May 26, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

Five separate policy mechanisms are being assembled into a single architecture of financial repression: a Fed-Treasury absorption channel that anchors nominal yields below inflation and liquidates federal debt in real terms, just as the 1946-1974 precedent did.

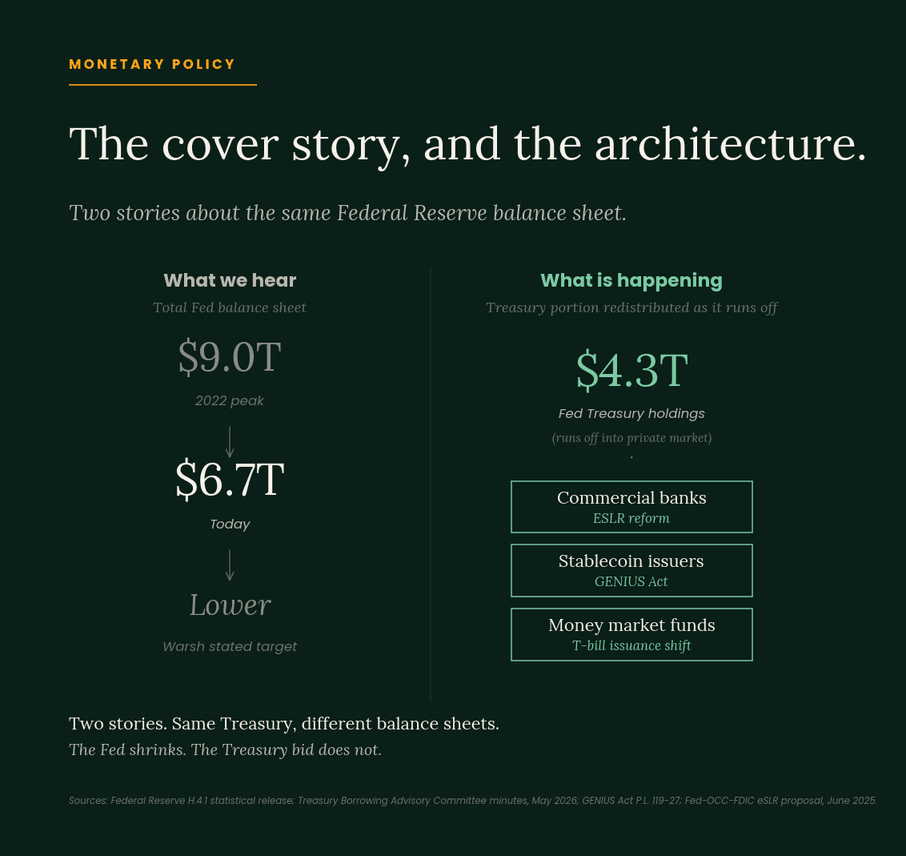

Kevin Warsh wants to shrink the Federal Reserve's balance sheet. He has said so publicly for years. He said so again at his April 21 confirmation hearing. He has been Chair for eleven days, and the agenda is now policy. The Fed's total balance sheet currently stands at $6.7 trillion, of which $4.3 trillion is Treasury securities and $2.0 trillion is mortgage-backed securities. Every dollar of the Treasury holding the Fed declines to reinvest as it matures has to be refinanced by the Treasury Department and absorbed somewhere else in the private market. The architecture being assembled to absorb it is visible across five separate institutions and pieces of legislation. The components have not been put together publicly. They should be.

The Financial Repression Architecture Is Being Built

Warsh's cover story

Warsh's balance sheet position is the most consistent stated view in his policy record. At his confirmation hearing he was unusually candid about what he believes the central bank's holdings have done: "As it's grown its balance sheet, grown its imprimatur on the economy, those with financial assets have benefited. If we were to cut rates, a broader number of people will benefit from it, versus quantitative easing, which tends to move through financial assets first."

The candour is worth pausing on. Warsh has acknowledged that quantitative easing functioned as a transfer mechanism to asset holders, and is proposing rate cuts as a more politically palatable alternative. Fortune's analysis of his hearing captured the trick: Warsh "wants to reduce the balance sheet, currently standing at $6.7 trillion, and conveniently delivers another neat argument for rate cuts without raising alarm bells over questions of Fed independence."

The $6.7 trillion total includes the $4.3 trillion in Treasuries and $2.0 trillion in mortgage-backed securities. The architecture this piece describes is the absorption mechanism for the Treasury portion specifically. The MBS portion runs off into a different market and creates a different problem.

The Bitcoin community's reception of Warsh has been broadly positive, but for reasons orthogonal to the balance sheet position itself. He has personal equity in the digital asset ecosystem. He has called Bitcoin a sustainable store of value. He has consistently advocated for lower short-term rates. The rate cut signal is what the community is welcoming. The balance sheet shrinkage is treated as the procedural cover that makes the rate cuts politically possible: if you can claim the balance sheet is being tightened, you can cut the short end without raising independence concerns.

Michael Howell at Capital Wars framed the more accurate read in February. This is the Warsh Pivot from Fed QE to Treasury QE, not from QE to no QE. The balance sheet shrinkage is not hawkish. It is a redistribution of the absorption channel.

The mechanism works through runoff. When a Treasury security matures on the Fed's balance sheet and the Fed declines to reinvest, the Treasury Department has to refinance the maturity with new issuance into the market. The market then has to find a buyer. The $4.3 trillion Treasury portfolio on the Fed's books is therefore not just a static holding. It is a continuous stream of refinancing pressure on the private market for as long as Warsh shrinks. Five separate mechanisms are being assembled to ensure the private market absorbs it without a real-yield premium.

The architecture

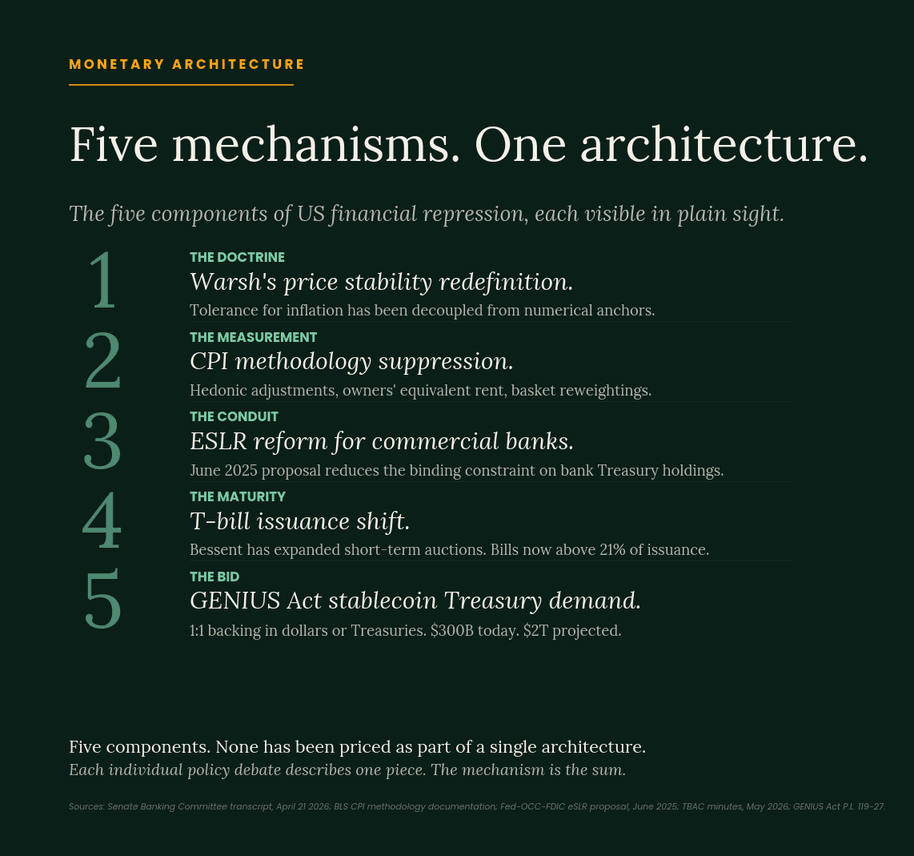

The doctrine. Warsh's stated goal at the April 21 hearing was "regime change" at the Federal Reserve. He wants to abandon forward guidance and the dot plot. He has redefined price stability as "a change in prices such that no one's talking about it." The redefinition is the tell. The old 2% PCE anchor required actual measured outcomes to be tolerated. The new framing requires only that the measured outcomes not generate political or financial market attention. Tolerance has been decoupled from numbers.

The doctrine has a companion justification. In a November 2025 Wall Street Journal op-ed and repeatedly since, Warsh has argued that "AI will be a significant deflationary force, increasing productivity and strengthening US competitiveness." At the April 21 hearing he stated that "inflation is a choice, and the Fed must take responsibility for it." Read together, these positions allow the Federal Reserve to cut the policy rate before measured inflation falls, justified by the claim that AI productivity will push prices down on a forward basis. The policy lever moves first. The measured inflation falls (or does not) later. Markets are openly sceptical. Fed funds futures now price a 2026 rate hike as more likely than a cut. The 10-year Treasury yield closed at 4.61 percent on May 18, the highest in a year. The architecture does not require market consent. It requires policy execution.

The measurement. CPI methodology has shifted measured inflation structurally below experienced inflation for years. Hedonic adjustments treat quality improvements as price reductions. Owners' equivalent rent, one third of the basket, is imputed from a survey of landlords rather than observed transaction prices. Geometric mean substitution lets consumers be assumed to switch to cheaper alternatives. Basket reweightings update annually. Each individual adjustment has technical justification. The cumulative effect is that the rate the Fed targets is not the rate households experience. When Warsh defines price stability as a change in prices "such that no one's talking about it," the measurement system has already been tuned to ensure fewer people are talking about it.

The conduit. In June 2025 the Fed, OCC, and FDIC jointly proposed replacing the 2% enhanced supplementary leverage ratio buffer for global systemically important banks with a capital charge equal to half of the bank's GSIB surcharge. The proposal invited public comment on exempting trading Treasury securities held by GSIB broker-dealer subsidiaries from the leverage calculation entirely. Treasury Secretary Bessent has publicly supported the reform. The mechanism: even without a full Treasury exemption, the proposal reduces the binding capital constraint on banks holding Treasuries. Commercial banks are being prepared to absorb the runoff the Fed declines to reinvest.

The maturity. Bessent has expanded T-bill auctions to record levels. He has stated publicly that Treasury does not plan to increase auction sizes for longer maturities. T-bills currently sit above 21 percent of total issuance, above the 20 percent target the Treasury Borrowing Advisory Committee recommends. Standard Chartered projects that raising the bill share by 2.5 percentage points over three years would create approximately $900 billion in additional bill supply, which "could effectively suspend 30-year auctions for three years." The May 5 TBAC minutes flagged a $1.3 trillion funding shortfall projected in fiscal years 2027 and 2028 based on current sizes. Maturing MBS proceeds on the Fed's balance sheet are already being reinvested directly into bills. The maturity of US debt is being shortened deliberately. Short-term debt requires short-term holders. Bills suit money market funds, banks, and stablecoin issuers. Long bonds do not. The maturity shift also locks the absorbed debt at the part of the curve the Federal Reserve directly controls. T-bill yields move with the policy rate by construction. When Warsh cuts, the entire absorbed stack reprices lower the same day.

The bid. The GENIUS Act, passed July 2025, requires payment stablecoins to be backed 1:1 in dollars or US Treasury securities. Every dollar of stablecoin supply growth equals roughly a dollar of new Treasury demand. The total stablecoin market sits above $300 billion. Standard Chartered projects $2 trillion. That implies roughly $1.7 trillion in additional structural Treasury demand from this channel alone over the coming years. Yield-bearing variants drove more than half of stablecoin growth in Q1 2026 through sister-token wrappers that route Treasury yield to holders. The CLARITY Act being debated this week is intended to close that loophole. The point of the prohibition is structural. If stablecoin issuers can pay yield, holders extract the Treasury yield. If they cannot pay yield, the issuer captures the yield and the Treasury bid is locked in. Either way, the yield that holders or issuers earn is the T-bill yield, which is the policy rate. Tether earned roughly $13 billion in 2024 on $100 billion of T-bill reserves at a 5 percent policy rate. The same balance sheet at a 3 percent policy rate earns $6 billion. The captive holder base shrinks with every cut.

The five components do not appear connected in any individual policy debate. The ESLR reform is described as Treasury market resilience. The T-bill shift is described as cost management. The GENIUS Act is described as stablecoin regulation. The CPI methodology is described as measurement modernisation. The Warsh doctrine is described as regime change. Each description is true. Together, they are the architecture for absorbing federal debt at suppressed real yields.

The five components share one property the 1966-1980 architecture did not have. They are all priced, directly or indirectly, off the policy rate. T-bills price off the rate by construction. Stablecoin reserves earn the T-bill yield by statute. Money market funds hold T-bills and repo. Bank deposit rates lag the policy rate down on every cut. Long bonds carry a term premium over the policy rate that fluctuates but does not detach. The captive savings base of 2026 sits on instruments that the Federal Reserve controls through one variable. Regulation Q was a static ceiling that inflation rose above. The Warsh rate is a dynamic ceiling being pushed down before inflation falls. The mechanism produces the same outcome. The conduit is faster.

The result, and the precedent

The output of the architecture is nominal yields anchored below true inflation. Real rates structurally negative. Federal debt devalued in real terms without explicit default and without explicit hyperinflation. The phenomenon has a technical name. Carmen Reinhart and Belen Sbrancia called it financial repression in 2011 because that is what it is.

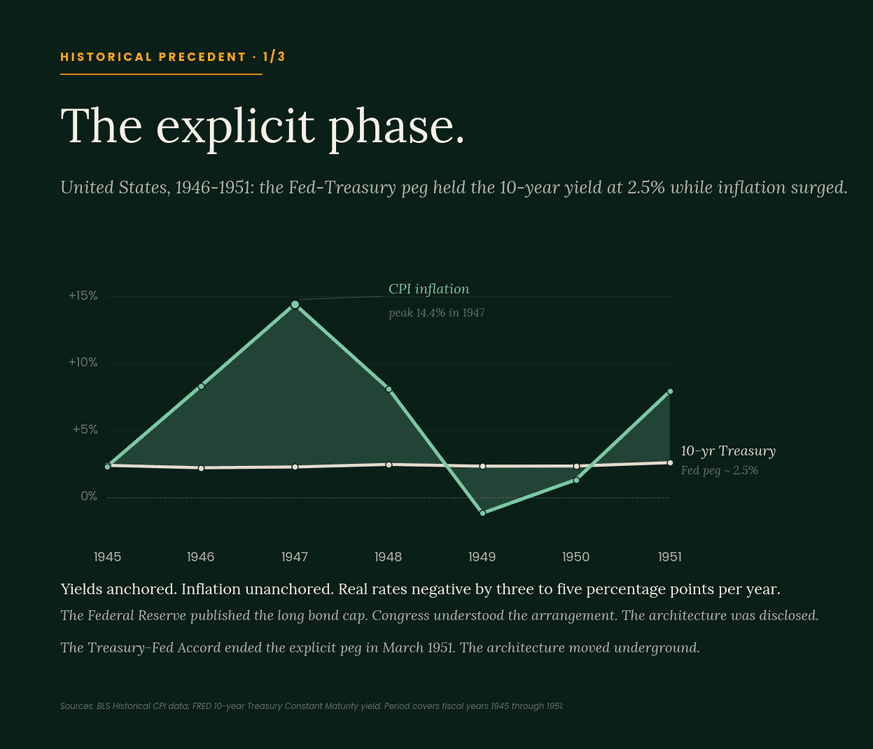

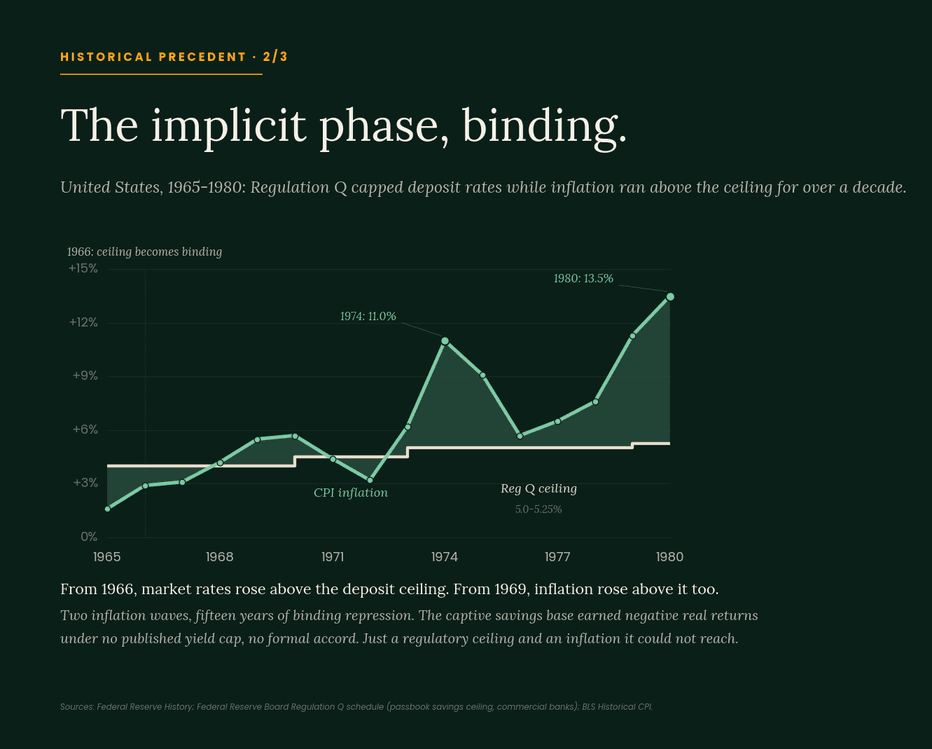

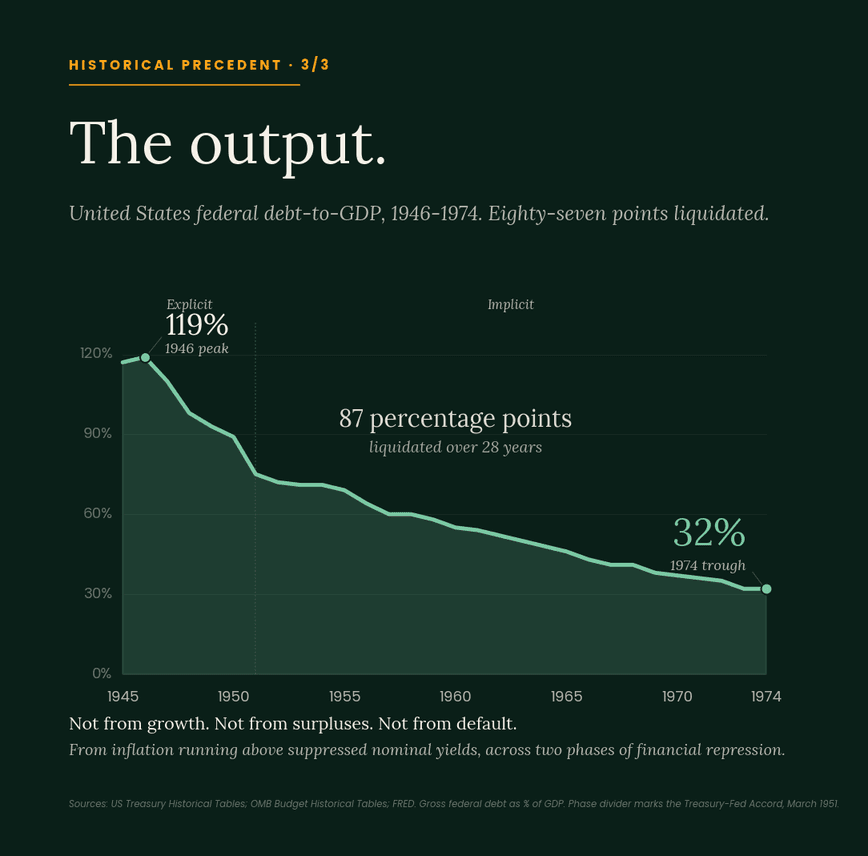

The most relevant historical precedent is the one Americans tend to remember least. Between 1946 and 1974, US federal debt fell from 119 percent of GDP to roughly 32 percent. Eighty-seven percentage points liquidated over twenty-eight years. The mechanism worked in two phases. The first, from 1942 through 1951, was the explicit phase: the Federal Reserve held the long bond yield at 2.5 percent under formal accord with the Treasury, while CPI inflation averaged 6.5 percent and peaked above 14 percent in 1947. Real rates were negative by three to five percentage points per year for most of the period. The second phase, from 1952 through 1980, was the implicit phase. No explicit yield peg, but Regulation Q deposit caps, capital controls, selective tax exemptions for government debt, and institutional channels that routed savings into government debt at suppressed rates. The implicit architecture had two sub-periods. From 1952 through 1965 the architecture was in place but not binding: market rates and deposit rates both sat below the Regulation Q ceiling, so the cap did not bite. From 1966 onward, market rates rose above the ceiling and the architecture became operational. Bank depositors and savings institution holders began earning negative real returns. The 1973-74 and 1979-80 inflation waves, which pushed CPI to 11 percent and then 13.5 percent while the deposit ceiling sat at 5 to 5.25 percent, were the moments the implicit repression became visible in households' purchasing power. The architecture was implicit. The cost was real, and it ran for fifteen years.

Japan has run a version of the same architecture for thirty-five years. Debt-to-GDP rose from roughly 70 percent in 1990 to over 263 percent today, with the Bank of Japan absorbing the marginal issuance and real rates structurally negative throughout. The European Central Bank ran a similar architecture from 2010 onward through sovereign bond purchases that anchored yields below underlying inflation. Each was obscured at the time as crisis management. Each was visible in retrospect as a coordinated debt management strategy.

The American architecture being assembled in 2026 is not the 1945 model. It is the 1952 model entering the 1966 phase. The explicit Fed-Treasury peg of 1942-1951 was openly disclosed: the Fed published the long bond yield cap, and Congress understood the arrangement. The implicit architecture that ran from 1952 through 1974 was not openly disclosed. It operated through Regulation Q, capital controls, tax preferences, and bank regulation. Savers absorbed the cost without being told that an architecture was extracting it. The 2026 architecture replicates the implicit version, in updated institutional vocabulary. ESLR reform replaces Regulation Q. Stablecoin requirements replace capital controls. T-bill shortening replaces the tax-preference channel. The CPI methodology replaces the simple absence of measurement. The architecture sits where the implicit precedent sat in 1965: in place but not yet binding. Warsh's stated plan to cut rates aggressively, justified by AI productivity, is the lever that would make it binding. The 1966 transition took two years of market rates rising into the cap. The 2026 transition could take one Federal Open Market Committee meeting.

Warsh's personal portfolio

Warsh's pre-nomination financial disclosure documents over $100 million in digital asset investments across twenty named entities, including stablecoin infrastructure (Basis), Bitcoin payments (Flashnet), prediction markets (Polymarket), digital asset managers (Bitwise, Polychain, Electric Capital), and various DeFi and Layer 1 holdings. He has signed an ethics agreement requiring divestment of most private holdings. The portfolio is therefore not a forward signal of his policy direction. It is a backward signal of his pre-confirmation understanding. He has personal equity in many of the people building the stablecoin infrastructure that the GENIUS Act has converted into a structural Treasury bid. He is not being briefed on the architecture. He has been reading the same map the architecture is being built on.

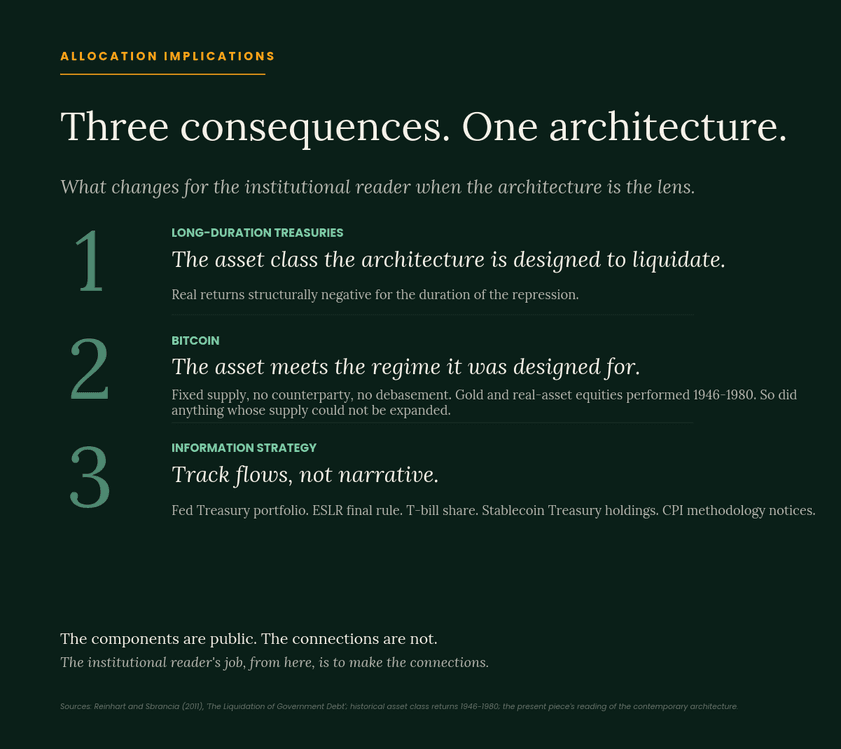

Three structural consequences

The first consequence is that real returns on long-duration Treasuries are likely to be structurally negative for the duration of the repression. This is not a forecast. It is the operating principle of the architecture. Allocators who hold long-duration Treasury exposure as a portfolio anchor are holding the asset class the architecture is designed to liquidate in real terms.

The second consequence is that Bitcoin's monetary case gets the macro regime it was designed for. Fixed supply, no counterparty, no debasement mechanism, no political override. The asset's monetary thesis has been theoretical for fifteen years because the regime had not yet required it. The regime now requires it. The 1946-1974 precedent is the most useful institutional reference.

The architecture worked. Eighty-seven percentage points of debt-to-GDP were liquidated. The assets that performed in real terms during the period were the ones whose supply could not be expanded to absorb the absorption. Gold performed, particularly in the 1970s wave when the implicit repression intensified. Real-asset equities performed when held through multiple cycles. Long Treasuries did not perform in real terms across the whole period. The institutional reader who held the 10-year Treasury through 1946-1974 lost a substantial portion of real purchasing power, even with coupon income reinvested.

The third consequence is that the institutional reader's information strategy has to change. The architecture is visible in the data even when the policy debate obscures it. Track the Fed balance sheet trajectory. Track the ESLR final rule. Track the T-bill share of issuance. Track stablecoin Treasury holdings. Track the CPI methodology notices. Each individual data series is dry. Together, they are the most consequential financial market story of the coming decade.

What to watch

The Fed Treasury portfolio trajectory under Warsh. If it shrinks slowly through declining reinvestment of maturing Treasuries, the runoff is being passed back to the private market on schedule.

The Fed MBS portfolio trajectory. Maturing MBS proceeds are currently being reinvested into T-bills. Whether that continues, accelerates, or shifts to coupons will signal how the mortgage market is being managed alongside the Treasury repression.

The ESLR final rule. The proposal is in public comment. Whether the final rule includes the Treasury exemption for GSIB broker-dealer subsidiaries will signal how aggressively banks are being converted into Treasury absorbers.

The T-bill share of issuance at the next Treasury quarterly refunding. A move above 22 or 23 percent confirms the maturity shortening is operational.

Stablecoin Treasury holdings. Tether already holds roughly $100 billion. Circle holds tens of billions. The aggregate is climbing. Watch the rate of climb.

The June FOMC meeting under Warsh's chairmanship. Whether the Summary of Economic Projections includes the dot plot, and whether the inflation framing is described in numerical terms or in Warsh's qualitative formulation.

The conclusion that is being obscured

The components of the architecture are public. The ESLR proposal is public. The Treasury issuance plans are public. The GENIUS Act is law. The CPI methodology notices are published. Warsh's doctrine is on the Senate transcript. None of this is hidden.

What has not been done, in any analysis I have seen, is to place the five components on a single page and observe that they describe a single mechanism. The mechanism is financial repression. The precedent is 1946-1974, both the explicit and implicit phase. The output is a debt that gets liquidated in real terms while the headline numbers tell a different story.

The institutional reader who has held long-duration sovereign exposure as a portfolio anchor is holding the asset class the architecture is designed to liquidate. The institutional reader who has held Bitcoin as a theoretical hedge against monetary regime change now holds the asset to hedge against the regime change itself.

Shrink the Fed. Grow the system. The numbers tell one story. The architecture tell another.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

CLARITY Act floor vote pending.

The Senate Banking Committee passed the Digital Asset Market Clarity Act 15-9 on 14 May, with Senators Gallego and Alsobrooks crossing party lines. The bill now needs 60 floor votes to overcome a filibuster. The White House is targeting a 4 July signing. Even in the best case, enforceable rules will not exist until 2027.

Executive order on 22 May.

The administration issued a new EO directing federal agencies to reassess outdated digital asset rules. The regulatory normalisation tempo continues. The next signal worth watching is the final ESLR rule from the Fed, OCC and FDIC, which determines how much Treasury inventory the commercial banking system can absorb without it counting against capital.

Stablecoin yield compromise still contested.

The CLARITY Act's stablecoin yield language is the bill's most contested clause. Yield-bearing variants such as USDY and sUSDS continue to route Treasury yield through sister-token wrappers and drove more than half of stablecoin market growth in Q1. The bill tightens the loophole. The banking lobby would prefer it did not exist at all.

AI & Financial Infrastructure

Power is the binding constraint.

Morgan Stanley projects US data centre demand at 74 GW by 2028 against a 49 GW shortfall in available power access. Polymarket prices the probability of at least one US AI data centre moratorium passing into law by year-end at 93.5%. Constellation Energy fell 6% on Monday. The grid build-out is no longer keeping pace with the load growth.

The AI capex curve has not bent.

Amazon, Google, Meta and Microsoft are now committing roughly $400 billion per year to AI data centre infrastructure. Combined industry spending across 2025-2026 is projected above $1 trillion. The buildout continues at the pace of capital, not at the pace of available power, which is the structural mismatch that has not yet been priced through.

The onchain financial layer keeps building.

Babylon Labs this week proposed native Bitcoin collateral on Aave V4 via Trustless Bitcoin Vaults, with no bridge, wrapper, or custodian. Hyperliquid is expanding beyond perpetual derivatives into pre-IPO markets, prediction contracts, and 24/7 asset trading. The composability story keeps moving on rails the legacy infrastructure cannot easily replicate.

Geopolitics & Markets

Bond market rejects the easing thesis.

The 30-year Treasury yield touched 5.06% on Friday, the highest level since 2007. The 10-year closed at 4.56%, the highest in over a year. Fed funds futures now price a 2026 rate hike as more likely than a cut. The bond market is pricing inflation persistence, not the AI-driven disinflation that Warsh's framework requires.

Equity records decouple from bond stress.

The Dow closed at 50,579, the S&P 500 at 7,473, the Nasdaq at 26,344, all fresh highs on Friday. Equity is pricing for an Iran resolution that has not materialised and a Fed pivot the bond market does not expect. Two of those positions cannot both be right.

Risk allocation reset into the tail.

New US strikes on Iran triggered roughly $300 million in digital asset liquidations on Monday. Bitcoin spot ETFs shed $1.25 billion across a six-day outflow streak. Jane Street cut Bitcoin ETF holdings by 70% in Q1; Goldman reduced by 10%. The market-making complex has stepped back. Allocators looking to add into stress prints will find thinner cover than they had a quarter ago.

The Week in Numbers

| Indicator | Reading |

|---|---|

| 30-yr Treasury (Fri close) | 5.06% |

| 10-yr Treasury (Fri close) | 4.56% |

| S&P 500 (Fri record) | 7,473 |

| Fed funds target | 3.50-3.75% |

| Bitcoin (Tue open) | $77,352 |

| 6-day BTC ETF outflows | -$1.25B |

| Polymarket AI moratorium | 93.5% |

| CLARITY Banking Committee vote | 15-9 |

What to Watch This Week

| Date | Event | Why it matters |

|---|---|---|

| May 27 (Wed) | Conference Board Consumer Confidence; Durable Goods | First reads on consumer state and capex appetite after a week of bond-yield stress. |

| May 28 (Thu) | Q1 GDP second estimate; Initial Jobless Claims | Growth picture going into the data corridor before Warsh's first FOMC. |

| May 29 (Fri) | April PCE inflation; Personal Income & Spending | The Fed's preferred inflation measure. First major print Warsh inherits. |

| Rolling | ESLR final rule (Fed, OCC, FDIC) | Determines how much Treasury inventory the commercial banking system can absorb. |

| Rolling | CLARITY Act floor vote | Senate timing fluid. 60 votes needed. White House targets 4 July signing. |

| June 5 | May Nonfarm Payrolls | Last labor print before Warsh's first FOMC on 16-17 June. |