July 3, 2026 Roundup: Swindling Futurity

Brian Cubellis | Chief Strategy Officer

Free. Every week. One story that matters, read all the way down.

Sound money was written into America's founding on purpose, by men who had seen what happens without it. It was dismantled in stages across the twentieth century and abandoned entirely within living memory. The debt we carry into the country's 250th year is what that removal left behind.

Swindling Futurity

Tomorrow the country turns two hundred and fifty, and the version of the story it will tell itself is a political one, about independence and the men who declared it. What this version leaves out is the part that should concern us most, which is what the founding had to do with money.

The people who built this country had just watched a currency die. They financed the Revolution with paper, printed it faster than the war could absorb, and saw it lose almost all its value before the shooting stopped. That experience stayed with them. When they sat down to design the new government, they wrote rules meant to keep it from doing to the dollar what they had just done to their wartime paper money, and for a long stretch of American history those rules held. Then they were weakened by degrees, and the last of them was abandoned a little over fifty years ago.

You can blame this administration or that one for the size of the debt, and there is plenty of blame to spread around, but the deeper cause sits underneath all of them. Once the money was no longer tied to anything the government could not print, the ordinary limit on borrowing stopped existing, and the rest is arithmetic.

Continental currency note; $1; 1775

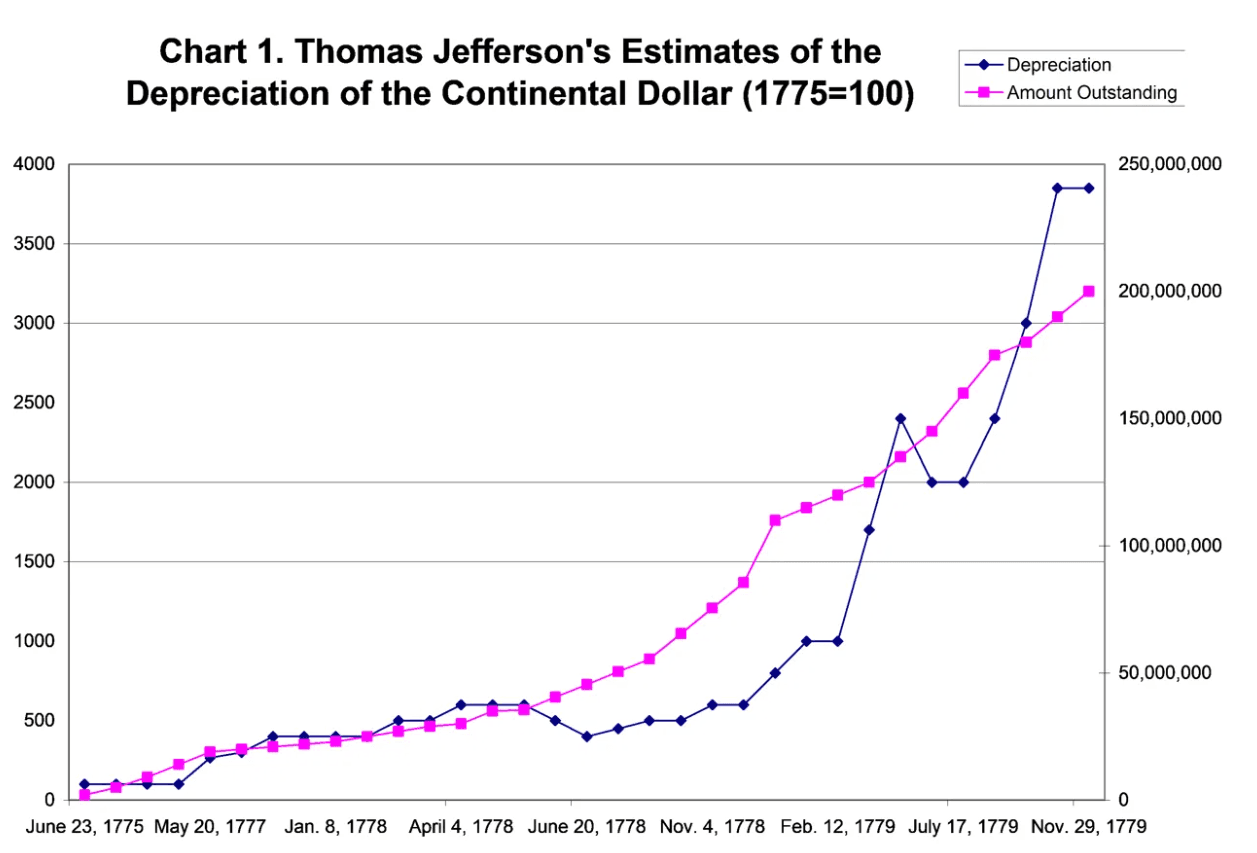

An early taste of debasement

The Revolution had to be paid for, and the Continental Congress had almost no power to tax. What it had instead was a printing press. Beginning in 1775 it issued paper money, the Continental, in escalating quantities to cover the cost of the war. The predictable happened. As the supply grew, the value collapsed, and by the early 1780s the currency had lost nearly all of its purchasing power. The failure was severe enough that "not worth a Continental" entered the language as a way of describing something with no value at all.

This was not ancient history to the framers. It was the recent past, still fresh, experienced firsthand by the same people who a few years later sat down to design the monetary architecture of the new republic. And they designed it as a direct response to what they had just watched happen.

Source: The Daily Economy

The response is written into our founding documents. The Constitution gives Congress the power to coin money, a deliberate choice of verb, and it forbids the individual states from making anything but gold and silver coin legal tender for the payment of debts. A few years later the Coinage Act of 1792 defined the dollar itself as a fixed weight of precious metal, 371.25 grains of fine silver, with gold pegged alongside it. Sound money, for them, was a structural reaction to having seen paper money destroy itself and take a good deal of the war economy with it.

The founders could not eliminate the temptation to inflate. No constitution can do that. What they could do was raise the cost of giving in to it, by tying the unit of account to something the government could not simply manufacture. For most of the next century and a half, in one form or another, that anchor held.

The rules held, then bent

The story from 1792 to the modern era is, at its core, the slow loosening and eventual severing of that anchor. It did not happen all at once, and it is worth resisting the temptation to treat any single date as the whole explanation. But the direction of travel is unmistakable.

