June 12, 2026 Roundup: Liquidity Flows Downhill

Brian Cubellis | Chief Strategy Officer

Free. Every week. One story that matters, read all the way down.

This morning SpaceX will begin trading on the Nasdaq at a $1.77 trillion valuation, raising $75 billion in the largest IPO ever priced, two and a half times the old record. It arrives carrying months of narrative about capital rotating out of bitcoin to chase the AI listings, with OpenAI and Anthropic waiting in the wings.

We think the rotation story has the flow of funds exactly backwards, and the deeper lesson is about the difference between speculation and savings: one asset is priced for perfection at ~100 times revenue, the other sits at half its all-time high with a seventeen-year record of doing exactly what it was designed to do. Followed by our standard Chart, Quote, and Podcasts of the Week.

Liquidity Flows Downhill

SpaceX goes public on the Nasdaq today under the ticker SPCX. The offering priced at $135 per share, selling 555.6 million shares to raise $75 billion at a $1.77 trillion valuation, the largest IPO in history. The scale is hard to overstate. Saudi Aramco's listing raised $29.4 billion at a roughly $1.7 trillion valuation, and Alibaba's 2014 debut raised $21.8 billion; SpaceX has raised two and a half times the all-time record in a single deal.

The order book drew $350 billion in total demand, nearly five times the shares available, and first indications came in around $175, a 30% jump before a single share traded. It arrives as the first of three anticipated mega-listings, with OpenAI and Anthropic expected to follow, and for months a narrative has been building around these debuts: capital has supposedly been rotating out of bitcoin to position for the AI trade, with bitcoin's drawdown offered as the evidence.

We'd encourage readers to look closely at what is actually being sold today, and at what price.

SpaceX generated $18.7 billion in revenue last year and recorded an operating loss of $4.2 billion, with Starlink standing as the only profitable division. At the $135 offer, buyers are paying nearly 95 times trailing revenue for a business that loses money; at the indicated $175 open, the multiple climbs past 120 times and the market cap approaches $2.3 trillion, which would make SpaceX the sixth-largest public company in the world at its first trade.

Every company that has ever carried a trillion-dollar market cap was solidly profitable when it arrived, and the contrast with the existing club is stark. Among the nine public trillion-dollar companies, the smallest by revenue is Micron at $58 billion over the past year, more than triple SpaceX's top line, and the least profitable is Tesla, which still produced $3.8 billion of net income in 2025. SpaceX enters as the club's only unprofitable member, on the strength of a story about Starlink, Mars, and AI data centers in orbit.

SpaceX may well execute on much of that story. Musk's companies have a long record of embarrassing their skeptics, and Starlink is a genuinely remarkable business. But the relevant question for anyone treating a stock purchase as long-term savings is what the realistic path looks like from here. A double from the offer price would place SpaceX alongside Microsoft and Apple, companies that each earn roughly $100 billion a year. A triple, around $5.3 trillion, approaches the all-time record Nvidia set in mid-May at $5.7 trillion, and Nvidia supports that valuation by booking $68 billion of sales in a single quarter, more than triple what SpaceX produces in a year.

Wall Street itself can't agree on what's being sold today: Oppenheimer initiated coverage with a $190 target while Morningstar's probability-weighted fair value sits at $63 per share, less than half the offer price, with its analyst calling the gap the result of mathematics more than skepticism. The far more common path for hot issues, even ones backed by good businesses, runs lower before it runs higher. Facebook priced at $38 in May 2012 with a genuine profit machine underneath it, lost half its value within four months, and needed more than a year to reclaim the offering price. Rivian priced at $78 in November 2021, briefly doubled on debut euphoria, and has never traded at its IPO price since.

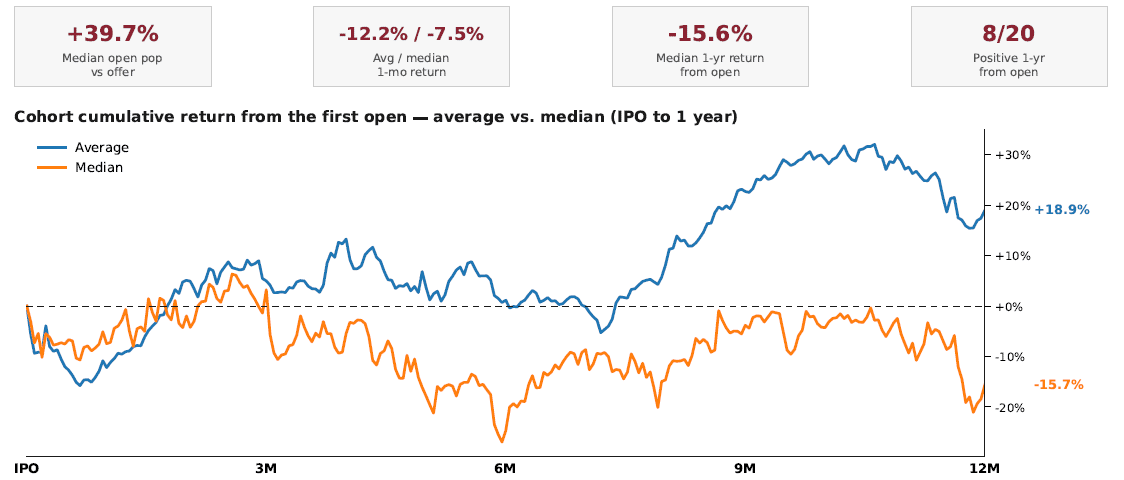

Renaissance Macro Research: "Arguably the most anticipated IPO ever debuts today. We pulled the 20 most-hyped IPOs since 1995 and measured 1st print returns. Avg 18.9% / Median -15.6% (most live the median experience). The gap between IPO pricing and 1st trade is 39% (It's a "Hype tax")."

Day-one demand has never been the question with these offerings, and $350 billion of orders settles it emphatically. The question is where the marginal buyer comes from in year two, after the staggered lockups have fully released in December and the float reflects everyone who wanted out.

Now set that against the asset capital has supposedly abandoned. Bitcoin trades near $63,600 this morning, roughly 49.5% below its all-time high of $126,080, putting the value of the entire network around $1.28 trillion. Sit with that comparison for a moment. A single unprofitable company is opening at a valuation roughly a trillion dollars greater than the entire bitcoin network, a monetary system with a fixed supply of 21 million units, an operating record stretching back more than seventeen years, and no dependence on any executive, product roadmap, or competitive moat. One asset is priced for perfection at the moment of maximum attention. The other sits at half price with no line out the door.

Which brings us to what the rotation narrative gets wrong. It assumes capital fled bitcoin to chase these listings, but consider who actually receives the liquidity. The company aimed to place roughly 30% of the offering, about $22.5 billion, in retail hands, and 70% of the institutional shares went to long-only investors; the bulk of the wealth event, though, accrues to employees and early shareholders, people who have spent their careers inside the technology industry.

This is the most bitcoin-literate cohort of sellers in the history of public markets. Their own employer told them as much in its prospectus: SpaceX's S-1 disclosed 18,712 BTC held as a strategic reserve, acquired for $661 million at an average cost near $35,300 per coin and carried at $1.29 billion as of March 31, with no sales since late 2024. The position is larger than Tesla's, and it means the company these sellers are cashing out of chose bitcoin as the home for its own excess cash, nearly doubling its money in the process.

And the liquidity arrives fast. SpaceX skipped the traditional six-month cliff in favor of a staggered release. Insiders can sell up to 20% of eligible shares after the company's first earnings report as a public company, rolling tranches unlock at 70, 90, 105, 120, and 135 days, another 28% releases after the second earnings report, and every restriction lifts at the 180-day mark, which falls in mid-December. A friends-and-family carve-out covering 5% of shares carries no lockup at all, meaning roughly $3.75 billion could reach the market on day one.

There's even a performance trigger: if the stock holds 30% or more above the offer price for five of ten consecutive trading days, an additional 10% of insider shares unlocks early, which means today's hot open is itself accelerating the supply it celebrates. The lone exception is Musk himself, restricted for 366 days, a fitting detail in an offering whose valuation rests so heavily on one man: the key-man cannot sell for a year while everyone who built the thing gets release valves starting at the first earnings print.

For the employee base, the exits open within weeks. When that cash lands, they will survey the same landscape every newly liquid saver surveys: equities near record multiples, real estate at generational unaffordability, bond yields that barely clear the official inflation rate and fall well short of the true pace of monetary expansion, and bitcoin at half price. Capital flowing from these liquidity events into bitcoin at depressed levels is the more logical trade, and we suspect it begins playing out well before year-end while the rotation story dominates the headlines.

The deeper point is one we return to often. Buying an IPO is speculation in the precise sense of the word. The buyer is underwriting competitive dynamics, execution risk, capital intensity, key-man exposure, and the patience of future shareholders, all in exchange for a claim on cash flows that do not yet exist. Some of that speculation will be rewarded, and there is nothing wrong with the exercise as long as it is named honestly.

Savings is a different discipline. Savings is the portion of your labor you intend to carry across time without asking anyone to perform on your behalf. Bitcoin was purpose-built for that job, with a known supply, protocol-level rules no boardroom can amend, and seventeen years of doing exactly what it was designed to do. Fortunes will be made in SpaceX by people who got in years ago at a fraction of today's price. That entry point doesn't exist anymore. Bitcoin's does.

CHART OF THE WEEK

"We can see that the narrowing or broadening is really just an AI vs ex-AI dynamic. Excluding AI, the market has not even taken out the pre-Iran highs, although in recent days it has come close. On Friday when the SPX was down 2.6%, the Goldman Sachs ex-AI basket was flat. It’s a good reminder to remain diversified."

QUOTE OF THE WEEK

"AI & robotics should be the most disruptive event in human history, except for maybe the Black Death. Will be massively deflationary. But… in a paper money world that economic reality will almost surely be turned upside down. Can’t print Bitcoin."

PODCASTS OF THE WEEK

The Dollar Reset Runs Through Bitcoin | Matt Dines

The Last Trade: Matt Dines, CIO of Build Asset Management, joins to lay out the seismic monetary reshuffling underway in 2026, the unwind of the post-Bretton-Woods offshore-dollar system that ran the global economy from 1971 to 2022, why LIBOR's deprecation and the SOFR transition quietly moved the dollar's command center from London to New York, Scott Bessent's strategy to monetize the asset side of the Treasury balance sheet through the GENIUS Act stablecoin and a Bitcoin reserve targeting 1 million BTC, Tether's December 2023 alignment with the American Sovereignist movement, and the contrarian read on MicroStrategy as a "dollar strategy" rather than a Bitcoin strategy.

Inside the SpaceX IPO And Why Bitcoin Is the Value Trade

Final Settlement: This week Brian, Michael, and Liam cover the SpaceX IPO and the capital-rotation narrative around Bitcoin, the Bernie Sanders / David Sachs debate over government equity stakes in AI companies, the Zcash inflation bug that allowed unlimited mint for four years before Claude caught it, JPMorgan's tokenized-deposit consortium with Citi, Bank of America, Wells Fargo, and Chase, the Stripe / Visa / MasterCard stablecoin consortium, Morgan Stanley's Galaxy partnership letting high-net-worth clients lend Bitcoin for in-kind ETF conversions, Tether's first gold-backed Visa card, the US sanctioning Iran's largest crypto exchange Nobitex, and the Polymarket MicroStrategy resolution controversy.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis