Annual Letter Season

Brian Cubellis | Chief Strategy Officer

Feb 27, 2024

Having spent the bulk of my professional career in the realm of traditional investment management, I have a particular affinity for this time of the calendar year – it is “annual letter” season. This period, spanning from mid-January to early March, is an opportunity for professional investors, specifically portfolio managers, to opine on the happenings of the recently completed year, dissect their fund’s performance, provide LPs with an updated lens into their philosophical stance, and prognosticate on the future.

For my own purposes, while allocating capital on behalf of private banking clients at my prior firm, this exercise of reviewing annual letters from across the investment management space was immensely valuable – it allowed me to assess the perspectives of the broader industry and better contextualize the positioning of investments within our own portfolio. I would compare and contrast the views of fund managers on our platform with the myriad of other investors who would release their annual letters publicly. A consistently reliable repository to track the release of such reports was the Subreddit called SecurityAnalysis – here is the aggregation of this season’s musings: Q4 2023 Letters & Reports.

Despite departing the world of traditional investment management to focus my analytical energy on bitcoin, I still find value in sifting through these letters. If nothing else, the exercise is helpful in triangulating where the notion of bitcoin currently sits in the TradFi zeitgeist. During 2017 and again in 2021, several managers’ letters mentioned bitcoin’s bull market theatrics, albeit in a dismissive manner, referring to tulip bubbles or the asset’s lack of cash flows. Unsurprisingly, the past few years of letters included hardly any mention of the best performing asset of the last decade, as its bear market decline afforded traditional investors the opportunity to once again ignore its existence. While I suspect this dynamic may shift in the coming quarters, bitcoin-related commentary this season was fairly sparse, with a few notable highlights:

Manager: O’Keefe Stevens Advisory

AUM: $326M

Q4 2023 Annual Letter

This annual letter begins with a report card of the manager’s predictions from Q4 2022:

- One of our top 25 holdings gets acquired

- TSLA is a sub $200B market cap by the end of 2023

- Crypto, the final blow

Credit where credit is due, they nailed their first prediction.

(Grade: A-)

As for prediction number two, Tesla ended 2023 with an ~$880B market cap.

(Grade: D)

Prediction number three is where we find our mention of bitcoin. The report card reads as follows:

Crypto becomes far less relevant.

(Grade: B-)

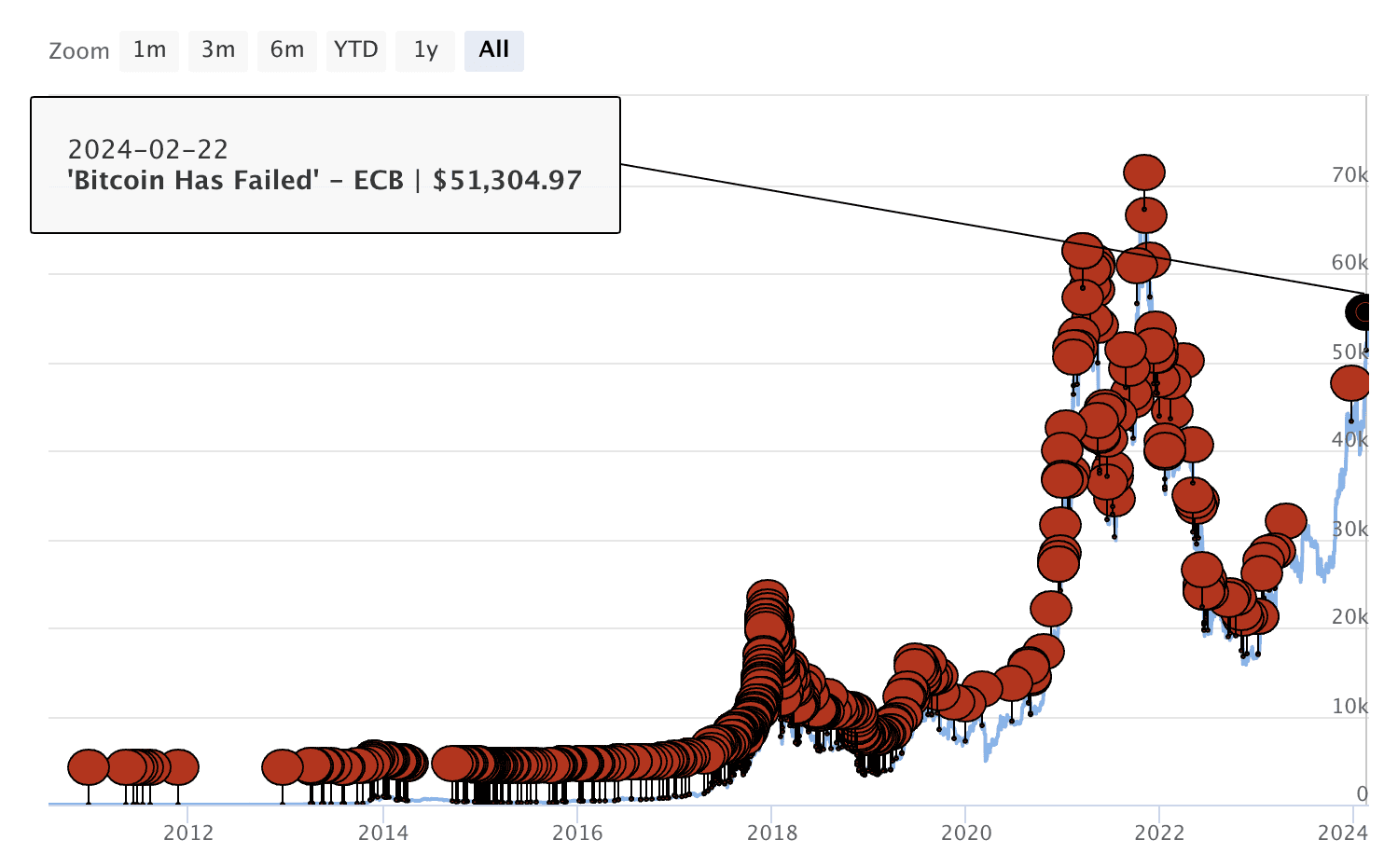

The resilience of a worthless item is incredible. During the year, FTX, the largest crypto exchange, went out of business after the second coming, Sam Bankman Fraud, stole billions of speculator’s capital. In addition, the largest crypto bank, Silvergate, had a bank run and was seized by the FDIC. We still have not found a credible use case for the coins. Until this is the case, we will stick with USD. While the prediction results are unsatisfactory, if we said, TSLA 2024 earnings estimates are down 46%. You’d likely think the stock is not where it is today. Furthermore, if the largest crypto exchange and the most prominent crypto bank went under; you’d predict Bitcoin is at $10,000, not $42,000. While the results are poor, the rationales weren’t far off. In this business, results can outweigh process in the short run; in the long run, process dictates results.

In the wake of FTX’s collapse, the manager presumed the “worthless item” was on its deathbed. Despite bitcoin appreciating ~157% in 2023, ETFs inching towards their eventual approval, and bitcoin miners shifting the narrative around their impact on the environment, the manager generously graded the prediction above as a B-. As of this writing, bitcoin is hovering around $57,000 and while I won’t speak for the rest of “crypto,” bitcoin is far from dead, and arguably more relevant than it’s ever been.

Historical Bitcoin Obituaries

source: 99Bitcoins

Manager: Howard Marks, Oaktree Capital Management

AUM: $189B

Annual Memo: Easy Money

One annual letter that I always look forward to reading is that of Howard Marks, co-founder and co-chairman of Oaktree, and one of the most prolific debt investors of all time. I have immense respect for Howard, had the opportunity to interact with him and his colleagues while at my prior firm, and have always found his writing extremely valuable.

Over the years, Howard’s views on bitcoin have steadily evolved. In 2017, he dismissed the asset, calling it “nothing but an unfounded fad (or perhaps even a pyramid scheme).” Four years later, in 2021, Howard revised his stance by articulating that he had not studied the asset long enough to form an educated opinion. He also noted that he had grown to appreciate the views of those in favor of bitcoin, comparing its properties to gold: “There’s a big argument that [bitcoin is] digital gold, that it has some of the qualities of gold in the sense of being inflation-resistant, and maybe crisis-resistant. But relative to gold, it has advantages. You don’t have to pay to store it, it’s not challenging to send it someplace or move it around, and you can spend it — which you can’t do with gold.”

Fast forward to 2023 and Howard’s understanding had evolved even further in the wake of the US regional banking crisis, stating “It [bitcoin] is an anti-bank play, and the weakness of the bank shows up in the strength of bitcoin, and it’s done very, very well this year.” It is also worth noting that while Howard has never disclosed any personal investments in bitcoin, he has confirmed that his son, Andrew Marks, has had exposure to bitcoin for a number of years. Andrew was a partner at the Marks family office, Freemark Partners, for several years before co-founding TQ Ventures, a tech-focused venture fund, in 2018.

In Howard’s most recent memo, he doesn’t explicitly mention bitcoin. Nevertheless, his poignant commentary on the concepts of easy money, interest rate policy, and resultant malinvestment are remarkably attune to the problems that bitcoin was designed to solve. Howard has rightly identified the ills of the prevailing monetary system and its negative externalities for the broader investment landscape, but has yet to recognize bitcoin as the plausible solution. Howard even evokes the philosophical tenets of one of Austrian Economics’ forefathers, Friedrich Hayek, as he states:

“I love Hayek’s word ‘malinvestment,’ because of the validity of the idea behind it: in low-return times, investments are made that shouldn’t be made; buildings are built that shouldn’t be built; and risks are borne that shouldn’t be borne. People with money feel they must put it to work, since cash yields little or nothing. They drop their risk aversion and, as discussed below, compete spiritedly for lending or investing opportunities with higher potential returns. The investment process becomes all about flexibility and aggressiveness, rather than thorough diligence, high standards, and appropriate risk aversion.”

Beyond his tacit espousal of the merits of the bitcoin thesis, Howard’s most recent memo resonated with me in his exploration of the role of cash in a world of easy money.

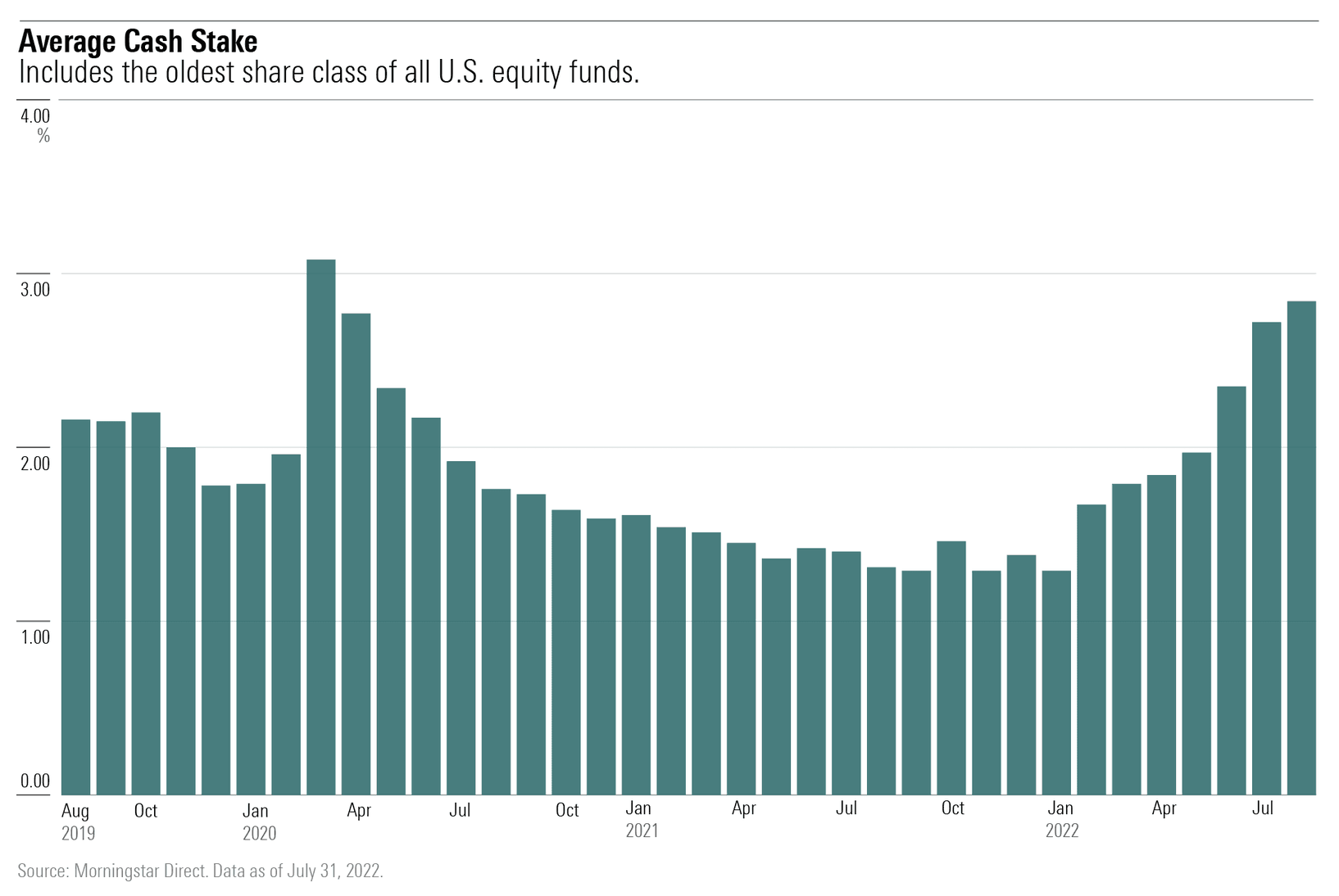

Cash Positioning

Reflecting on my prior analyses during annual letter season, Howard’s musings reminded me that the cash positioning of a given fund manager was always a particularly insightful data point. I viewed the extent to which a given portfolio was allocated towards cash as a useful barometer for the high-level market outlook of a given investor. A portfolio devoid of cash implied a bullish stance, a belief in the continuous appreciation of stocks and growth potential of earnings. On the other hand, a substantial cash position suggested a more cautious or bearish outlook, indicating concerns around rich valuations or uncertain market conditions.

source: Morningstar Direct

From a philosophical perspective, my prior firm believed in the foundational tenets of value investing. In the world of value investing, significant cash positions were not entirely uncommon. For many traditional value investors, the relentless nature of equity returns over the past twenty years occurred against their preconceived notions about markets and valuations. A meaningful cash position was effectively a stance that the “good times” couldn’t keep rolling forever, and that when the proverbial music stopped, they wanted to not only protect their portfolios from the associated downside, but also be positioned to redeploy dry powder as there was blood in the streets.

For this reason, cash positioning was always an intriguing signal for me with respect to the current conviction of a particular manager. Their exposure to cash was the most overt data point in determining their outlook on equity markets, whether they believed the music would keep playing or that valuations were getting excessive. Being fully invested (with near zero exposure to cash) signaled they believed prices still had room to run; they couldn’t afford to be sitting in cash and risk not participating fully in that upside. More meaningful cash positions (in the double digits as a percentage of the portfolio), signaled a more cautious view.

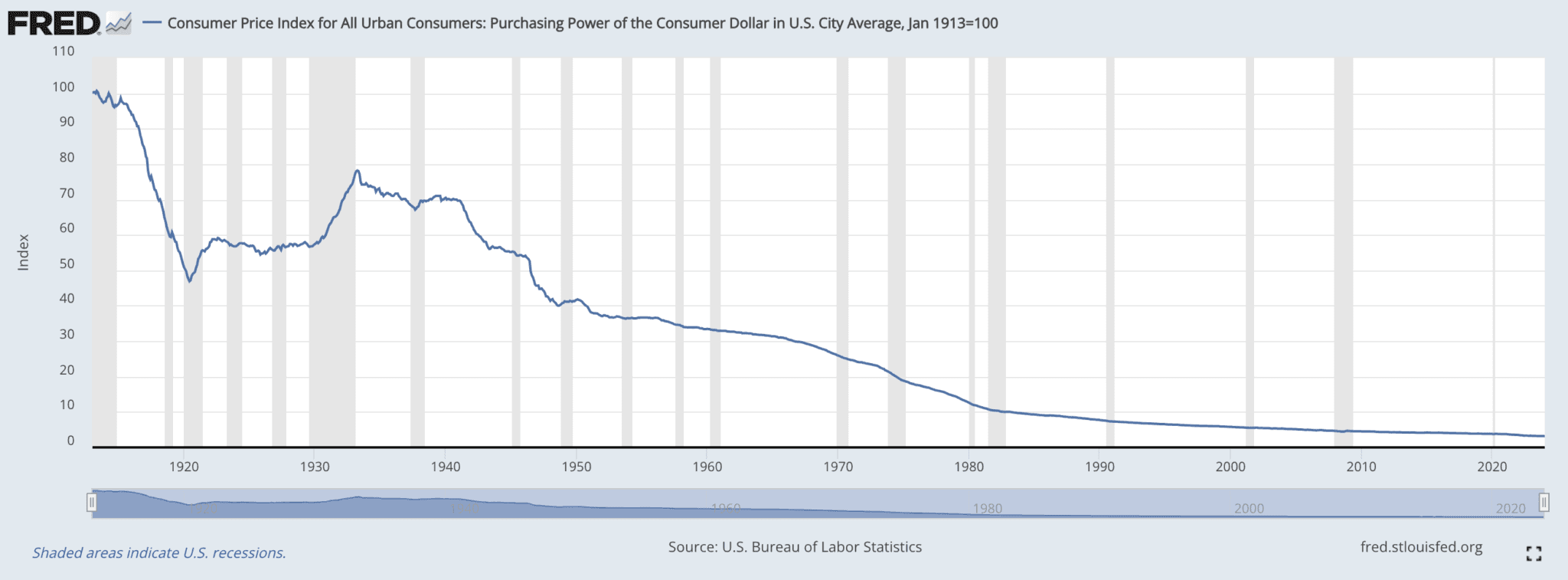

This conventional wisdom posits that cash, as an asset class, represents a safe haven – a bulwark against market fluctuations and a reserve of dry powder ready to be deployed opportunistically. However, I now recognize that this view fails to account for the inherent risks associated with holding cash, particularly in the context of inflation and monetary debasement.

source: U.S. Bureau of Labor Statistics

Upon closer examination, and through my subsequent study of money and bitcoin, it became apparent that holding cash is far from a neutral position. It is, in effect, an active bet against the market’s potential, but even more importantly represents a decision fraught with the silent erosion of purchasing power. Over time, the purchasing power of cash reserves inevitably diminishes, making the strategy of holding cash a tacit acceptance of guaranteed value loss. While specific stocks may experience volatility from time to time, cash steadily erodes in value, subject only to the whims of central bank policy and inflationary pressures. In today’s economic landscape, where central banks wield unprecedented influence over monetary policy, traditional cash holdings in a portfolio context demand a reevaluation.

Bitcoin is a Superior Form of Cash

If portfolio managers were to apply the same level of due diligence in analyzing cash options as they do evaluating stocks, they might recognize the importance of considering the monetary policy of the nation issuing that particular currency. Questions about fiscal deficits, debt sustainability, and foreign demand for a nation’s debt, should inform any decision to allocate towards cash. Yet, all too often, cash is instead treated as a passive, conservative non-action, devoid of the scrutiny applied to other exposures of the portfolio.

In this context, bitcoin emerges as a compelling alternative. As a decentralized form of money immune to government manipulation and debasement, bitcoin offers a differentiated alternative to state-backed fiat currencies. Unlike fiat currencies, which are subject to arbitrary inflation targets and political agendas, bitcoin’s long-term purchasing power is ensured by its programmatic scarcity, enforced by immutable code and social consensus. By allocating a portion of traditional cash holdings to bitcoin, investment managers can transform dormant capital (guaranteed to erode over time) into a dynamic allocation poised for growth, mitigating the inflationary risk inherent in fiat cash holdings while maintaining the strategic liquidity necessary for opportunistic investments.

source: Onramp Terminal

In the wake of spot bitcoin ETF approvals in the US, this theoretical approach to cash positioning is now a more practical possibility. However, as demonstrated by the analysis of this season’s annual letters, the traditional investment management world is still largely oblivious to this ongoing paradigm shift in the monetary order. That said, investors like Howard Marks appear well on their way to understanding the value proposition of bitcoin and may be inching closer to recognizing its role as a superior form of money, or cash. Invariably, some portfolio managers will eventually decide to park some of their excess cash in bitcoin, and when their portfolio outperforms their peers as a result, others may quickly begin to take notice.