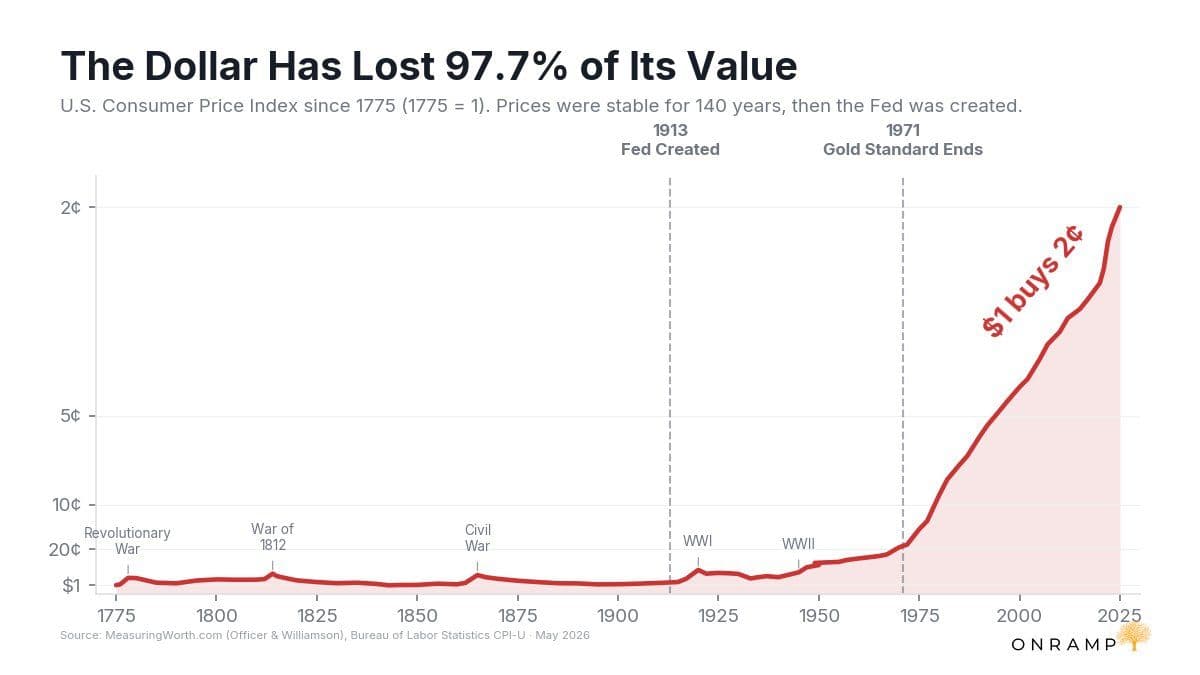

The creation of the Federal Reserve in 1913 centralized the issuance of currency and credit. In 1933, in the depths of the Depression, the government called in privately held gold and ended the domestic convertibility of dollars into it, then revalued the metal upward the following year. After the Second World War, the Bretton Woods arrangement kept a version of the discipline alive internationally, with the dollar convertible into gold at $35 an ounce for foreign governments and the rest of the world's currencies pegged to the dollar. The anchor was thinner and more remote than the founders had intended, but it was still there.

Then, on the fifteenth of August, 1971, it was cut entirely. Faced with foreign governments redeeming dollars for gold faster than the country wished to part with it, the Nixon administration suspended convertibility. What had been presented as a temporary measure became permanent. From that point forward the dollar was backed by nothing outside the government's own authority to issue it, and the last external constraint on how much the country could borrow and spend was gone.

As long as the dollar was tied, however loosely, to a quantity of something the government could not conjure at will, there was a hard ceiling on borrowing. You could run deficits, but they had to be financed within a system that ultimately answered to a fixed reference point. Remove it, and the only remaining limit on borrowing is political will, which is to say there is no reliable limit at all. Everything that has happened to the federal balance sheet since is downstream of that change.

Everything downstream

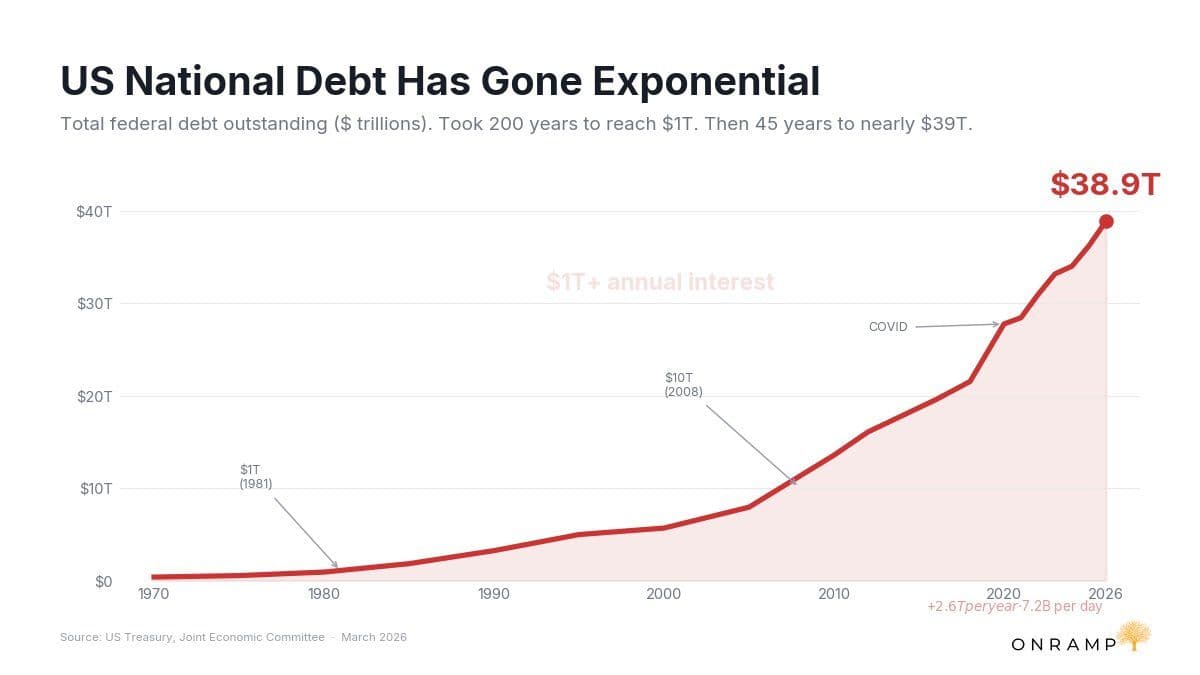

The gross national debt is close to crossing forty trillion dollars. Measured against the size of the economy, gross debt is running around 124% of GDP, a level the country has not seen since the immediate aftermath of the Second World War. The difference is that the wartime debt was borne of a single existential conflict and then paid down over the decades that followed. This time there is no war to explain it. There is only the accumulated result of spending more than the government takes in, year after year.

The annual gap is enormous and has become routine. The fiscal 2025 deficit came in at roughly 1.8 trillion dollars, close to 6% of the entire economy. Put in household terms, the government collected about 5.2 trillion dollars and spent about 7.0 trillion, which means that for every $1 it took in, it spent roughly a $1.34. A deficit of that scale in ordinary economic times would have been almost unthinkable under the monetary regime the founders built, because the regime itself would have made the borrowing prohibitively difficult long before it reached this point.

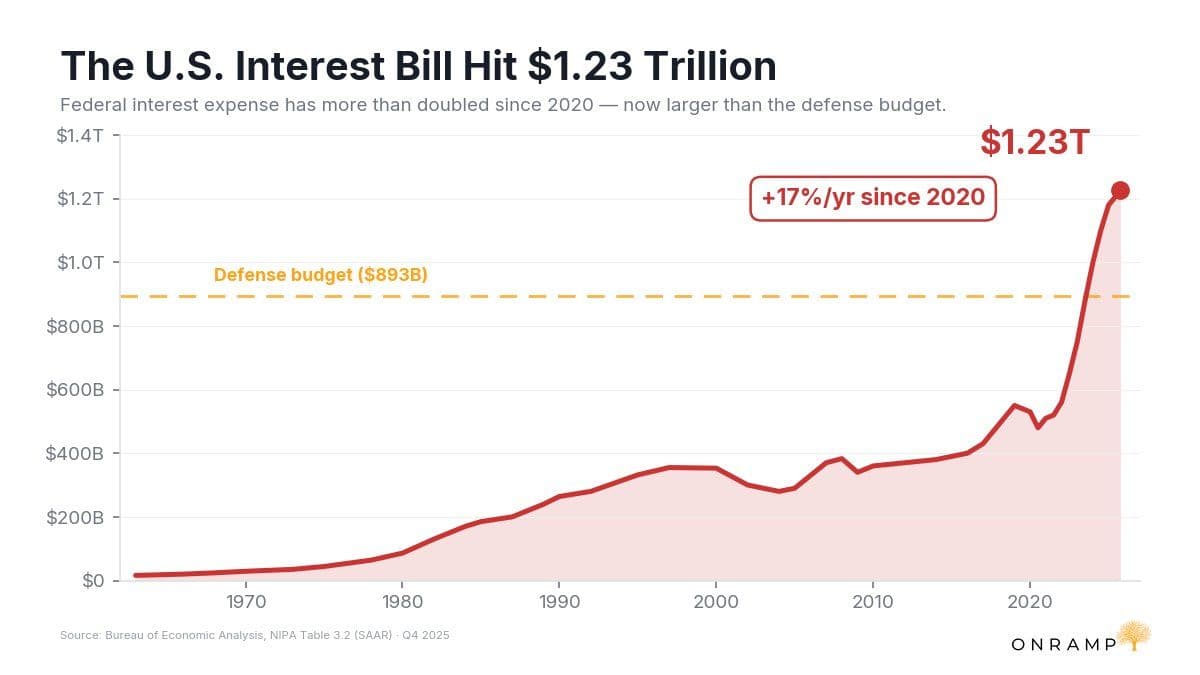

And now the arithmetic has begun to compound. Net interest on the debt has reached about 1.23 trillion dollars, a figure large enough to surpass what the country spends on national defense and to rank as the third-largest line item in the entire federal budget, behind only Social Security and Medicare. The Treasury is now paying on the order of 2.8 billion dollars every single day simply to service what it already owes. The Congressional Budget Office projects that net interest will roughly double to about 2.1 trillion dollars a year by 2036, and that the government will spend something like 16.2 trillion dollars on interest alone over the coming decade.

This is what a compounding trap looks like from the inside. Interest is now large enough to widen the deficit, the wider deficit adds to the debt, and the larger debt generates still more interest. None of it requires a new spending program or a new crisis to keep growing. It grows on its own, mechanically, because the constraint that once would have stopped it from reaching this size no longer exists.

Jefferson saw the mechanism

The remarkable thing is that the most precise description of this trap was written more than two hundred years ago, by the man who drafted the Declaration. Writing to John Taylor in 1816, Jefferson set down a sentence that reads like a definition of the thing economists now call fiscal dominance.

"And I sincerely believe, with you," he wrote, "that banking establishments are more dangerous than standing armies; and that the principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale."

Spending money to be paid by posterity. That is the entire modern arrangement, described succinctly, decades before the machinery to do it at scale even existed. He had worked the idea out more fully years earlier. In a letter to Madison in 1789 he treated the question of whether one generation has the right to bind the next as one of the fundamental problems of government, and he answered it from first principles.

"I set out on this ground," he wrote, "which I suppose to be self evident, 'that the earth belongs in usufruct to the living': that the dead have neither powers nor rights over it." From that premise he drew the conclusion directly. "Then no generation can contract debts greater than may be paid during the course of its own existence."

A debt that outlives the people who incurred it, in his framework, is not merely imprudent. It is a claim by the dead upon the living, a reversal of the natural order in which the earth belongs to whoever is currently standing on it.

We are the posterity he was worried about. The bill for a great deal of past spending has been handed forward to people who had no vote in the decisions, and the interest on that bill is now the fastest-growing obligation in the budget. The founders tried to make this outcome structurally difficult by anchoring the money. Jefferson wanted to go further and cap the term of any debt at the lifespan of the generation that took it on. The anchor was cut in 1971, the cap was never adopted, and the swindle he named runs today as ordinary policy.

There is a second, quieter danger worth mentioning. Once the debt grows large enough, the money itself becomes hostage to it. A central bank that would otherwise raise rates to defend the currency has to weigh the fact that every increase in rates raises the interest bill on nearly forty trillion dollars of debt. The temptation, at that point, is to keep money loose not because the economy calls for it but because the government cannot afford anything else. That is fiscal dominance in its mature form, the tail wagging the dog, monetary policy quietly subordinated to the task of financing the state. It is precisely the condition the founders' hard-money architecture was meant to make impossible.

The unfinished business of 1776

This is the frame in which bitcoin stops looking like a speculative curiosity and starts looking like a serious answer to a very old problem.

The founders wanted money that the government could not debase at will, and they reached for the only tool available to them, which was metal and the force of law. The law proved repealable. Over the course of the twentieth century it was amended, suspended, and finally set aside, and the discipline went with it.

What bitcoin offers is the same constraint the founders were after, sound money that cannot be quietly inflated to pay for the present at the expense of the future, implemented in a way that does not depend on any legislature keeping its word. The rules of its monetary policy are set at the protocol level, and no congress, treasury, or central bank has the authority to reach in and change them. The supply schedule is fixed and the terms are trustless in the specific sense that they hold regardless of who is in charge or what they would prefer.

The country was founded, in part, on the conviction that money should be something the state cannot manufacture to fund its own convenience. That conviction was written into the Constitution, defended for a century and a half, and then abandoned.

The fiscal position we now occupy, the forty trillion in debt, the trillion-dollar interest bill, the deficits that no longer need a war to explain them, is the downstream consequence of abandoning it. Jefferson told Madison that the earth belongs to the living. Two hundred and fifty years on, the living are servicing the debts of the dead, and looking for a way to stop.

The unfinished business of 1776 was always monetary. Bitcoin gives modern Americans a chance to finish the job.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis