June 26, 2026 Roundup: The Signal in Five Charts

Brian Cubellis | Chief Strategy Officer

Free. Every week. One story that matters, read all the way down.

Five charts this week in place of the usual structure, and they tell one story. The market's most crowded trades were built for a falling cost of capital, and the Fed has taken rate cuts off the table. The AI buildout is spending well past the cash it throws off, the private credit redemption queue continues to grow, and the bitcoin treasury wrappers are breaking. Bitcoin itself carries none of that leverage, and it is sitting right at the level that has marked every prior cycle low.

The Signal in Five Charts

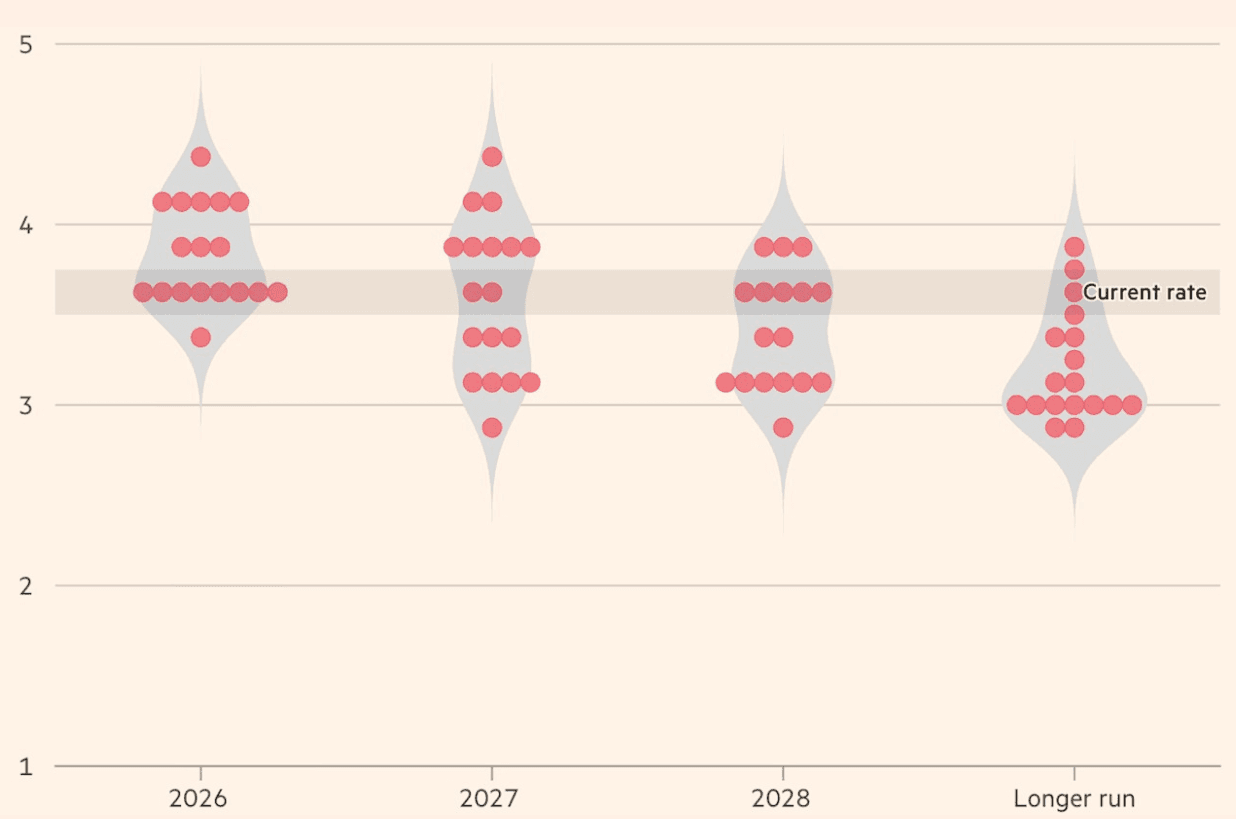

1. The dots flip higher, and a trapped Fed shows its hand

Source: Financial Times

The June dot plot is the clearest read yet on a central bank boxed in. For 2026, almost every projection now sits at or above the current 3.50% to 3.75% rate, a knot of them gathered near 4%, one reaching toward 4.4%, and a single lonely dot below today's level. The median moved up to 3.8%, a reversal of the cut the committee still carried at the end of last year, with six participants marking more than one hike and seventeen of eighteen seeing inflation risk skewed higher. The hold was unanimous and the statement was cut to 130 words, but the most telling mark on the page is the one that is missing. Kevin Warsh, in his first meeting as chair, declined to submit a dot, calling it unhelpful to the conduct of policy and flagging a year-end review of the dots and the rest of the forward-guidance apparatus.

The turn higher is less a show of strength than an admission of the corner. Rates are leaning up into an energy crisis the Fed cannot drill its way out of, a federal deficit it cannot hike its way out of, and inflation that has stayed stubborn through both, with the committee's own 2026 price forecast lifted to 3.6%. Oil actually fell back after the interim US-Iran peace and the projections tightened anyway, which says the pressure it fears runs deeper than the barrel.

The policy rate is a tool built for a demand problem, and this inflation is a supply-and-deficit problem, so every hike does little except raise the government's cost of carrying the very debt feeding the fire. A Fed fighting this with interest rates is working from a broken toolkit, and the market knows it, pricing the odds of a hike by December near three in four.

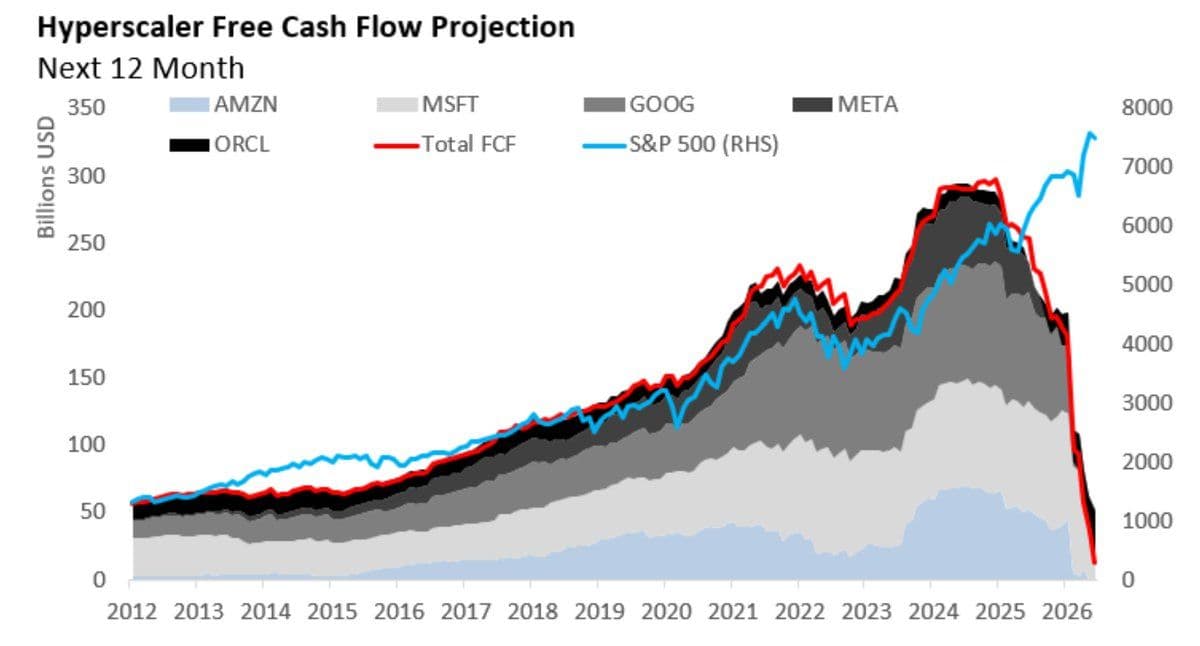

2. The cash that built the bull market rolls over

Source: Nomura

For more than a decade the S&P 500 and the free cash flow of its largest names moved as one line. Amazon, Microsoft, Google, Meta, and Oracle threw off a rising tide of cash, the index tracked it almost tick for tick, and what looked like a story about multiples was, underneath, a story about cash. The chart is that relationship drawn out from 2012, the red line and the blue line climbing together for fourteen years.

Then look at the right edge. The red line, the projected next-twelve-month free cash flow for the five, falls almost vertically from near 290 billion dollars toward zero as the AI build, headed toward a trillion a year, consumes the cash these businesses have always generated. The blue line does the opposite, pushing to fresh highs near 7,500 while the cash beneath it drains. The two have come apart for the first time in the series.

The index is printing records exactly as the free cash flow that justified it disappears into capital spending, funded at the margin with debt and priced off a cost of capital that just reset higher. Whether the gap closes by the cash returning or the price falling is the question the next few years will settle. The chart only says that something has to give.

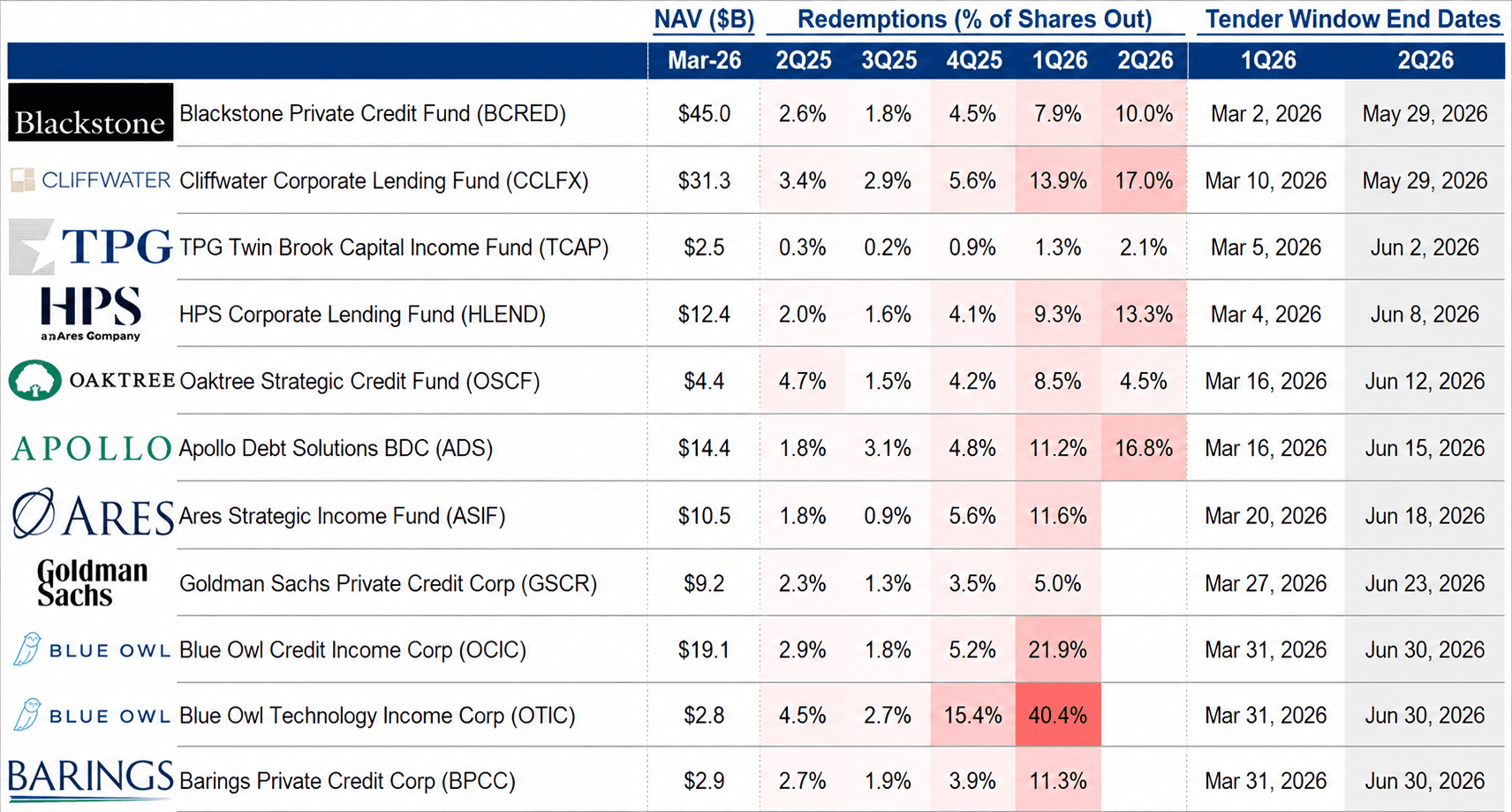

3. Private credit takes its first real liquidity test

Source: Evercore

The table shows a redemption queue forming across the largest non-traded private credit funds, and the line asking for money back grows every quarter. A year ago, requests at vehicles like Blackstone's BCRED, Apollo's ADS, and the Blue Owl funds ran in the low single digits as a share of the fund. By the most recent windows they had jumped into the double digits nearly everywhere, Cliffwater and Apollo near 17%, HPS at 13%, Blackstone at 10%, and Blue Owl's technology and credit vehicles at 40% and 22%. From late last year into this quarter, the shape is a slow run, with defaults on the broader measure of private credit already at the highest on record.

Almost none of that money is actually leaving. These funds let investors out only through quarterly tender windows capped near 5% of shares, so a 40% request against a 5% gate means the gate is doing exactly what it was built to do, holding the door while the marks stay where the manager put them. That is the tension under the whole asset class. Net asset value here is set by model rather than by trade, so it reads smooth for as long as nobody is forced to sell, and the gate is the thing that guarantees nobody is. An asset you cannot exit at its marked price is worth whatever you could actually get for it, and the gates exist so that no one has to find out.

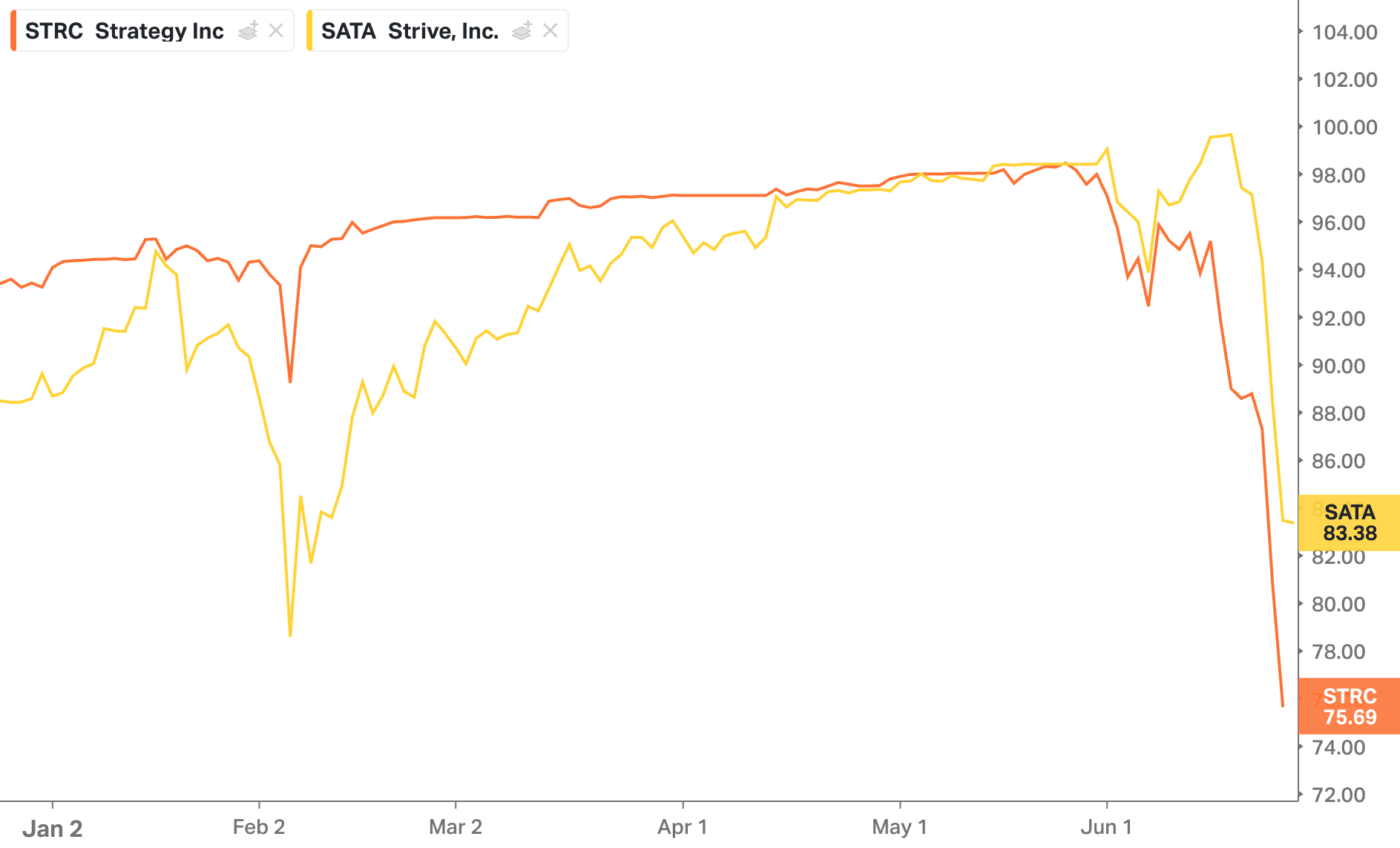

4. STRC and the 'money market like' fallacy

Source: Koyfin

The chart shows two "Digital Credit" instruments, Strategy's STRC and Strive's SATA, sold on the same promise. For months they did the one thing they were built to do, holding a tight band around par of $100 while the marketing pointed at the flat line as proof of safety. Then June came and both broke together, STRC to about $76 and SATA to $83.

The case was never that Strategy implodes tomorrow. It was that the fundamental risks of these instruments were purposely obscured. STRC is perpetual preferred equity, with no maturity, no lien on a single coin, a dividend the board can cut or defer at will, and a claim sitting junior to billions of dollars of senior debt. None of that is what "money-market-like" describes. A money market is short, principal-stable, and segregated, while STRC is perpetual, principal-permanent, and unsecured, and the low volatility that flattered every risk metric was manufactured by seven straight defensive dividend raises from 9% to 11.5%, each one a response to capital walking out the door.

As our own research from roughly two months ago put it, STRC carries the counterparty risk of a bank, the custody risk of an exchange, and the opacity of a hedge fund, bolted onto an asset whose whole purpose was removing all three. What makes it worse than a bad trade is who was on the other side. Roughly 82% of STRC sits with retail, sold a leveraged wrapper in the language of a savings product, while the same pitch told a second story about institutional money stuck in low-yield mandates finally getting bitcoin-backed income. That buyer cannot be both informed and rational, because any institution that does the work to underwrite an unsecured perpetual preferred on a bitcoin treasury reaches the cleaner answer every time and buys the spot asset instead.

The simpler trade we have made the case for, real bitcoin in cold storage beside a Treasury ladder, hands over the same income and keeps the actual coin, with none of the layers.

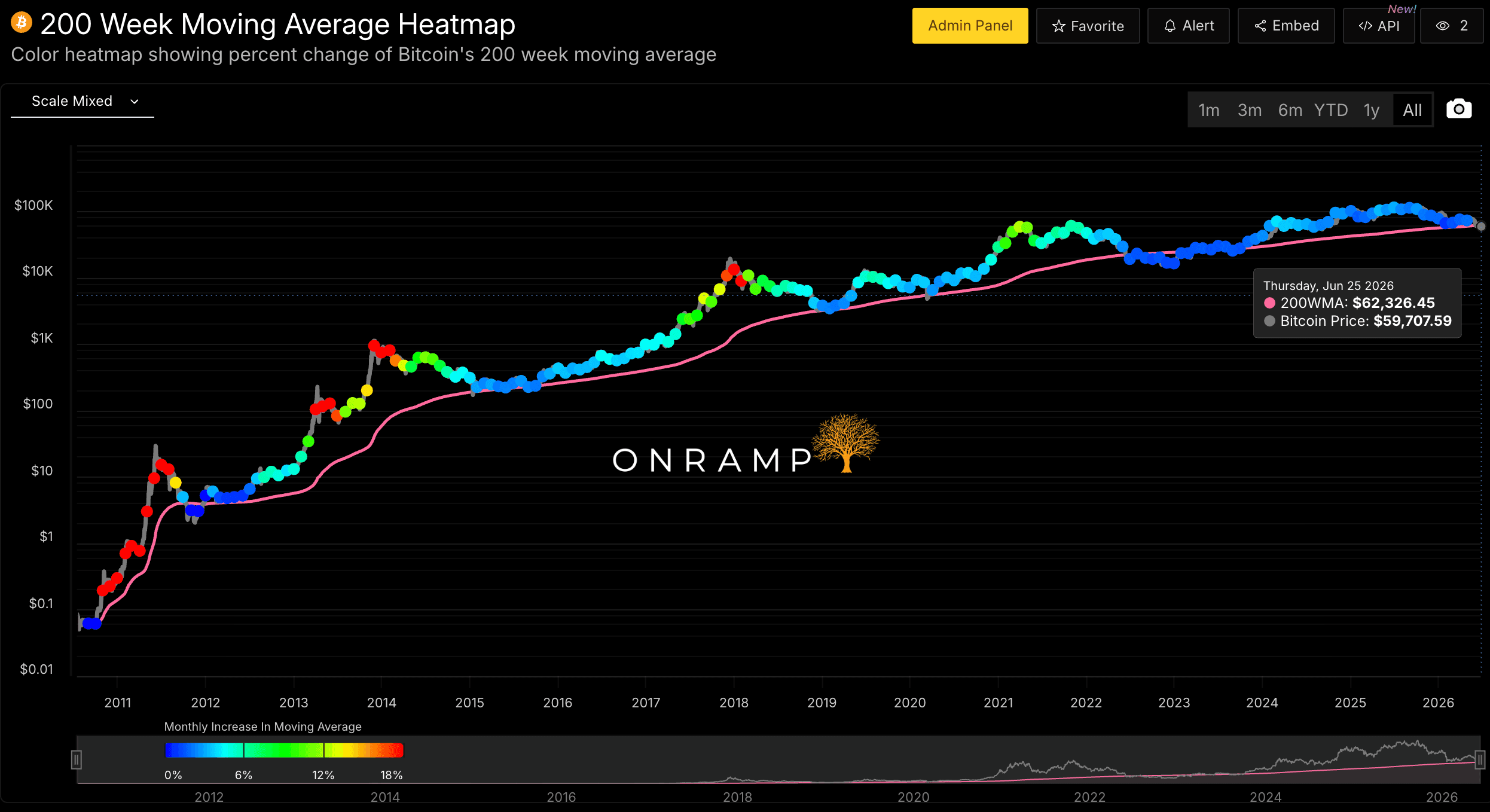

5. Bitcoin sits in deep value at the 200-week line

Source: Onramp Terminal

The pink line is the 200-week moving average, the slow floor under four years of price, and the dots are price colored by how fast that floor is climbing. Blue marks the months when the climb goes flat, and those blue runs sit on every major bottom the asset has made, 2015, 2018, and 2022. Two things stand out this time. Each cycle top has run cooler than the last, red in 2013 and 2017, green in 2021, and only light blue at the 2025 high, the signature of an asset whose volatility keeps compressing as it matures. The right edge is dark blue again, today's price around $60,000 against a 200-week average of $62,300, the first time this cycle bitcoin has traded beneath the line.

That is the deep value end of the range, where sats are on sale, and the math is plain. Bitcoin has closed below this line on about a tenth of all trading days since 2017, and buying those windows returned a median above 113% over the next year and past 300% over two, with two days to break even and a worst drawdown near 9%. For anyone whose horizon runs in years, this is the range history has rewarded, and the only move it has ever asked for is the long view.

Back to Basics:

Everyone's a Scammer

In 2014, with bitcoin under five hundred dollars and the scams cruder, Michael Goldstein, the writer better known as bitstein, published "Everyone's a Scammer" (Satoshi Nakamoto Institute). His argument was that the real threat to your bitcoin was never the hacker. It was the pitch.

The essay sorts the combatants: merchants who tell you your coins are worth only the price of their goods, and investments that promise a better return than simply holding. Each is built to convince you to hand over the asset for something that looks like a deal in dollars and turns out to be a terrible one measured in bitcoin. Goldstein's test was a single question, whether the thing beats just holding, and almost nothing does.

Twelve years later, the pitch has a balance sheet and a marketing budget, and chart four above is the essay come to life. "Digital Credit" tells an investor bitcoin is too volatile, hands him a coupon, and keeps the appreciation for the issuer. It is the merchant and the investment peddler in a suit. The defense has not changed. Measure the offer against the asset, lower your time preference, and keep the coins. As Goldstein put it, "scammer" is a heuristic, not an accusation, and the only winning move is to hold the thing itself.

PODCASTS OF THE WEEK

The Last Trade: Jackson, Michael, and Brian go signal versus noise on the most confusing Bitcoin tape in years, with Bitcoin in the 50s and roughly 50% off its all-time high. They make the deep value case (a 5-year DCA into Bitcoin matches the S&P 500 while sitting 50% below its highs, the 200-week moving average flashing, and a gold analog that ran 750% off a similar drawdown), break down the Strategy / STRC confidence crisis and why the whole DAT experiment increasingly looks like an objective failure, and riff on Warsh's Fed, the hyperscaler free cash flow cliff, Trump's quantum order, and Meta moving into prediction markets.

Franklin Templeton's New Bitcoin Product & The Truth Behind AI

Final Settlement: This week Brian, Michael, and Liam cover Anthropic's Mythos and Fable controversy and the orchestrated open-source-vs-frontier AI dynamic, Franklin Templeton's new ETFs that auto-invest stock dividends into Bitcoin, Fidelity and State Street's entry into stablecoin reserve management, Illinois Governor Pritzker's 0.2% crypto wealth tax, the Fed's 130-page stablecoin KYC rulemaking, Binance's MiCA expulsion, Coinbase's tokenized-stocks rollout, SpaceX's IPO run and $60B Cursor acquisition, and the latest on Strategy's stretch product.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis