May 19, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

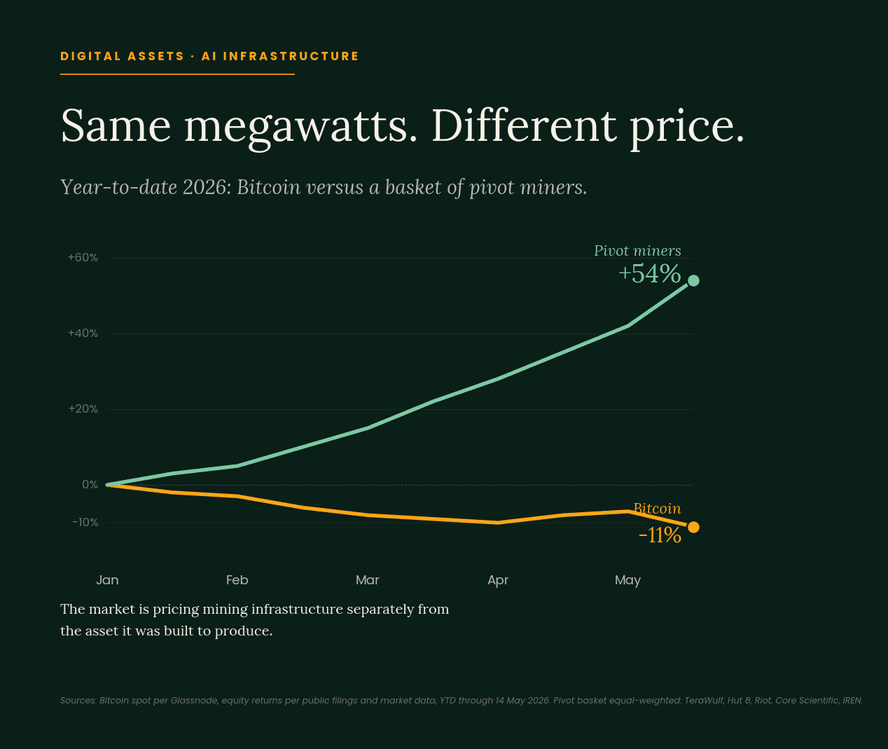

Bitcoin mining produced, as a side effect, the most valuable energy infrastructure portfolio outside the utility sector. The market is now revaluing that infrastructure based on its highest use, which is no longer hashing.

Bitcoin miners spent ten years building the only proven business model for monetising stranded power. AI just discovered the same megawatts are worth more in a server rack than in an ASIC. The pivot is being reported as bearish for Bitcoin. The structural read is the opposite.

The Megawatt Premium

What happened

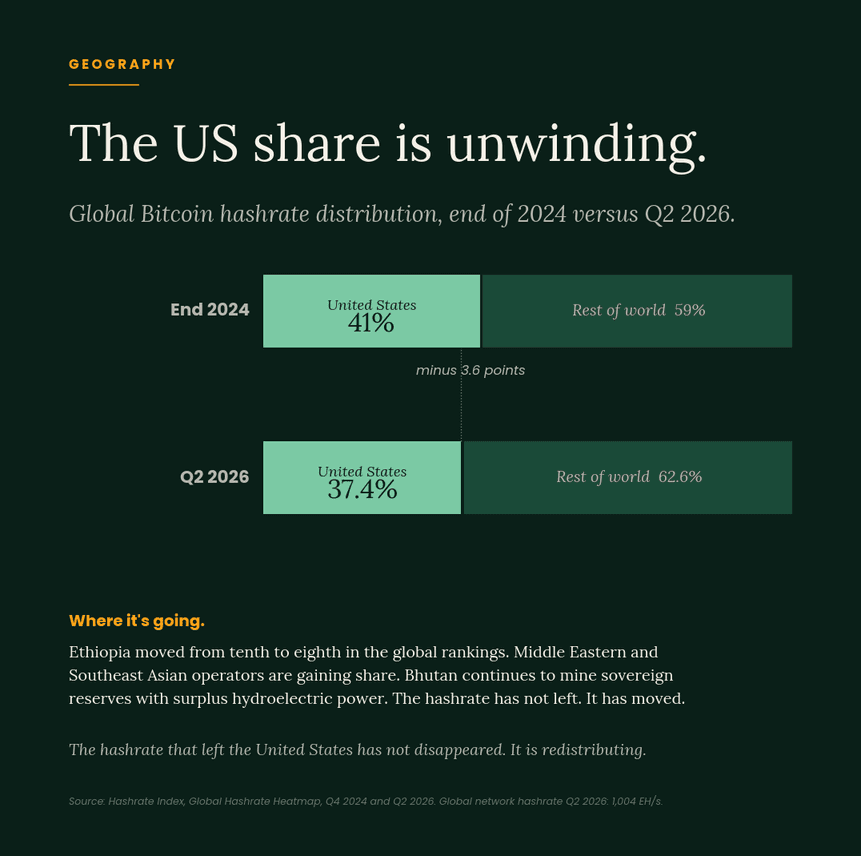

For the first quarter of 2026, Bitcoin network hashrate fell. Down 4% year-to-date, the first first-quarter decline since 2020. The Q2 figure was worse, down 5.8% quarter-on-quarter to 1,004 EH/s. The protocol has issued six downward difficulty adjustments in 2026, reducing total difficulty by 10.7% from the start of the year.

The US share of global hashrate, which had risen from 35% in 2021 to over 40% by end-2024, fell to 37.4% by Q2 2026.

Bitcoin trades at ~$80,000. Production costs across the public miner cohort sit closer to $90,000. The 2024 halving cut block rewards in half. Power costs rose. The math stopped working for marginal operators.

The longer explanation is the interesting one. Mining did not just stop being profitable. AI started being more profitable, on the same infrastructure, for the same operators.

The deal stack

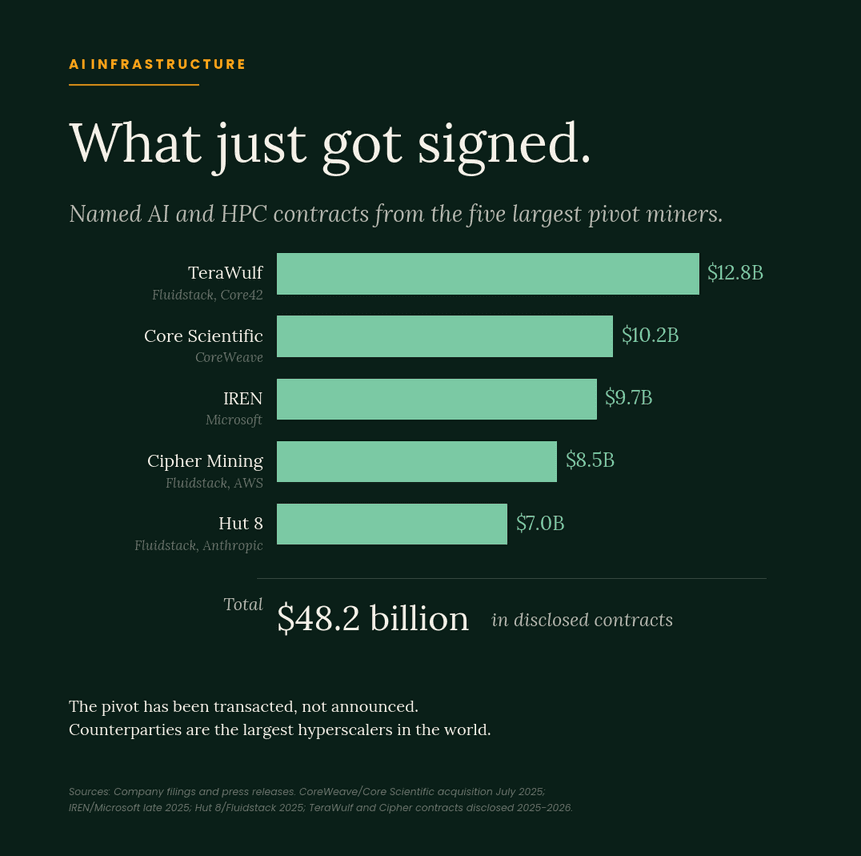

More than $70 billion in AI and HPC contracts have been announced by Bitcoin miners.

CoreWeave acquired Core Scientific in an all-stock transaction valued at approximately $9 billion in July 2025. Core Scientific has since said its mining operations will continue winding down through 2026, with only one or two of its ten sites still operational for Bitcoin mining by year-end. IREN signed a $9.7 billion contract with Microsoft for 76,000 GB300 GPUs across 200 megawatts in Texas. Hut 8 signed a $7 billion fifteen-year contract with Google-backed Fluidstack, with Anthropic among the named counterparties. TeraWulf has locked in $12.8 billion across deals with Fluidstack and Core42. Cipher Mining secured $8.5 billion, with Google taking a 5.4% equity stake via warrants on the Fluidstack contract.

CoinShares projects 70% of public miner revenue will come from AI by the end of 2026, up from roughly 30% a year earlier.

What is actually being sold

The miners are not selling their hashing capacity. They are selling their power infrastructure: substations, grid interconnects, cooling, PPAs, gigawatt-scale agreements with utilities.

New utility-scale grid interconnects in the United States have lead times of five to seven years. AI demand cannot wait, and the Bitcoin mining industry owns most of the gigawatts that already exist. Bitcoin miners are the option value on the entire AI buildout. That option just got exercised.

The market has already priced this

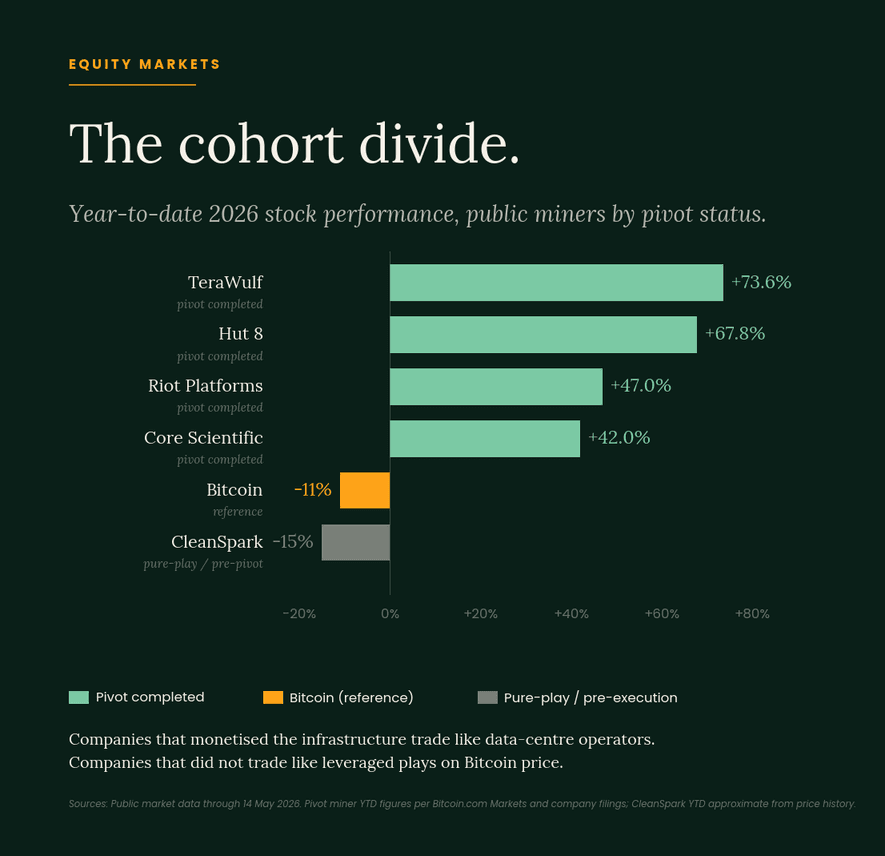

Three distinct cohorts have emerged.

The pivot miners trade on AI infrastructure multiples. TeraWulf is up 73.58% year-to-date. Hut 8 up 67.75%. Riot up 47%. Core Scientific up over 40%. IREN, the most aggressive pivot, derives 90% of its valuation from AI and HPC contracts.

The pure-plays are tracking Bitcoin downward. CleanSpark, the largest US-listed miner without an executed AI contract, trades at roughly $11.50, down approximately 62% from its 52-week high. Q2 FY2026 net loss of $378.3 million, nearly triple the prior year. Revenue down 25% year-on-year. The company has 1.8 GW under contract but is only utilising 808 MW.

Management language has shifted to "multi-gigawatt AI tenancy" and "hyperscale customer discussions" but no contracts are signed. American Bitcoin is doubling down on pure mining, pledging 3,090 Bitcoin to Bitmain as collateral for new ASICs. Bitdeer was downgraded by KBW in January, price target cut from $26.50 to $14.

The market is pricing the infrastructure separately from the asset it was built to produce. Companies that have monetised the infrastructure trade like data centre operators. Companies that have not trade like leveraged plays on Bitcoin price.

What it means for Bitcoin

Three structural consequences.

Network security improves through geographic redistribution. As US power prices rise on AI demand, mining migrates to wherever stranded electrons remain cheap. Ethiopia has moved up to eighth in the global rankings. Middle Eastern and Southeast Asian operators are gaining share. Bhutan continues to mine sovereign reserves using surplus hydroelectric power. Greater geographic distribution is a security feature. The 2021 China ban was a stress test the network survived precisely because the failure mode was geographic concentration. The unwinding of US concentration redistributes the network's physical footprint.

The forced-selling dynamic that ended every previous Bitcoin cycle has been structurally weakened. Miners with mixed-use infrastructure now have an alternative revenue stream that does not depend on Bitcoin price. When mining economics deteriorate, megawatts can be reallocated to AI compute, which pays in stable, contracted, multi-year cash flows. The infrastructure base no longer needs to be liquidated. Miners can ride out Bitcoin drawdowns without being forced to sell. The most reliable source of forward-selling pressure during bear markets has been removed.

Network security is denominated in cost-of-attack, not raw hashrate. As AI demand bids up the price of electricity, the marginal cost of mining a block rises. So does the marginal cost of attacking the network. The two move together. The security ratio does not change. The miners that remain are the most efficient operators with the cheapest stranded power. The category consolidates around elite siting.

What to watch

US hashrate share. If it falls below 30% in the next twelve months, geographic distribution has reached levels not seen since 2021.

International growth in Ethiopia, Paraguay, Oman, and the Gulf. The hashrate that leaves North America has to go somewhere.

The CleanSpark trajectory specifically. The largest remaining pure-play. If management executes a hyperscaler contract in 2026, the cohort divide closes. If it does not, the divide widens, and the market signal becomes definitive.

Curtailment credits from miners operating as flexible load. Riot earned $6.2 million in December 2025 alone. As the dual-revenue model matures, curtailment credits become a third revenue stream alongside mining and AI hosting.

The unwritten conclusion

The pivot is being treated as a story about Bitcoin's weakness. The framing is upside down. Bitcoin mining produced, as a side effect, the most valuable energy infrastructure portfolio outside the utility sector. The market is now revaluing that infrastructure based on its highest use, which is no longer hashing.

Bitcoin gets a more distributed network, a structurally weaker forced-selling dynamic, and a miner cohort that is both better capitalised and more resilient. The hyperscalers get a path to the gigawatts they need on a timeline they can deliver. The miners get paid for the infrastructure they built rather than only for the Bitcoin it produced.

The premium was always on the megawatt. The miners just took a decade to figure that out, and another year to collect it.

Sources

Hashrate Index, Global Hashrate Heatmap Q2 2026. Glassnode, Bitcoin network hashrate and difficulty data. JPMorgan, Bitcoin mining sector update, January 2026. CoinShares, public miner revenue projections, Q1 2026. CoreWeave press release, Core Scientific acquisition, July 7 2025. IREN, Hut 8, TeraWulf, Cipher, MARA, Riot, CleanSpark, American Bitcoin, Bitdeer SEC filings 2025-2026. KBW research notes on mining sector, January 2026. TheEnergyMag Miner Weekly, May 2026.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

CLARITY clears the committee that killed it for four months.

The Senate Banking Committee passed the Digital Asset Market Clarity Act 15-9 on Thursday May 14, with Senators Gallego and Alsobrooks crossing the aisle. The Tillis-Alsobrooks stablecoin compromise survived 8,000 American Bankers Association letters in the final week. Van Hollen's ethics amendment failed 11-13 and now becomes the floor fight that decides Democratic support against the 60-vote threshold. White House adviser Patrick Witt is targeting a presidential signature by July 4. Five legislative steps remain: floor vote, reconciliation with the Agriculture Committee version, reconciliation with the House-passed July 2025 text, and signature. The deadlock that has held the bill since December is finally broken, and the timeline that survives this committee passage is the one institutional capital will underwrite product roadmaps against.

Bhutan went from third-largest sovereign holder to almost nothing.

Arkham Intelligence data shows Druk Holding and Investments, the Kingdom of Bhutan's sovereign wealth fund, has moved approximately 9,900 BTC since mid-2025. Sovereign holdings have declined from roughly 13,000 BTC to 3,119 BTC. The Bhutanese government denies selling and has not addressed specific wallet movements, despite years of undisputed Arkham attribution. The remaining stack will not cover Bhutan's public pledge of 10,000 BTC to seed the Gelephu Mindfulness City economic zone. At current outflow rates the reserve runs out by October. The third-largest sovereign Bitcoin holder has, on the on-chain data, become one of the largest sovereign Bitcoin sellers. The transparency advantage that distinguished sovereign Bitcoin holdings from sovereign gold reserves has just been demonstrated to cut both directions.

Saylor signals what he said for five years he would never signal.

On the Q1 earnings call on May 5, Executive Chairman Michael Saylor told investors: "We will probably sell some Bitcoin to fund a dividend just to inoculate the market, just to send the message that we did it." CEO Phong Le told CNBC the same day that the trigger for sales would be when Strategy's mNAV falls below 1.0. The current mNAV is 1.22. The company carries 818,334 BTC at an average cost of $75,532. Bitcoin closed Monday at $77,119. The buffer between Saylor's five-year public commitment never to sell and his Q1 commitment to sell when the wrapper inverts is roughly $2,000 per coin. With volatility now elevated by Iran headlines, that buffer is a single session move.

Strive ships the first daily-dividend preferred in capital-markets.

Strive Inc. will pay dividends on its SATA preferred stock every business day from June 16, at an annualised 13.00%. CEO Matthew Cole called it a "true zero-to-one innovation. The product compresses the duration of investor capital from monthly to daily and exists for the same engineering purpose as Strategy's parallel semi-monthly STRC shift: keep the preferred trading at par regardless of what Bitcoin does underneath. The arms race is no longer about who can accumulate the most Bitcoin. It is about who can engineer the most stable income wrapper around it. Allocators who underwrote 11.5% monthly dividends are about to underwrite 13.0% daily ones from a smaller, more fragile issuer. The credit market this cohort is building did not exist in 2024.

Satsuma becomes the first treasury company to be forced to unwind.

Pantera Capital, holding roughly 7% of London-listed Satsuma Technology, formally requested a return of capital on April 23. Satsuma's market capitalisation has fallen below the value of its 646 Bitcoin, the structural signal that an accumulator has stopped functioning as a premium-bearing equity proxy and started functioning as a closed-end fund trading at a discount. Empery Digital is already selling Bitcoin to fund share buybacks, having sold 20 BTC at an average $74,425 to repurchase shares at $5.71 against a 52-week high of $44.09. Two different vehicles, same mechanism: the wrapper inverts and becomes a seller of the asset it was built to hold. The next twelve months separate treasury structures that absorb capital from those that get absorbed by it.

AI & Financial Infrastructure

Transformer lead times extend to four years.

PwC's May 11 analysis confirms that high-capacity transformer lead times have stretched from a historical 12-18 months to as long as 48 months. The constraint is no longer chip allocation or capital. It is the steel, copper, and grain-oriented silicon steel required for the mundane physical hardware that connects a data centre to the grid. China controls approximately 60% of global transformer production, a dependency the US Commerce Department has flagged as strategic. Even with unlimited capital, the OpenAI Stargate Project, announced last autumn at $500 billion and backed by SoftBank's $40 billion loan commitment, has shown no significant physical progress as of April 2026. The bottleneck has migrated from the server rack to the substation, and no hyperscaler balance sheet can compress a four-year delivery schedule into eighteen months.

The Microsoft backlog has grown larger than the GDP of Sweden.

Microsoft's commercial cloud bookings backlog hit $627 billion at Q3 close, up 99% year-over-year. CFO Amy Hood used the phrase "capacity-constrained" three times on the earnings call. Azure revenue grew 40%. The AI business hit a $37 billion annualised run rate, up 123%. The company has booked $627 billion of orders it cannot fulfil because the equipment to fulfil them does not yet exist. For allocators, this inverts the cycle that ran from 2023 to 2025: demand is no longer the question. Supply is. The companies that win this leg of the trade are not those guiding to the largest capex numbers, but those that already control the scarce physical inputs that the capex is trying to acquire.

Two-thirds of AI data centre announcements are still PowerPoints.

Sightline Climate's April analysis of 140 US data centre projects with 2026 opening dates: 16 GW of computing capacity announced, only 5 GW under construction. The remaining 11 GW exists as press releases with zero visible build progress, despite data centres typically requiring 12-18 months of construction time. Between 30 and 50 percent of the 2026 pipeline will slip into 2027, 2028, or die entirely. Fermi America, the Trump-branded developer, disclosed in mid-April that its 1.1 GW 2026 target is no longer achievable. The press-release timeline and the steel-and-copper timeline have decoupled, and the divergence is now measurable at company-by-company level. The AI infrastructure trade has become a supply-chain audit.

Hyperscalers commit $650B and stocks fall on the announcement.

Combined 2026 capex from Meta, Microsoft, Alphabet, and Amazon now sits between $650 and $700 billion, every one of them raised from prior guidance. Meta lifted its range to $125-145 billion and the stock fell 6% after-hours. Microsoft raised to $190 billion, attributing part of the increase explicitly to memory pricing. Alphabet raised to $180-190 billion with 2027 signalled "significantly higher." Amazon held at $200 billion. The market punished the spending despite the revenue confirmation because the supply chain has become the binding variable. For the first time in this cycle, larger capex announcements no longer translate to larger forward earnings expectations. Capital is no longer the moat; component access is.

Custom silicon goes from optionality to imperative.

High-bandwidth memory is sold out across Samsung, SK Hynix, and Micron through year-end 2026, the new constraint that did not exist twelve months ago. Component prices are rising. Meta's MTIA, Google's TPU v6, and AWS Trainium 2 are all scaling to production volumes in 2026 that put each hyperscaler within reach of internal silicon serving a meaningful share of inference workloads. The chips are not faster than Nvidia's. They are available, owned, and not subject to allocation queues that depend on a single vendor's manufacturing partner. The trade is not over. Its character is changing. The structural beneficiaries of the AI cycle, including Nvidia, TSMC, and the HBM trio, face a buyer base actively reducing dependence on them.

Geopolitics & Markets

April CPI: 3.8%, the highest since May 2023.

Headline CPI accelerated from 3.3% in March to 3.8% in April, the largest two-month jump since 2022. Energy rose 17.9% year-over-year. Gasoline up 28.4%. Fuel oil up 54.3%. Core CPI at 2.8% remains contained but is no longer falling. Shelter rose 0.6% month over month, still the stickiest component. The CME FedWatch tracker now prices essentially zero probability of rate cuts through 2027, and the implied probability of a hike before year-end has risen to 40%. This is the print that retired the rate-cut thesis for 2026. The remaining question is whether the Fed simply holds against persistent 3-4% inflation or whether Warsh signals tightening in the middle of an energy-driven supply shock he did not create.

Warsh confirmed 54-45, the closest Fed Chair vote in modern history.

Kevin Warsh was confirmed as the 11th Fed Chair of the modern banking era on Wednesday May 13, on a vote that broke almost entirely along party lines. Only Senator Fetterman crossed. Warsh has previously called the 2022-2023 inflation episode "the Fed's biggest policy mistake in four decades" and has consistently advocated for monetary policy to support productive investment cycles. Powell remains on the Fed Board of Governors as Vice Chair, the first chair to do so in nearly 80 years and a deliberate institutional check on political pressure. Warsh's first FOMC meeting is June 16-17. He will inherit a Fed holding rates at 3.50-3.75% against 3.8% headline CPI and a market pricing both no cuts and a 40% chance of a hike. The bond market has already begun pricing his arrival.

30-year Treasury yields hit 5.12%, highest since October 2023.

The 30-year jumped 11 basis points on Friday May 15 to 5.121%, the highest level in over two and a half years. The 10-year sits at 4.6%. The 2-year at 4.08%. The yield curve is flattening from the long end as the market raises its terminal rate expectations. The April Treasury budget surplus was 17% below the same month in 2025, and $97 billion of monthly federal spending now goes to debt service alone, second only to Social Security. Spiking yields are not confined to the US. German bunds at 3.13%, Japanese 10-year at 2.69%, UK gilts at 4.56%. Duration is being repriced globally on the same thesis: structurally higher inflation, structurally higher fiscal deficits, structurally less central bank willingness to suppress either.

Trump rejects Iran's latest counterproposal as "totally unacceptable".

Iran's 14-point peace offer of May 5 was followed by a revised counter on May 10 demanding war reparations, full sovereignty over the Strait of Hormuz, sanctions lifted, and frozen assets released, with nuclear negotiations deferred to later stages. Trump rejected it Sunday on Truth Social: "TOTALLY UNACCEPTABLE." Vice President Vance's planned trip to Islamabad for resumed talks was cancelled. The ceasefire that began April 7 is now described by the White House as on "massive life support." The blockade remains in place at 76 days. The US has fired on two Iranian tankers attempting to breach the blockade, killing at least one sailor. The diplomatic theatre and the kinetic conflict are now running in parallel, with neither containing the other.

UAE nuclear facility struck; Brent at $108 on May 18 escalation.

Energy infrastructure across the Persian Gulf came under attack over the weekend including a nuclear facility in the United Arab Emirates, the first such target of the war. Brent traded between $107 and $111 on Monday after Trump's overnight Truth Social post warning that for Iran "the clock is ticking, and they better get moving FAST, or there won't be anything left of them." The post triggered $657 million in crypto liquidations within hours and broke Bitcoin through $80,000 support to $77,119. Brent is now up over 60% since the war began on February 28. The IEA warned Monday that global oil inventories are declining rapidly, with stockpiles projected to fall from 101 days of demand cover to 98 days by end of May. Markets are no longer pricing peace; they are pricing the gap between rhetoric and execution.

The Week in Numbers

| Indicator | Reading |

|---|---|

| Bitcoin (-4.87% wk) | $77,119 |

| Brent crude | $107.71 |

| April CPI YoY | 3.8% |

| 30Y Treasury | 5.12% |

| CLARITY committee vote | 15-9 |

| Warsh confirmation | 54-45 |

| Bhutan outflows | 9,881 BTC |

| Strategy mNAV / trigger | 1.22 / 1.00 |

What to Watch This Week

| Date | Event | Why it matters |

|---|---|---|

| May 20 (Wed) | FOMC minutes from April 28-29 meeting | Last set of Powell-era minutes. Reveals the internal debate before April CPI confirmed the energy passthrough into core. |

| May 21 (Thu) | Memorial Day recess deadline | Effective last working day before two-week recess. CLARITY merge with Agriculture Committee text needs to start the moment Senate returns. |

| May 27 (Tue) | Strategy and Strive AGM votes | Strategy shareholders vote on semi-monthly STRC. Strive's daily-dividend mechanic begins June 16. Two different answers to the same wrapper problem. |

| Jun 10 (Wed) | May CPI release | First full month with Brent above $100. If headline holds at 3.8% or pushes higher, the 40% hike probability priced into futures becomes the consensus. |

| Jun 16-17 | Warsh's first FOMC | Warsh inherits a Fed that holds 3.50-3.75% against 3.8% headline CPI. Whatever he says in the press conference resets every duration trade in the world. |