April 14, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

Three systems of trust - physical, monetary, and custodial - are fracturing at once. As Iran privatizes the Strait of Hormuz, governments debase in unison, and France empties its gold from New York, the world is left asking what instrument settles trade between adversaries.

Why the world's next reserve asset won't be issued by a government

The Trust Collapse

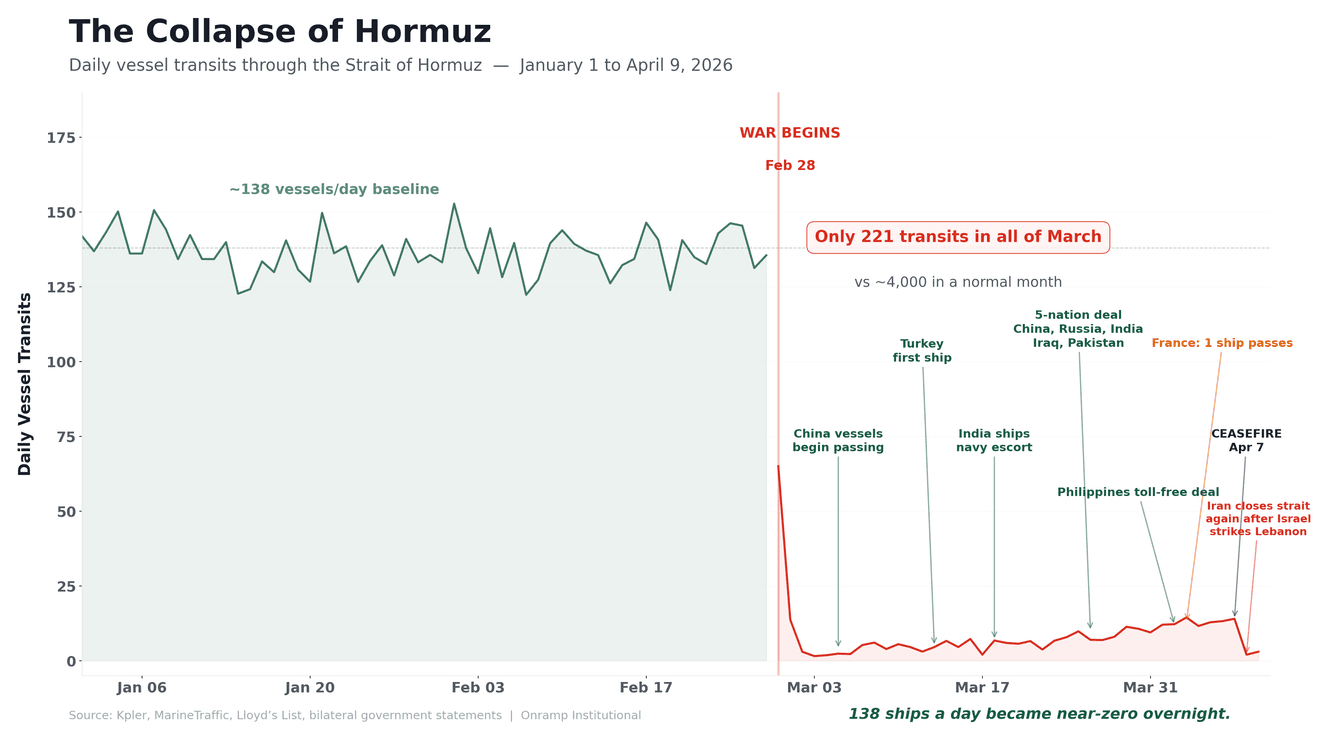

On February 27, 2026, one hundred and thirty-eight commercial vessels transited the Strait of Hormuz - a normal day. By March 2, the number was near-zero. In the five weeks since, the narrow waterway through which a fifth of the world's oil once moved freely has been transformed into something the post-war order was specifically designed to prevent: a chokepoint controlled by a single state, open to some, closed to others, and priced at the discretion of the gatekeeper. This is a story about that chokepoint. But it is not, ultimately, a story about oil. It is a story about what happens when the three foundations the modern global economy was built on - neutral shipping lanes, sound currencies, and secure vaults - fracture at the same time. It is a story about the collapse of trust between nations. And it ends with a question that, six months ago, would have sounded ideological but today sounds like common sense: in a world where no single power is trusted by all parties, what instrument settles trade between adversaries?

The Tollbooth

Lloyd's List, the 290-year-old shipping journal that has chronicled maritime commerce since the age of sail, gave it a name within days: the Tehran Toll Booth. By the second week of March, the Revolutionary Guard Corps had made its position clear. The Strait of Hormuz was not closed. It was under new management.

