9/19/24 Roundup: Fed Cuts Rates: Another Turn of the Monetary Ratchet

Onramp Weekly Roundup

Written By Mark Connors & Brian Cubellis

Before we get started…

If you want to learn more about multi-institution custody and its benefits for securing bitcoin for generations — connect with Onramp.

And now, for the weekly roundup…

Mark Connors’ Macro Corner…

- Market Scorecard

- Another Turn of the Monetary Ratchet

- Either Way, Bitcoin Wins

Chart of the Week…

- The looming wall of US debt maturities

Quote of the Week…

- Druckenmiller on reactions to Fed policy

Podcasts of the Week…

- The Last Trade / Scarce Assets / Onramp Webinar Series / Wake Up Call

Market Scorecard

The divergence between Gold and Oil holds the most intel for investors on where the investment puck is going.

source: Onramp & Koyfin

Gold, +25% YTD and punching to new all-time highs by the day, has separated from economically sensitive Oil, which is roughly flat YTD, after rolling over of late, -11% over the past 3 months.

Global equities are in the middle, stuck in a range since sour global growth estimates emerged in July, leaving all major indices below their mid summer peaks.

NASDAQ remains up 17% YTD, down 1.3% over the past three months. Similar for the Japan’s Nikkei, +9% YTD, down 4% over the past 3 months, due in large part to the Yen carry trade unwind in late July, early August.

This divergence between Gold and Oil is due to the challenge of a weakening economy, which reduces oil demand, while investors are concerned about the Fed’s readiness to print money and cut rates, despite inflation NOT being fully under control.

Another Turn of the Monetary Ratchet

TLDR: While equities spent the summer in limbo, the U.S. money supply emerged from its first annual reduction in supply since the great depression, with the Fed, Treasury, and Congress all conspiring for an even larger uninterrupted expansion that may rival the Covid-19 print.

Three reasons yesterday’s 50bps rate cut was different:

1) Externalities played a big role.

- Currency volatility spurred by the unusual circumstance of U.S. rates being HIGHER than the majority of other sovereigns.

- Namely, August’s currency volatility that rocked Japan’s equity markets and spilled over into global markets.

- It was less about employment and price, more about global instability (Yen/ NKY) that ended up spilling over into U.S. markets.

- The Fed’s unintended consequence of providing a profitable global arbitrage between the cheap Yen and expensive USD had to end.

2) Liquidity increased BEFORE rates were cut.

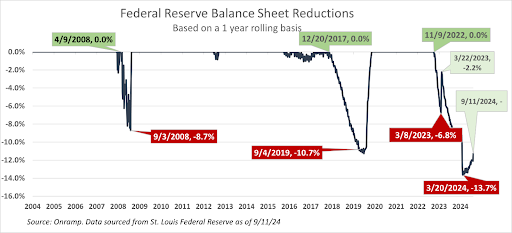

- The U.S. money supply (M2) started to increase months before the cut, which is unusual, as shown in the Fed balance sheet reduction chart below.

- The chart shows instances when the Fed reduced their balance sheet since 2002. Note the Fed reduced their degree of reduction starting this past March.

- The reversal in balance sheet management is very different than the period leading INTO the 2008 GFC, when the Fed drained liquidity with asset sales from April 2008 to September 2008.

- We believe the Fed has learned their lesson, that liquidity is needed to grease the inefficient, indebted banking and global financial system…well ahead of any rate cut.

3) The Fed’s third Mandate.

- For the first time, the Fed’s action was in support of their third, shadow mandate, to ensure proper market functioning.

- Yesterday we heard Chair Powell state that they acted to balance their dual mandates, full employment and price stability.

- Last week’s Roundup made the case that inflation is NOT in hand, so no balance there. As far as employment, yes, it does appear to be shifting, BLS restatements notwithstanding.

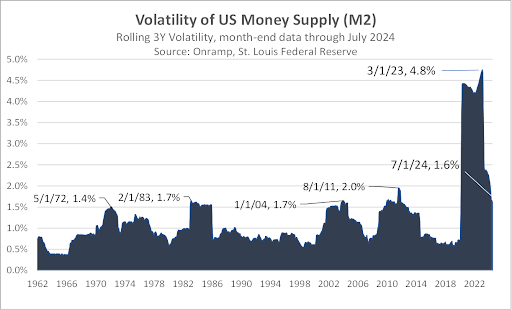

- The March 2022 rate hike campaign was the fastest in the Fed’s history, contributing to the destruction of Bank asset values and the March 2023 bank failures.

- To illustrate the historic impact, we show money supply (M2) volatility below. Note that the peak occurred in March 2023, the month the banks failed. The reason it declined is because the Fed intervened with $400B in liquidity including a new program called the Bank Term Funding Program (BTFP).

- Note the volatility in M2 has crept up as the Fed Balance sheet has increased over time. Managing this growing hoard of assets has required more attention and we believe a new shadow mandate: Proper Market Function.

Either Way, Bitcoin Wins

Too Big to Fail now applies to our economy as more treasuries are being bought by fewer players, prompting the Fed to manage the fallout.

The decline in the number and duration of recessions will continue. The magnitude of debt in the system has made a good old fashioned deflationary crash (1981-83, 1989-91, 2001-2003, 2008) untenable. Therefore, credit defaults and asset impairment will be ‘walked down’ and controlled by a Fed ready to ‘Foam the Runway’ to mitigate damage from crashing banks.

Bitcoin winning in a debt-driven inflationary spiral is intuitive. The secured and scarce nature of bitcoin is in stark contrast to fiat. Gold’s decentralized, relatively scarce nature has similarly thrived in previous periods of debasement.

If the Fed blinks, however, as they did in September 2008, and allows a major financial entity to fail, bitcoin may very well thrive as a stable monetary system outside the sclerotic, fractional reserve banking system.

Maybe the Fed is learning from their mistakes. In March 2023, the Fed had to add $400B in liquidity to support the spate of bank failures. The spike in volatility was a figurative pin prick to bank integrity.

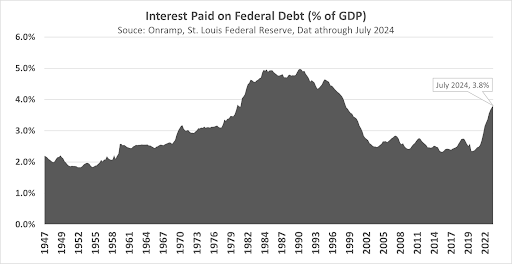

Today, we see a different spike emerging. This time it is the amount of interest expense and instead of a bank balance sheet, it is a sovereign. The United States balance sheet growing to 3.8% of GDP, with the risk to exceed 1980 peak levels.

Chart of the Week

“There is only one reason why the Fed cut 50bps this week…they MUST get front-end rates lower as this colossal wall of debt matures.”

Quote of the Week

“I don’t care if they go 25 or 50, I really don’t. But I can’t help but point out that right after inflation was 9% with rates at zero they went 25bp. Where were all the Wall Street cheerleaders calling for 50 because real rates are too high? The asymmetry in their narrative is striking.”

Podcasts of the Week

The Last Trade E065: Navigating Custodial Risk with Rich Kerr

In this episode of The Last Trade, Rich Kerr, Onramp’s President of Managed Wealth, joins to discuss social engineering attacks, physical wrench attacks, custodial risks of bearer assets, the evolution of bitcoin custody, challenges with plastic devices, trust & care in financial services, & more.

Scarce Assets E018: David Zell – Bitcoin’s Alignment with American Values

In this episode of Scarce Assets, hosts Andy Edstrom & Jesse Myers are joined by David Zell, co-founder of the Bitcoin Policy Institute, to discuss national security implications, concerns around partisanship, the path for sensible bitcoin policy, benefits of a strategic bitcoin reserve, & more.

Wake Up Call (9.16.24): Matt Golliher, Vista Investment Partners

In this episode of Wake Up Call, hosts Rich Kerr & Mark Connors are joined by Matt Golliher, Financial Advisor at Vista Investment Partners, to discuss how advisors can embrace bitcoin and properly educated their clients.

Onramp Webinar Series E004: The Evolution of Bitcoin Custody

Session 4 of the Onramp Webinar Series featured an insightful discussion with Onramp’s Jesse Myers, Brian Cubellis, Cam Stromme, & Jackson Mikalic, about the evolution of bitcoin custody, critical tradeoffs with various forms of custody, the merit of Multi-Institution Custody, & more.

Closing Note

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Find this valuable? Forward it to someone in your personal or professional network.

Until next week,

Mark Connors & Brian Cubellis