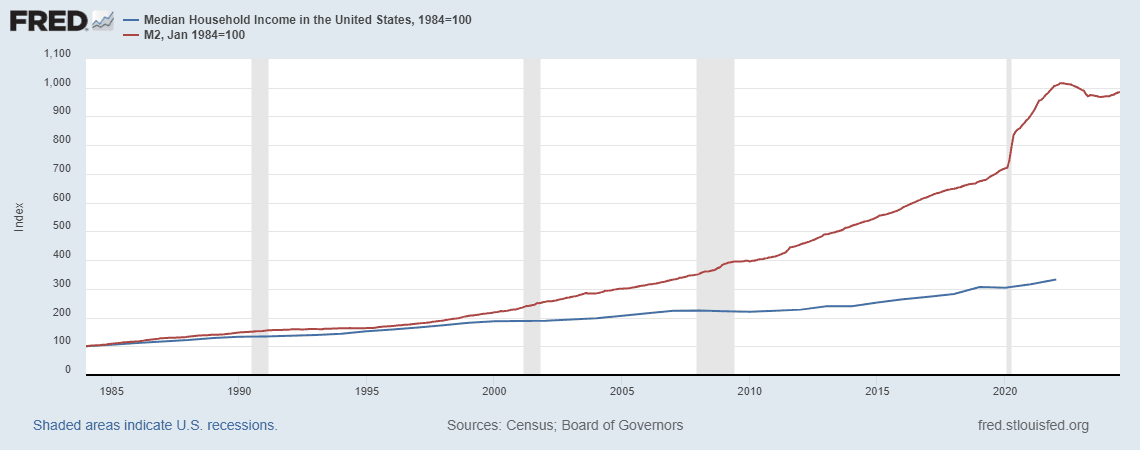

Charts of the Week

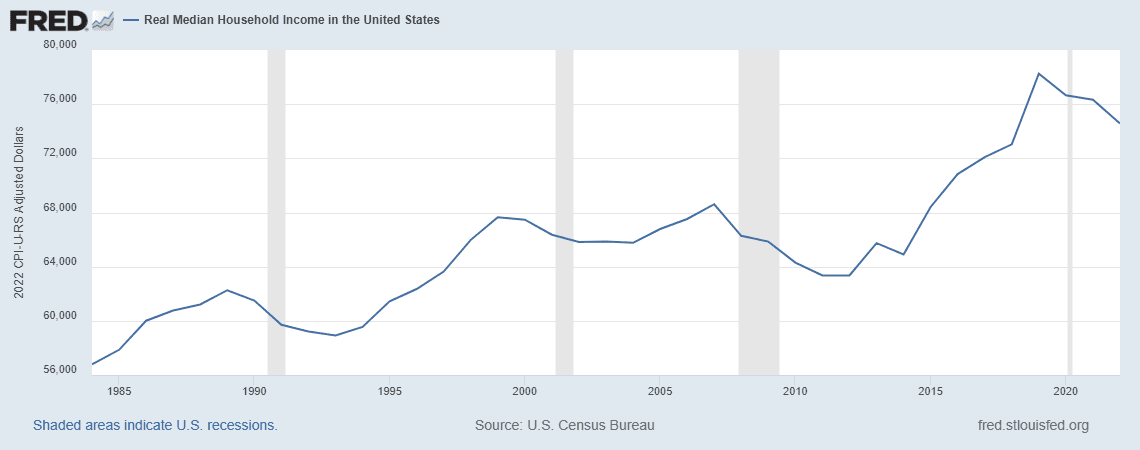

According to FRED data, “real” (CPI-adjusted) median household income is up 31% since 1984. But if you adjust for M2 growth instead of CPI, median household income has declined significantly. Through January 2022, nominal median household income grew 230% since 1984; meanwhile, M2 grew 900% over the same period.

Quote of the Week

“The limits of our knowledge—so clearly evident during the pandemic—demand humility and a questioning spirit focused on learning lessons from the past and applying them flexibly to our current challenges.”

— Jerome Powell, Jackson Hole Economic Symposium, August 23, 2024

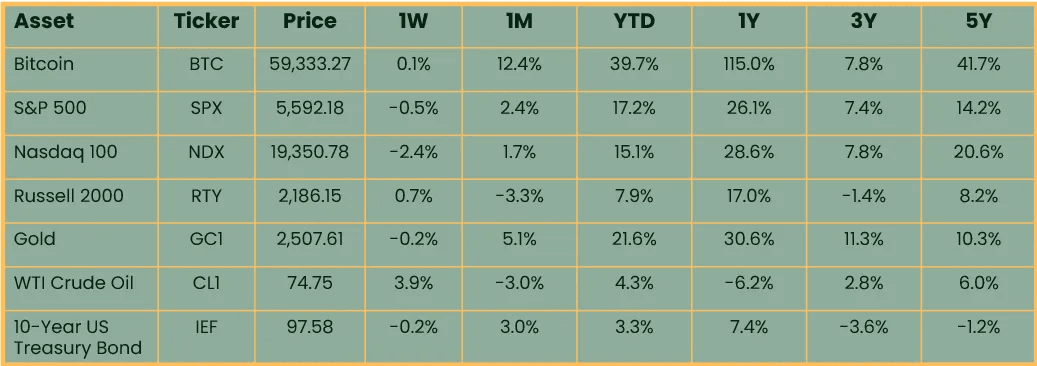

Market Update

As of 8/29/2024:

Source: Onramp, Koyfin. 3-, 5-year figures annualized.

Asset rallied last Friday on Jerome Powell’s dovish comments at Jackson Hole, but gave back those gains in early trading this week. Bitcoin is unchanged over the last week and hovering around the $60k level. NASDAQ was the worst performer as traders were cautious ahead of Nvidia’s earnings report on Wednesday night. Small caps outperformed in equities as they are seen to be the biggest beneficiaries of rate cuts. Gold was flat. Crude rallied 4% on Middle East tensions but is still the worst performing asset over the past year. Treasuries held their recent gains on lower rate expectations.

Podcasts of the Week

The Last Trade E062: The Evolution of Bitcoin Custody with Brian Cubellis & Bradley Chambers

In this episode of The Last Trade, we’re joined by Brian Cubellis, Onramp’s Chief Strategy Officer & Bradley Chambers, Onramp private client & marketing advisor to the firm, to discuss our recently published report “The Evolution of Bitcoin Custody.” Download the full report here. Register to attend our upcoming webinar here.

Final Settlement E012: MENA’s Synergistic Embrace of Bitcoin with Ralph Gebran

In this episode of Final Settlement, Ralph Gebran, Managing Partner of Onramp MENA, joins the pod to discuss innovation in Dubai, bitcoin’s conservative nature, market structure in MENA, synergies btw bitcoin & the region, & more.

Wake Up Call (8.26.24): Paul Scudellari, Founder of RIApex

Wake Up Call is a weekly show that will be streamed live on LinkedIn every Monday morning. To catch the premier of each episode, follow Onramp’s LinkedIn page and add Wake Up Call events to your calendar. Hosted by Mark Connors, Onramp’s Head of Global Macro Strategy, and Rich Kerr, Onramp’s President of Managed Wealth, this show seeks to provide financial professionals the “wake up call” they need, prompt them to have an open mind with respect to bitcoin, rethink their prior assumptions, become more educated on the topic, and learn from others who are already farther down this path.

Closing Note

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Find this valuable? Forward it to someone in your personal or professional network.

Until next week,

Zack Morris