The mechanics are worth studying closely, because they reveal something far more sophisticated than a blockade. China, Russia, India, Iraq, and Pakistan were granted permission to transit. Japan secured passage for two tankers through careful bilateral talks. Malaysia and Thailand negotiated their way through. Turkey sent three ships, with eight more waiting for clearance. The Philippines - a treaty ally of the United States that imports 98% of its crude from the Middle East - declared a national energy emergency, then dispatched its foreign secretary to Tehran to cut a deal directly. By early April, Iran had granted selective access to more than a dozen nations. But permission and passage are not the same thing. Only 221 vessels crossed the strait in the entire month of March - barely 5% of normal traffic. The strait was not closed, it was rationed. And the nation locked out entirely was the one that had spent eighty years guaranteeing everyone else could pass freely.

The distinction is critical. Iran did not blockade Hormuz. A blockade is blunt, indiscriminate, and economically ruinous for the enforcer as much as the target. What Iran constructed was something altogether more dangerous: a selective access regime - granting permission based on political alignment, extracting revenue from the compliant and leverage from the excluded. It was not an act of desperation. It was a new business model. Kpler recorded those 221 commercial transits against more than 4,000 in a normal month. Vessels that did pass moved through an IRGC-controlled corridor around Larak Island, at Iranian-dictated times, after submitting cargo manifests, crew lists, and ownership records to Revolutionary Guard intermediaries. Lloyd's List - the 290-year-old shipping journal that named it the "Tehran Toll Booth" - reported transit fees of roughly $2 million per passage, settled in Chinese yuan or Bitcoin. Not dollars. The currency of the nation whose navy used to guarantee free passage is the one currency Iran will not accept.

For eighty years, the deal was simple: The United States guarantees the sea lanes, the world prices oil in dollars. That deal did not survive a Truth Social post.

On April 5, the President of the United States addressed Iran on social media with language that does not bear full repetition here, demanding it reopen the strait. The following day, he told allies who declined to join the war to "build up some delayed courage, go to the Strait, and just TAKE IT." He floated withdrawing from NATO.

The message, beneath its chaos, was unambiguous: the American security guarantee - the foundation on which the entire architecture of globalised energy trade was built - is no longer unconditional. And America's allies heard it with perfect clarity. They did not rally behind Washington. They went to Tehran.

This is not how the system is supposed to work. The entire edifice of globalisation - from container shipping to energy markets to the petrodollar itself - rests on the assumption that critical infrastructure is maintained as a neutral public good, underwritten by a power strong enough and willing enough to keep it open for everyone. When that assumption fractured at Hormuz, it did not merely disrupt oil markets. It revealed, under live fire, that the neutral layer the global economy depends on can be captured, monetised, and selectively operated by a single actor - while the guarantor of last resort watched from the sideline, tweeting threats. Every institutional allocator models geopolitical risk. Almost none have modelled the risk that the infrastructure itself picks a side.

The Printing Press

If the Strait of Hormuz demonstrated that physical infrastructure can be captured by an adversary, the sovereign debt markets are demonstrating something more insidious: that monetary infrastructure is being debased by the very governments that issue it.

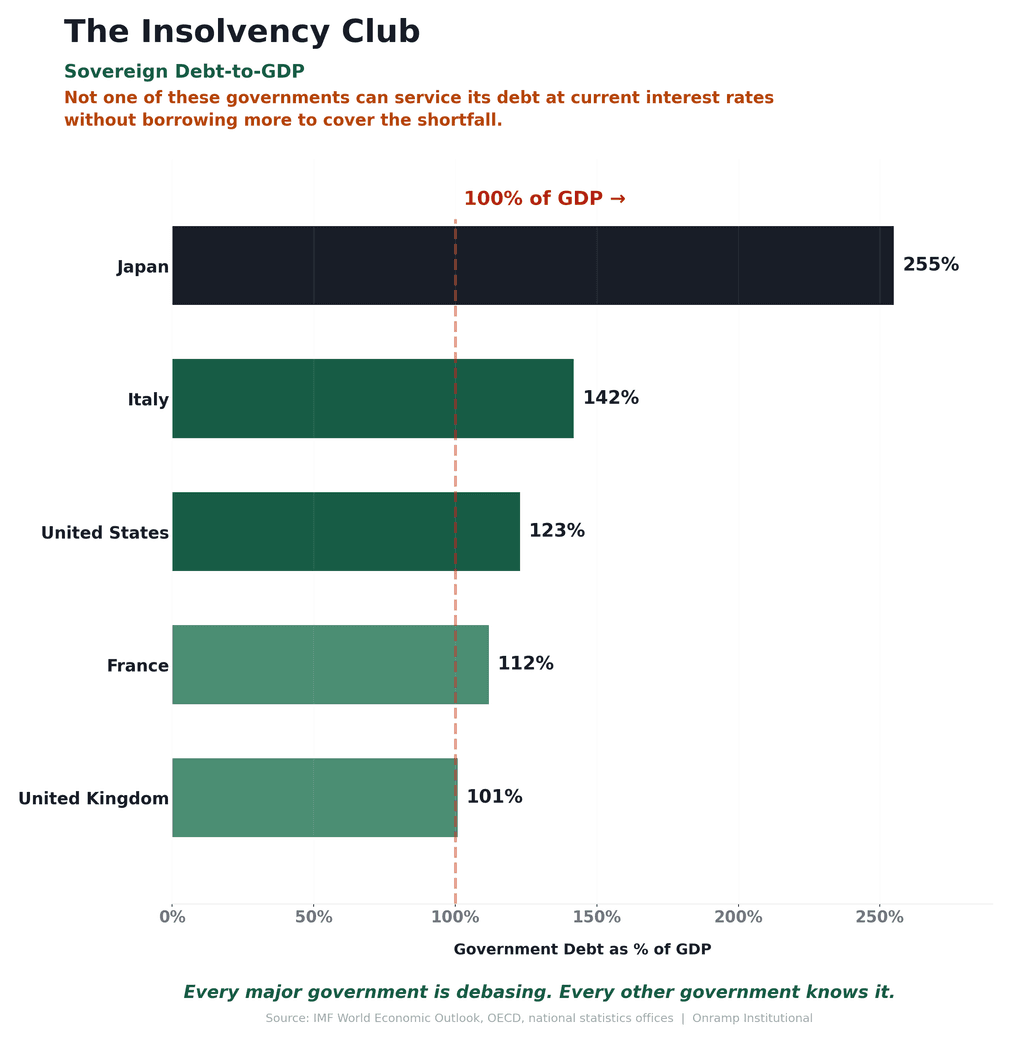

The numbers are familiar individually. Their simultaneous convergence is not. US federal debt has surpassed 120% of GDP. The United Kingdom sits above 100%. France above 110%. Japan above 250%. Italy above 140%. Not one of these governments can service its existing obligations at current interest rates without issuing new debt to cover the gap. The polite term for this is "fiscal dominance." The honest term is slow-motion insolvency, managed through the quiet erosion of each currency. This does not show up in exchange rates, because they're all debasing their currency at the same time.

Every major sovereign is running the same programme: issuing new liabilities to service old ones, while depending on its central bank to keep borrowing costs below the rate of economic growth. The trap is straightforward. When inflation rises, it should force interest rates higher. But a government that owes more than 100% of GDP cannot afford higher rates - at 120% of GDP, every percentage point of additional interest costs the United States more than $300 billion a year. So the central bank faces a binary choice: raise rates and blow up the government's fiscal position, or hold rates artificially low and let the currency absorb the damage. Every government in history that has faced this choice has eventually reached for the same mechanism: the printing press. Not because it solves the problem, but because it is the only option that defers the consequences past the next election.

The war has compressed this dynamic with violent speed. The United States is spending billions on Operation Epic Fury while simultaneously drawing down its Strategic Petroleum Reserve - which itself must be replenished at today's elevated prices. The IEA has committed to releasing 400 million barrels in the largest coordinated intervention in its history. European nations are scrambling to increase defence expenditure because Washington has told them, in terms both blunt and public, to defend themselves. The OECD's revised inflation forecast for the US in 2026 has nearly doubled, from 2.8% to 4.2%, driven almost entirely by the energy shock. Every major government's fiscal position deteriorated simultaneously, for the same reason - and the only tool available to any of them is the one that makes the problem worse in the long run: borrow more, print more - and pray that no one notices a unit of account that measures the rate of debasement of all of them at once.

And here is the recursive trap that distinguishes this moment from every previous debt cycle: every government knows every other government is debasing.

Beijing knows the Federal Reserve will ultimately monetise. The Fed knows the ECB will do the same. The ECB knows the Bank of Japan has been doing it for a decade. This mutual awareness is corrosive in a way that is difficult to overstate, because it poisons the reserve system from the inside. Why would China continue to hold $800 billion in US Treasuries when it understands that Washington's long-term fiscal strategy requires those obligations to be worth less in real terms? Why would Riyadh continue to price oil exclusively in a currency whose issuer is deliberately eroding its purchasing power? Why would any sovereign wealth fund treat any government's liability as a store of value when the stated policy of the issuer is to diminish that value over time?

This is not a hypothetical. China has quietly reduced its US Treasury holdings by more than $500 billion since 2013. Saudi Arabia has accepted yuan for oil sales. Central banks around the world have been accumulating gold at the fastest pace in sixty years. Their actions are speaking well ahead of and far louder than their rhetoric.

For decades, the answer to "why hold dollars?" was brutally simple: because there was nothing better. The dollar was the least bad option in a world of worse ones. But "least bad" is a brittle foundation for the world's reserve currency. It holds only so long as every alternative remains inferior - and only so long as no new category of monetary asset emerges that is simultaneously neutral enough for adversaries to trust and scarce enough that no government can print more of it.

The Empty Vault

On April 6, 2026, a story broke that attracted a fraction of the attention directed at the Hormuz deadline. It may prove to be the more important one.

The Banque de France disclosed that it had completed the repatriation of every gram of gold it held at the Federal Reserve Bank of New York.

The world's central banks are pulling their gold out of New York and London. The question is what they know that the rest of us don't.

The mechanics were carefully chosen. Rather than shipping 129 tonnes of physical bullion across the Atlantic — a conspicuous, expensive, and diplomatically explosive exercise - the Banque de France sold its New York holdings in 26 separate transactions between July 2025 and January 2026, then purchased an equivalent quantity of modern-standard bars on the European market. Not a single bar crossed the ocean. The operation delivered a capital gain of €12.8 billion. Every ounce of France's 2,437 tonnes of gold - the fourth-largest sovereign reserve in the world - now rests in La Souterraine, a secure underground facility south of Paris.

Governor François Villeroy de Galhau insisted the decision was "not politically motivated." The stated rationale - replacing non-standard bars dating to the 1920s with modern LBMA-compliant bullion - is technically coherent. But the timing makes it impossible to read as mere housekeeping. France completed this operation during a war in which its principal ally is actively bombing a sovereign nation, publicly threatening to leave NATO, and telling European capitals to provide for their own defence. In that context, selling your gold in your ally's vault and buying replacements in your own is not an operational upgrade. It is a judgement about where sovereign risk now resides.

France is not an outlier. It is the latest in a lengthening procession. Germany attempted to repatriate its gold from the Fed in 2013 and was told the process would require seven years - a delay that ignited persistent, unresolved speculation about whether the physical metal was there to return. The Netherlands quietly moved 122 tonnes home from New York in 2014. Poland, Hungary, Romania, and Turkey have all acted to increase domestic gold holdings in recent years. Central bank gold purchases globally have exceeded 1,000 tonnes in each of the past three years - a pace not seen since the 1960s.

The pattern is unmistakable. The nations that are supposed to trust each other's vaults are methodically emptying them. And the comprehensive audit of US gold reserves at Fort Knox - announced earlier this year to considerable fanfare - has vanished from the public conversation without a result.

Gold was supposed to be the antidote to the trust problem. It is tangible, finite, and carries no counterparty risk in its physical form. But the Hormuz crisis has illuminated a vulnerability that gold's advocates have long glossed over: gold has to sit somewhere. It must be stored in a vault, governed by a jurisdiction, and ultimately protected by a military. The instant you find yourself selling gold in one country's vault in order to repurchase it in your own - just to be certain you actually possess it - you have conceded that gold's neutrality extends only as far as your trust in the institution holding it.

And right now, that trust is running out faster than the gold can be moved.

The Convergence

Three systems of trust are fracturing simultaneously.

The first is physical. The Strait of Hormuz proved that neutral infrastructure - the kind the global economy treats as a permanent given - can be captured overnight and reopened selectively, on the captor's terms. Eighty years of guaranteed passage ended not with a treaty or a battle but with a social media ultimatum.

The second is monetary. Every major government is debasing its currency to manage its debt, and every other government knows it. The mutual knowledge of debasement corrodes the willingness to hold each other's liabilities as reserves. The dollar's supremacy was built on trust in its scarcity. That scarcity is being manufactured away, one Treasury auction at a time.

The third is custodial. France just demonstrated, with $15 billion of conviction, that it does not trust American gold custody. When you cannot trust the vault, you cannot trust the reserve. The oldest and most battle-tested store of value in human civilisation turns out to have a counterparty problem after all.

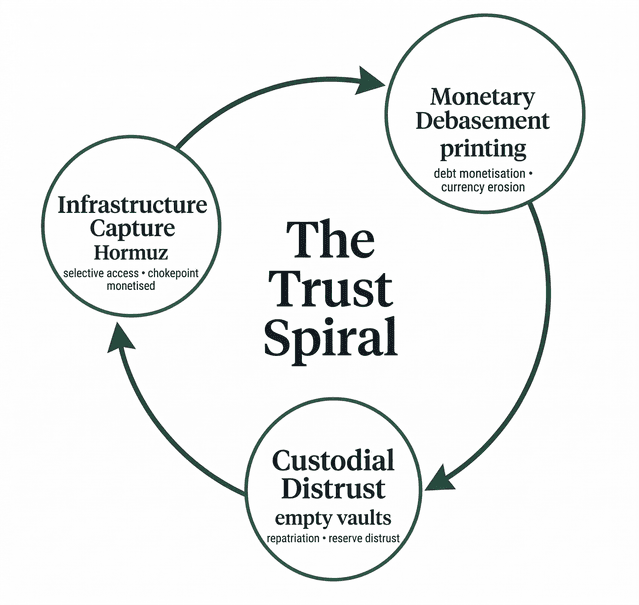

These three failures are not running in parallel. They are recursive. Each one amplifies the others. Debasement makes governments unwilling to hold each other's currency, which drives them toward hard assets. But the custodial failure means hard assets are unreliable unless held domestically. And the infrastructure failure means that even domestic reserves are only as valuable as the trade routes connecting your economy to the world. Trace the spiral with real names. Saudi Arabia considers accepting yuan because it no longer trusts the dollar's purchasing power. China hoards gold because it doesn't fully trust the yuan to hold value. France moves its gold out of New York because it no longer trusts the American vault. And the American vault is being depleted because Washington is draining the Strategic Petroleum Reserve to fight the very war that triggered the trust collapse in the first place. Each actor's rational response to the crisis makes the next actor's position worse. The degradation does not proceed in a straight line. It proceeds in a tightening gyre.

In a unipolar world, these stresses are manageable. A single hegemon can guarantee the waterways, backstop the currency, and underwrite the vaults. But the spring of 2026 has confirmed what many suspected and few wanted to say plainly: we no longer live in a unipolar world. We live in a world where America's treaty allies negotiate oil passage with the country America is bombing. Where France withdraws its gold from the vault of its closest partner. Where the largest coordinated energy intervention in history fails to arrest the price of crude. In a multipolar world, there is no hegemon to guarantee the neutral layer. Which means the neutral layer must guarantee itself.

The Settlement Layer

There is an asset that settles transactions without a chokepoint. It moves across borders without seeking permission from any government. It cannot be frozen, seized, debased, or diluted, because it exists in no vault, answers to no central bank, and obeys no authority other than the mathematics that govern its protocol. Its supply was fixed at inception and will never change. Its rules are enforced by cryptography, not by institutions. And it requires no trust between counterparties because the system was designed, from its first line of code, for precisely the world we now inhabit: one in which trust between counterparties cannot be assumed.

Intellectual honesty demands a nuance: Bitcoin was not immune to this crisis. It flash-crashed 5% in the minutes after the first strikes hit Iran. But within days it had recovered, and within two weeks it had outperformed gold, the S&P 500, and the Nasdaq. By mid-March, Bloomberg was calling it an "oasis of calm." The argument, however, is not about price. It is structural. And the war has demonstrated, with painful clarity, why Bitcoin was invented.

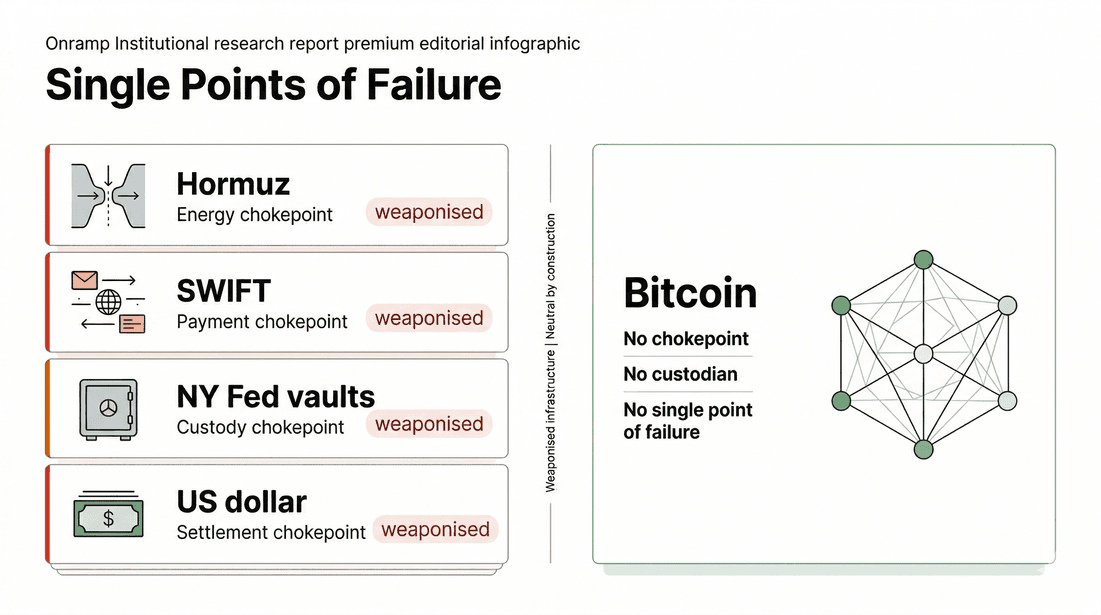

Consider the ledger of the last four years. In 2022, the West weaponised SWIFT to punish Russia — demonstrating that the global payments system has an off switch, and someone's hand is on it. In 2023 and 2024, dollar-denominated sanctions were expanded to secondary targets, proving that the world's reserve currency doubles as a coercive instrument. In 2026, Iran captured the Strait of Hormuz, showing that physical trade infrastructure can be seized and repriced overnight. And now France has emptied its gold from the Federal Reserve's vault, signalling that even the oldest store of value has a custodial vulnerability that allies are no longer willing to tolerate.

Each of these systems - SWIFT, the dollar, Hormuz, the New York Fed - functioned superbly when one power maintained them as neutral infrastructure for the benefit of all. Each became a weapon, or a vulnerability, the moment that power retreated, fractured, or chose a side. Bitcoin has no strait to close. No vault to empty. No single custodian whose allegiance must be maintained. No governing body that can freeze an account, reverse a transaction, or expand the supply. In a world where governments cannot trust each other's waterways, each other's currencies, or each other's vaults, it is the only monetary network on earth that requires no trust between its participants.

When neutral infrastructure is captured, you need infrastructure that is neutral by construction - not by promise. When every currency is being debased, you need money whose supply is governed by mathematics, not by men with printing presses and election cycles. When every settlement system can be weaponised, you need settlement that answers to no sovereign - because in a multipolar world, answering to one sovereign means being distrusted by all the others.

A decade from now, when historians chronicle the moment the international monetary order began its next great transition, they will not point to a white paper or a summit or a central bank communiqué. They will point to the spring of 2026 - when Iran privatised a waterway, France emptied a vault, every major government printed in unison, and the nation that built the post-war order told its allies, on social media, to fend for themselves.

The trust that sustained the old architecture did not shatter in a single dramatic event. It bled out, slowly and from multiple wounds, until the structure could no longer bear the weight it was designed to carry.

What replaces it will not be another government's promise. The world has had its fill of those.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

Bitcoin's Quantum "Threat": Massively Overhyped, Already Being Solved

Headlines warning quantum computers could break Bitcoin by 2029 are everywhere. They're wrong. No quantum computing platform today comes close to the hundreds of thousands to millions of physical qubits required to run Shor's algorithm against Bitcoin's cryptography. Companies routinely stretch the term "logical qubit" beyond recognition. And critically, "harvest now, decrypt later" attacks - the real quantum urgency - don't apply to digital signatures, which is what Bitcoin uses. Even the Federal Reserve got this wrong in a recent paper. The honest timeline for a cryptographically relevant quantum computer: a decade or more, not three years.

What makes this worth covering isn't the threat. It's what Bitcoin developers are doing about a threat that probably doesn't arrive until the mid 2030s. Three separate efforts are underway. BIP-360 proposes a new post-quantum address format (Pay-to-Merkle-Root) that removes exposed public keys from the chain entirely - BTQ Technologies has already launched a live testnet with 50+ miners and 100,000+ blocks processed. Lightning Labs CTO Olaoluwa Osuntokun posted a working prototype on April 8 that solves the hardest governance problem: how to rescue existing wallets if an emergency quantum defence is ever activated. Proof generation takes under 60 seconds on consumer hardware. And SPHINCS+, a hash-based post-quantum signature scheme standardised by NIST, is being evaluated as Bitcoin's long-term replacement for ECDSA.

The real lesson isn't about quantum. It's about how decentralised systems prepare for threats. No committee authorised these efforts. No government mandated them. Individual developers identified a distant risk, built solutions, and published them for peer review, years before the threat materialises. That's the immune system of open-source infrastructure operating exactly as designed.

Mythos Is the Real Threat Ethereum Should Actually Be Worried About

While Ethereum developers draft emergency plans for quantum computers that won't arrive for a decade, the actual existential threat landed on Tuesday. Anthropic's Claude Mythos Preview autonomously discovered thousands of zero-day vulnerabilities across every major OS and browser, including critical flaws in TLS, AES-GCM, and SSH — the cryptographic libraries underpinning DeFi. Ethereum's $200 billion in smart contracts is open-source code, readable by any model that can catalogue every weakness at machine speed. Mythos chains together three, four, sometimes five vulnerabilities into exploits no human auditor would find. Alex Stamos, former head of security at Facebook: "We only have six months before open-weight models catch up in bug finding." At which point every ransomware actor will be able to find and weaponise bugs.

Now notice the conflict of interest in the quantum narrative. The Google paper that generated every "Bitcoin cracked in 9 minutes" headline was co-authored by Justin Drake - an Ethereum Foundation researcher who leads Ethereum's post-quantum team. Within days of the paper's publication, the Ethereum Foundation launched a $2 million post-quantum research prize and a dedicated migration roadmap at pq.ethereum.org. Drake is simultaneously quantifying the threat and building the business case for Ethereum's response to it. Meanwhile, a16z's Justin Thaler argues we are "nowhere near" a cryptographically relevant quantum computer and that the real near-term risks are implementation bugs - not quantum attacks. The quantum narrative provides convenient political cover for the architectural overhaul Ethereum needs - an overhaul that Mythos just made genuinely urgent for entirely different reasons.

Bitcoin doesn't have this problem. Its script language is deliberately minimal. It doesn't run Turing-complete smart contracts. The attack surface is tiny by design. Satoshi's most underappreciated contribution wasn't proof of work or the 21 million cap. It was knowing what to leave out.

AI & Financial Infrastructure

Meta Abandons Open Source. The AI Arms Race Just Got Real.

On April 8, Meta debuted Muse Spark - the first model from Meta Superintelligence Labs, the AI division run by former Scale AI CEO Alexandr Wang, hired nine months ago for $14.3 billion. The model is proprietary. Not open-source. Not "open-weight." Proprietary.

This is a seismic shift. Meta spent three years positioning Llama as the open-source counter to OpenAI and Google. Zuckerberg built an entire narrative around democratising AI. That narrative died on Wednesday. Muse Spark matches the capabilities of Meta's older mid-size Llama 4 models for "an order of magnitude less compute," which tells you something important about what's being kept behind the wall. If they can achieve parity at 10x less cost, the frontier version is operating at a level they've decided is too valuable to share.

Meta's AI capex for 2026: $115-135 billion - nearly double last year. The open-source era of frontier AI may be ending. When the three largest AI labs (OpenAI, Anthropic, Google) and now the company that championed open models are all going proprietary, the message is clear: the next generation of intelligence is too valuable to share. For allocators: the infrastructure moat just widened. Companies without access to frontier models will be locked out of the capability curve entirely.

The 100x Energy Fix: Why Tufts Just Changed the AI Infrastructure Math

Tufts University researchers published a proof-of-concept AI system that reduces energy consumption by 100x while improving accuracy. The approach - neuro-symbolic AI, combining neural networks with human-like symbolic reasoning - is a category breakthrough, not an incremental improvement.

AI currently consumes over 10% of US electricity, and the IEA projects demand will double by 2030. Every major hyperscaler is scrambling to secure power for data centres. Microsoft signed the Three Mile Island deal. Amazon is buying nuclear sites. Google is deploying geothermal. The assumption underpinning hundreds of billions in infrastructure investment is that bigger models require more power, full stop.

The Tufts result suggests an entirely different path: instead of more power for bigger models, fundamentally more efficient architectures. If neuro-symbolic approaches scale - a significant "if" - the trillion-dollar race to secure energy for AI could decelerate sharply. That would be deflationary for AI infrastructure costs and massively bullish for AI adoption in the developing world, where power constraints have been the binding limitation. The paper is peer-reviewed and the methodology is reproducible. This isn't a press release. It's a proof of concept that challenges a fundamental assumption of the current AI investment thesis.

MCP Crosses 97 Million Installs. You Should Know What That Means.

Anthropic's Model Context Protocol - the standard that lets AI agents connect to external tools, databases, and services - crossed 97 million installs in March. Every major AI provider now ships MCP-compatible tooling. This is the moment MCP stopped being an experimental protocol and became foundational infrastructure for the agentic economy.

Think of it as the HTTP of AI agents: the standard that makes interoperability possible. When your AI agent books a flight, queries a database, files an expense report, and sends a Slack message in a single workflow, MCP is the plumbing underneath. For those tracking the machine economy thesis from our March 24 edition (Stripe MPP, Visa CLI, Coinbase x402): MCP is the connective tissue that makes all of it work together.

The 97 million number means the developer community has voted. The standard has won. What remains is execution - and the companies building on MCP today will have the same structural advantage that early web companies had by building on HTTP in 1995. The infrastructure layer is being decided now, and it's being decided quietly, while the headlines focus on model benchmarks and valuation rounds.

Geopolitics & Markets

Islamabad Failed. The Blockade Is Live. The War Just Entered a New Phase.

The ceasefire announced April 7 unravelled within hours. Iran re-closed the Strait after Israel struck Lebanon. Only four tankers transited on April 8. By Friday, Vice President Vance was en route to Islamabad for the highest-level direct US-Iran meeting since 1979 - a 300-person US delegation facing 70 Iranian negotiators across 21 hours of marathon talks at the Serena Hotel.

They failed. Vance said Iran refused to commit to abandoning its nuclear programme. Iran's Foreign Minister Araghchi said they were "inches away" from a memorandum of understanding before encountering "maximalism, shifting goalposts, and blockade."

The sticking points: nuclear enrichment, Hormuz sovereignty, and Iran's demand that the ceasefire include Lebanon - which Israel explicitly rejected.

Trump's response was immediate and unprecedented. At 10am ET on Monday, the US Navy imposed a full blockade of all Iranian ports and coastal areas, including traffic through the Strait of Hormuz.

CENTCOM clarified it will intercept vessels entering or leaving Iranian ports but "will not impede freedom of navigation for vessels transiting to and from non-Iranian ports." Iran's armed forces called it "piracy" and warned of a "decisive response."

Oil surged back above $100. No allies have joined the blockade - Britain explicitly refused, and France announced plans for a separate "peaceful multinational mission" to restore freedom of navigation. The UN Secretary General said "no one should do anything that harms freedom of navigation in the Strait." The ceasefire technically expires April 21. But with a US naval blockade now operational, the distinction between ceasefire and active conflict is increasingly academic.

March CPI: The Oil Shock Hits the Data

March CPI came in at 3.3% year-over-year - up from 2.4% in February, the largest single-month acceleration since 2022. Month-over-month, prices rose 0.9%, driven almost entirely by gasoline. Real average hourly earnings fell 0.6% - workers are losing purchasing power in real time. But look underneath the headline. Core CPI - stripping out food and energy - rose just 0.2% for the month and 2.6% over the year. That's actually decelerating. The oil shock hit exactly where expected and hasn't yet broadened into services and shelter. This is the split the Fed has to navigate: headline inflation screaming at 3.3% says hold or hike; core cooling to 2.6% says the underlying economy isn't overheating. For now, the Fed will likely stay frozen. But if Brent stays above $95 through Q2, headline prints will keep climbing - and the distinction between "transitory energy shock" and "entrenched inflation" will get harder to maintain with every passing month.

The Insurance Problem Nobody Is Talking About

The Islamabad talks collapsed. A US naval blockade is now live. And even before this week's escalation, large-scale shipping through Hormuz wasn't coming back because insurance had already collapsed. War-risk coverage for Gulf-transiting tankers was pulled entirely on March 5, and premiums had quadrupled before that. 230 loaded oil tankers are sitting inside the Gulf with nowhere to go.

Lloyd's of London and the protection and indemnity clubs that underwrite global shipping need binding commitments and stable conditions - not a ceasefire that frayed in 24 hours, followed by failed negotiations, followed by a naval blockade. The IEA, World Bank, and IMF issued a joint statement this week warning there will be "no quick relief for high fuel and fertiliser prices even after a resumption of regular shipping flows." Reconstruction of damaged regional energy infrastructure alone will take months. Rystad estimates the bill at $25 billion or more — including the Ras Laffan LNG facility in Qatar, which has lost 17% of export capacity. Saudi Arabia has reported 600,000 barrels per day of lost production capacity from strikes on its own facilities.

This is the bottleneck that outlasts every headline. Diplomacy can pause a war. It cannot rebuild an insurance market overnight.

The Week in Numbers

| Indicator | Reading |

|---|---|

| Brent crude (WTI ~$99) | ~$100 |

| Bitcoin | ~$74K |

| March CPI (up from 2.4%) | 3.3% |

| MSBT day 1 | $34M |

| War duration | 45 days |

| Stuck in the Gulf | 230 tankers |

| MCP installs | 97M |

| Meta AI capex | $115-135B |

What to Watch This Week

| Date | Event | Why it matters |

|---|---|---|

| Apr 13 | CLARITY Act Banking Committee markup | Senate returned Apr 13. Markup targeted for this week or next. Five legislative steps remain. |

| Apr 14 (Tues) | JPMorgan, Goldman Q1 earnings | Dimon's tone on consumer credit and the oil shock sets risk sentiment. Goldman's deal backlog signals M&A appetite. |

| Apr 21 | Ceasefire two-week deadline | Either extended, formalised, or collapsed. Oil reprices accordingly. |

| Apr 29 | FOMC meeting | March CPI at 3.3% just killed any rate cut hopes. 98.4% of CME FedWatch expects a hold. |