4/16/26 Roundup: All-Time Highs, All-Time Fragility

Brian Cubellis | Chief Strategy Officer

Apr 16, 2026

Equity markets are pricing in the best of all possible worlds. The data underneath tells a more complicated story. Sound money was built for exactly that complication.

The S&P 500 closed at a new all-time high on Wednesday, finishing at ~7,022 and surpassing its previous record of ~7,002 set on January 28. The Nasdaq posted its 11th consecutive winning session. The Dow was the only major index that declined.

Consider what those numbers are being asked to price in. An active U.S. military blockade of the Strait of Hormuz. An effective tariff rate of around 11%, the highest since the early 1940s. A Federal Reserve under open political pressure. The Bureau of Labor Statistics reported that the all-items consumer price index rose 0.9% in March alone, pushing the 12-month rate to 3.3%. The IMF raised its global inflation forecast for 2026 to 4.4%, up from 4.1%.

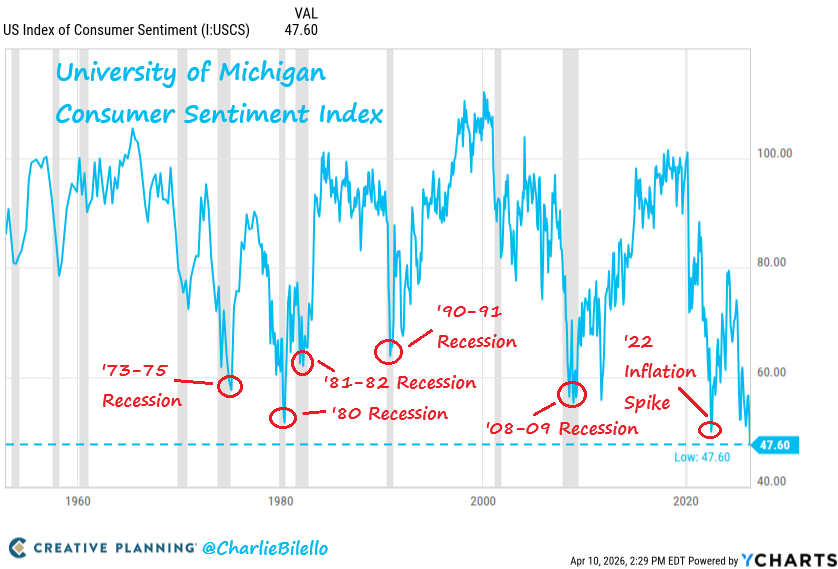

And behind all of it, consumer psychology has broken: year-ahead inflation expectations surged from 3.8% in March to 4.8% in April, the largest one-month increase since April 2025. The University of Michigan Consumer Sentiment Index plummeted to a historic low of 47.6 in early April.

Markets have absorbed all of it. Over the 10 trading sessions leading up to Wednesday, the S&P 500 rose 9.8%, faster than the bounceback after Liberation Day last year and the quickest 10-session run since the post-COVID rebound in April 2020.

The Magnificent Seven led the charge. Since the S&P's low on March 30, a fund measuring only those seven mega-cap tech stocks is up nearly 18%, while a fund measuring the S&P 500 absent them is up about 8%. The gap between what consumers feel and what equity markets are pricing has rarely been wider.

The Illusion of Diversification

The conventional wisdom around owning "the market" rests on a premise that no longer holds: that broad index ownership confers genuine diversification.

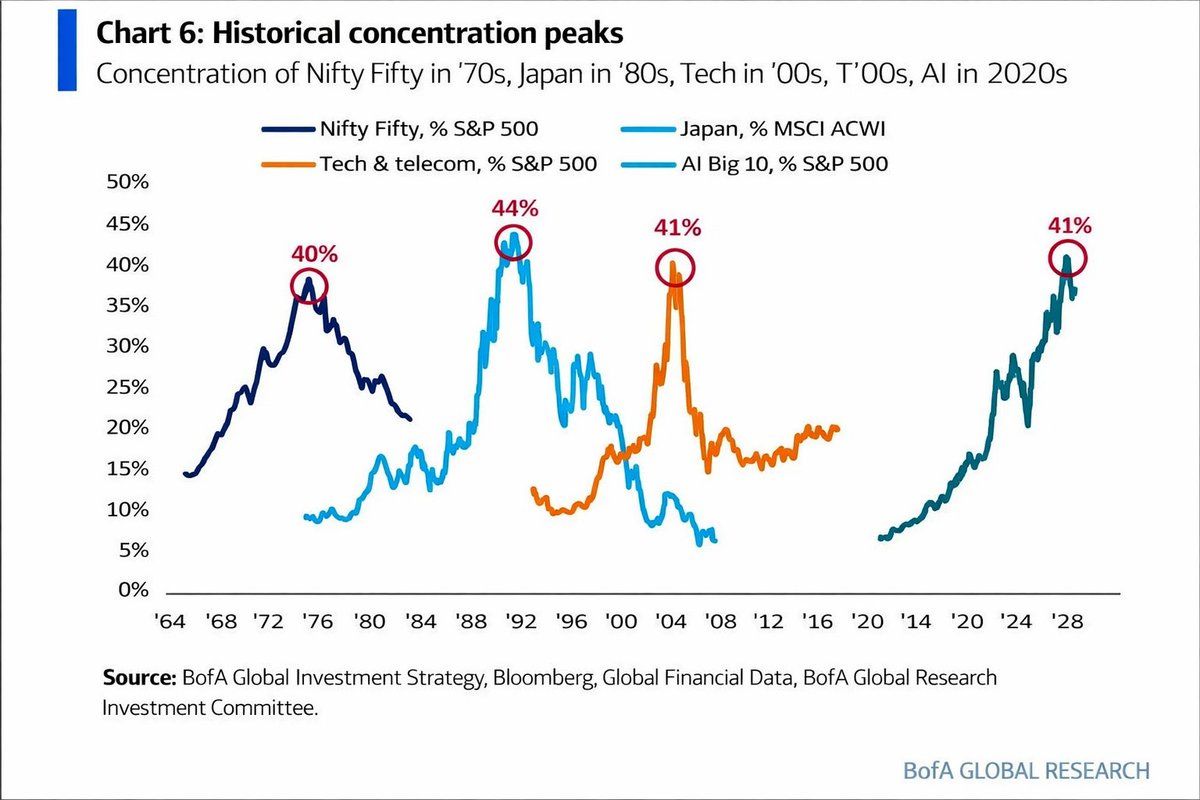

The top 10 companies now make up more than 40% of the S&P 500's total market value, the highest level of concentration since at least 1972. If you invested $1 million in the index today, about $400,000 would be allocated to just 10 companies, while the remaining $600,000 would be spread across the other 490.

A decade ago, that split looked nothing like this. At the end of 2015, the top 10 stocks accounted for about 19% of the S&P 500's weight and roughly 19% of total index earnings, with market value and fundamentals broadly aligned. The top 10 now generate about 32.5% of the index's total earnings while representing 40% of its total market capitalization, trading at meaningfully higher multiples than the rest of the market.

Narrative Over Fundamentals

Equities go up. Measured in dollars over long horizons, the historical record largely confirms this. But the dollar being used to measure those gains has lost most of its purchasing power over the past century.

The money supply has expanded by trillions across successive crises. The fiscal deficit is structural and growing. Every nominal gain printed on a brokerage statement is being quietly discounted by the same policy machinery that made those gains possible in the first place.

This is why equities became the default savings vehicle for most Americans. Holding cash guarantees loss and bonds have failed as inflation hedges across most of the past decade, so flows pile in from every direction: 401(k) contributions, pension allocations, passive index vehicles, retail accounts. Net flows into S&P 500 ETFs reached $4.2 billion in a single week recently, the highest in a month. The machine perpetuates itself.

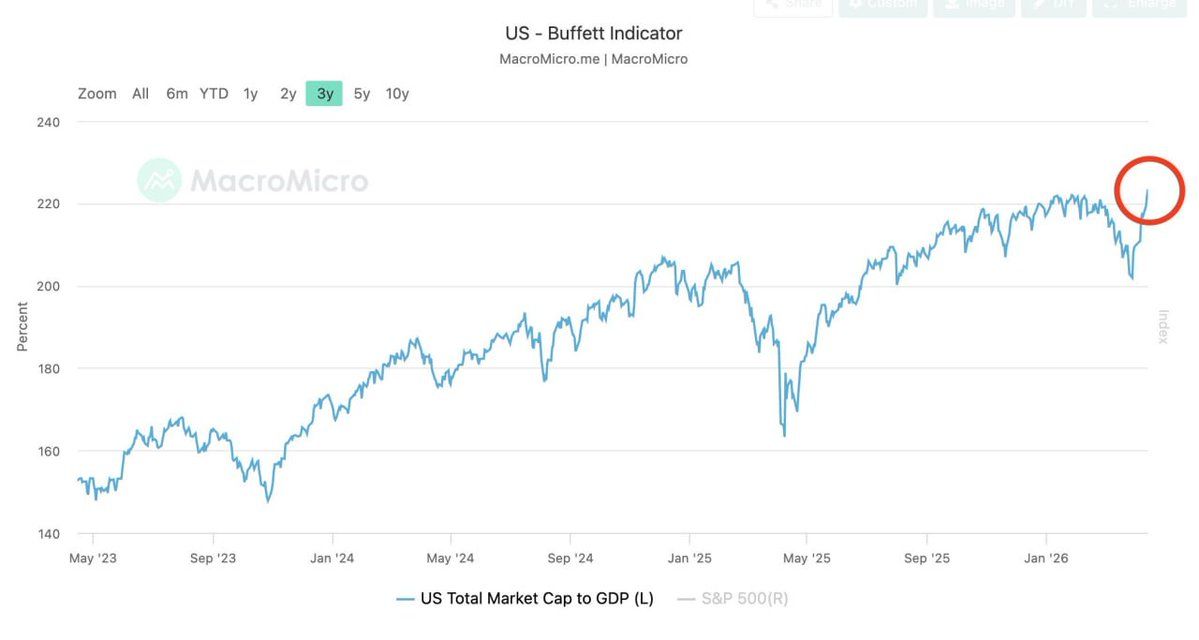

The Buffett Indicator, which measures total market capitalization against GDP, just hit its highest level in history at 223.55%, surpassing even the dot-com peak. Berkshire Hathaway is holding nearly $400 billion in cash, much of it in Treasuries, and now owns more T-bills than the Federal Reserve. When the most celebrated long-term equity conglomerate in history is sitting on the largest cash pile ever assembled rather than deploying it into the market, that is worth pausing on.

Moreover, fundamental risks under the surface haven't changed. Management execution, legal and regulatory exposure, competitive disruption, geopolitical supply chain fragility, and concentration in companies whose AI revenue narratives are still being proven out. Most investors carry none of this in their mental model of what index ownership actually means.

Wednesday offered a perfect example of where the market's attention actually lives. Allbirds, the sneaker brand that peaked at a $4 billion valuation in 2021 and had fallen to roughly $21 million by Tuesday's close, announced it was abandoning footwear entirely, rebranding as NewBird AI, and pivoting to GPU compute infrastructure. The stock closed up 582% on the day. The company has no AI business yet. It has a $50 million convertible financing facility, a stockholder meeting scheduled for May, and a press release. That was enough.

In a market running on narrative and momentum, the signal that unlocks capital is not earnings or cashflow or competitive position.

What Gold Is Telling Us

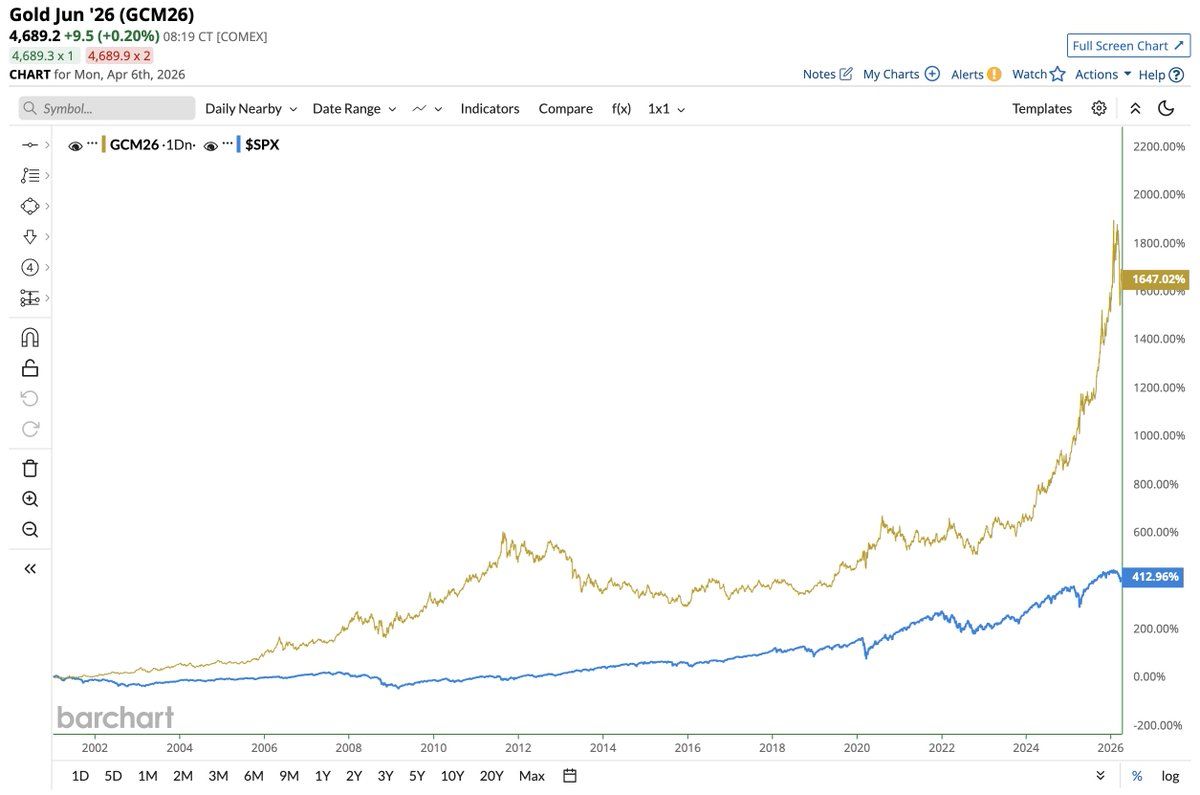

Gold is the real signal right now. The highest price ever recorded occurred on January 28, 2026, when it reached $5,589 per ounce. It currently trades around $4,800, having pulled back on Iran ceasefire optimism.

The 25-year performance record is where the real argument lives. A $10,000 investment in gold in January 2000 grew to approximately $126,596 by late 2025, while the same amount in the S&P 500 total return index reached $77,496. Gold compounded at roughly 10.4% annually against 8.3% for stocks over that span. The decade from 2000 to 2010 is the starkest chapter: gold's compound annual growth rate topped 15% while the S&P 500 barely eked out 0.32% annually, and the index needed 13 years just to claw past its 2000 peak.

Gold accomplished this without requiring its holders to assess earnings models, evaluate management teams, or predict competitive outcomes. You held it. It preserved value. The standard rebuttal is that gold pays no dividends and does not compound through reinvestment. Fair enough. But gold's long-run outperformance from a dollar-denominated starting point reflects something real about the currency doing the measuring. When a hard asset wins across multiple decades against the broadest equity index in the world, the monetary system is sending a signal worth taking seriously.

Bitcoin Extends the Argument

Gold demonstrates the case for sound money across long cycles. Bitcoin makes it programmable, portable, and scarce in a way no physical commodity can match.

When you own a share of stock, you own a claim on a business that can be mismanaged, disrupted, sued, regulated, or outcompeted. When you own bitcoin, you own a fixed monetary asset with no management team to second-guess, no earnings to miss, no supply chain exposure. The embedded risks are categorically different, and for savers who simply want to preserve purchasing power without becoming sophisticated investors, that distinction carries real weight.

The S&P 500 became the American savings account by default because for most of the past century, ordinary people had no better option. Bitcoin proposes a savings instrument whose scarcity is enforced by mathematics rather than by the discretion of central bankers and elected officials. The volatility is real and reflects an early monetization stage. But the underlying thesis grows stronger with every year of data, every deficit expansion, and every rate suppression cycle needed to keep the debt load serviceable.

Closing Thoughts

Markets are at all-time highs. But the S&P 500 in April 2026 is more concentrated than at any point in over 50 years, more expensively valued than at any time since the dot-com peak, and trading into a backdrop where consumer inflation expectations just posted their largest single-month spike in a year while the IMF revised global inflation upward.

A company with no revenue, no product, and no operational history in its new field can add hundreds of millions in market cap by changing its name and appending two letters. That is a reasonable portrait of where capital allocation instincts currently stand.

Sound money exists so that ordinary people are not required to become stock pickers just to preserve what they earn. Gold proved that thesis across the most turbulent monetary decades of the modern era. Bitcoin is building the next chapter. The case was never against productive capital allocation. The case is that the system should not demand sophisticated risk-taking as the entry price for simply saving.

That is the problem sound money solves.

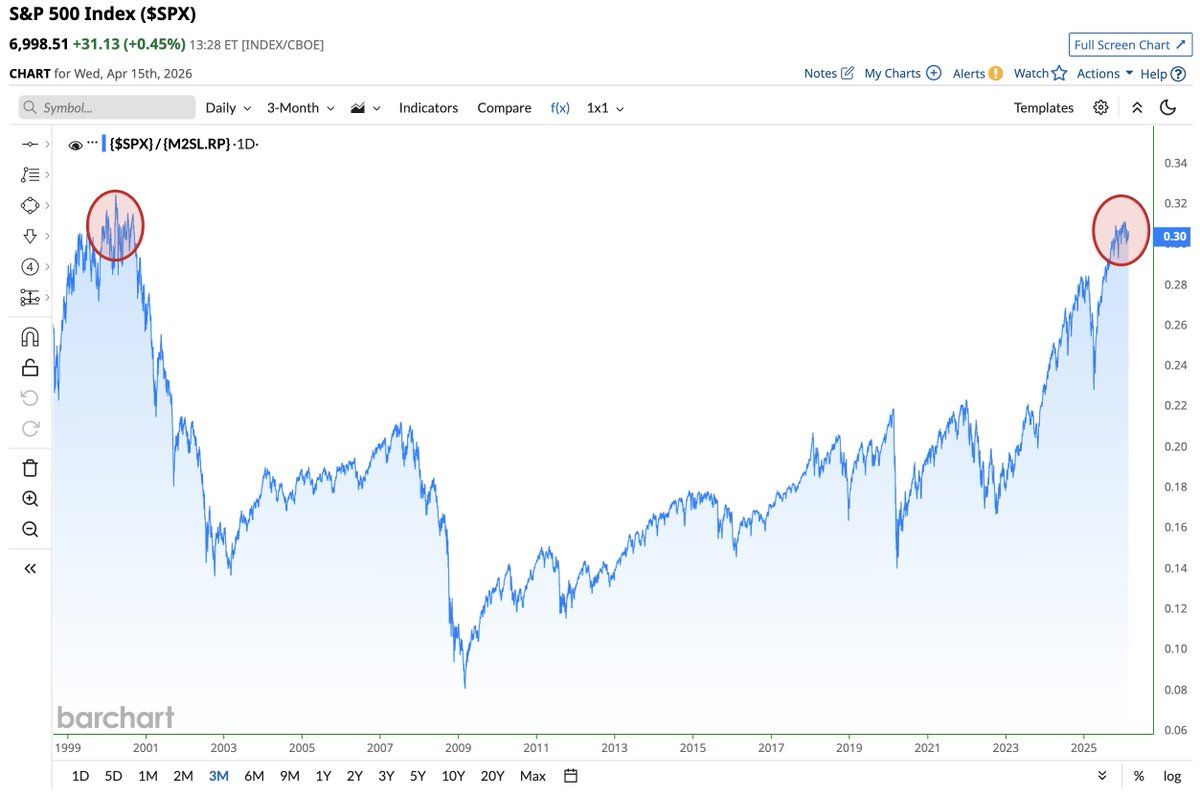

CHART OF THE WEEK

"S&P 500 relative to M2 Money Supply. Dot Com Bubble vs. Now."

QUOTE OF THE WEEK

"Separating authority backed by violence from the ledger (aka "money printer") is a critical aspect of advancing civilizations. The world would be a better place with an entirely independent ledger. Opt in to bitcoin."

PODCASTS OF THE WEEK

Morgan Stanley Just Ended the Bitcoin Bear Market

The Last Trade: Jackson, Michael, and Brian break down Morgan Stanley's Bitcoin ETF launch, the FDIC greenlighting the Genius Act, a Tennessee wrench attack ring hunting bitcoiners through DoorDash, Anthropic's Project Glasswing, and why bitcoin's 175% run during QT kills any bear argument.

Final Settlement: Bitcoin Is Money for Enemies

Final Settlement: Michael, Liam, and Brian break down bitcoin's role in global settlements, Morgan Stanley's ETF launch, Clarity Act progress, tokenization mania, private credit stress, and more!

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis