June 2, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

A thought experiment followed by an evidence review: history has handed anyone who wants to manage the price of a hard, fixed-supply asset the same three-part toolkit. Every component now exists around bitcoin at a scale it never has. The toolkit operates on claims; it has no grip on a coin held directly.

If you wanted to suppress the price of a fixed-supply asset, here is the toolkit. The open question is how much of it is being used.

In late seventeenth-century London, goldsmiths stored gold in iron vaults and issued paper receipts redeemable on demand. The receipts were lighter than coin and easier to carry, so they began to circulate between merchants as money in their own right. The metal stayed in the vault.

The goldsmiths noticed that almost no one redeemed at once, and drew the conclusion that built modern banking: they issued more receipts than they held in gold and lent the surplus at interest. The paper claim circulated as money while the metal it referenced stayed singular. Every holder could be paid, but only because they did not all present at the same time.

For a while this was a quiet fraud; through scale and respectability it became the operating system, and then it went further than the goldsmiths ever did. The goldsmith at least held gold. Modern banking removed the asset: the dollar's last formal link to gold was cut in 1971, leaving deposits as claims on fiat, which is a claim on nothing in particular. The reserve requirement that once forced a bank to hold a fraction of base money against deposits, itself fiat against fiat rather than anything real, was then abolished outright, in the United Kingdom in 1981 and the United States in 2020. What runs today is not a fractional reserve system but a no-reserve one, issuing claims on nothing and holding nothing against them.

Bitcoin is the first hard, fixed-supply, verifiable bearer asset to circulate at scale since gold, the first claim in fifty years that redeems into something singular and scarce. This piece is not an accusation but a thought experiment followed by an evidence review. Suppose you wanted to manage the price of such an asset, to hold it in a band and keep its monetary signal quiet. History has handed those who wish to do so the toolkit. The question, asked calmly and with the data in front of us, is how much of that toolkit now exists around Bitcoin, and how much of it is being used. The whitepaper, in its first sentence, was written to make the toolkit irrelevant.

The pattern through history

The pattern has run twice through the gold market in living memory. The London Gold Pool of 1961 to 1968 was the first openly admitted version: eight central banks (the US Federal Reserve, the Bank of England, the Bundesbank, the Banca d'Italia, the Banque de France, the Swiss National Bank, the Netherlands Bank, and the National Bank of Belgium) pooled reserves and sold into the London market whenever gold rose above $35 an ounce, defending the price to stop it revealing the dollar's true standing under Bretton Woods. It collapsed in 1968 when France withdrew and demand outran the metal the participants could supply. It failed for the reason these schemes always fail. The physical ran out.

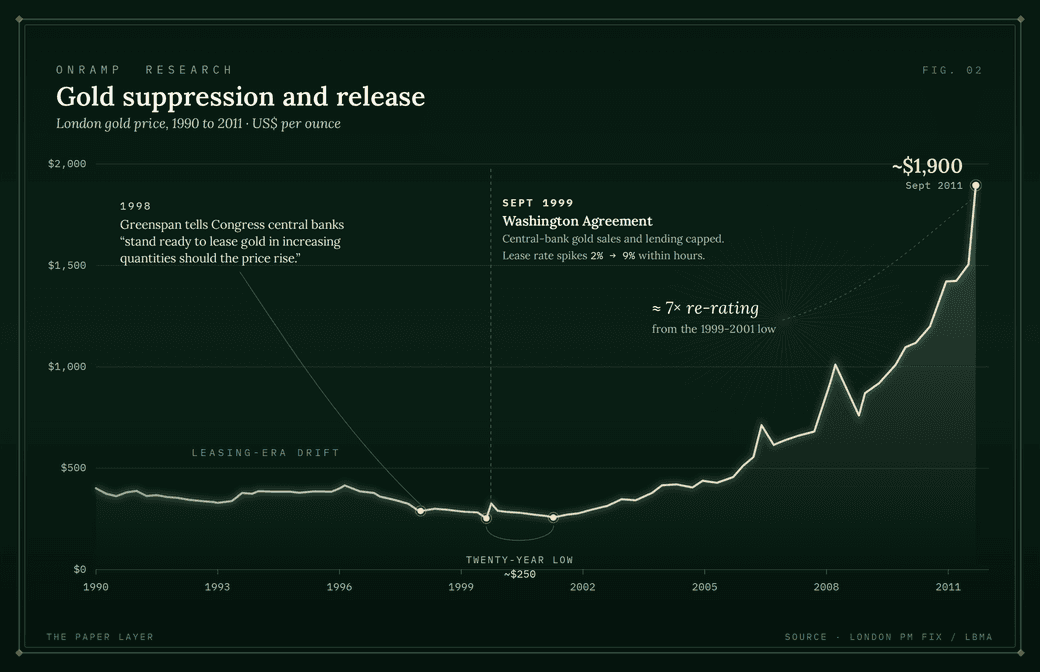

The 1990s version was subtler. As Ferdinand Lips documents in Gold Wars, central banks leased physical gold to bullion banks at one to two percent a year; the bullion banks sold it at the spot price immediately, bought Treasuries yielding five percent, and pocketed the spread. The metal flowed into Asian jewellery and did not come back. Lips estimates five to six thousand tonnes were leased this way, three to five years of world mine production. The same banks advising the central banks were the ones capturing the carry.

The mechanism was stated openly. In 1998 Federal Reserve chairman Alan Greenspan told Congress that central banks stand ready to lease gold in increasing quantities should the price rise, a sitting central banker describing a method for capping a price by issuing supply against demand. It broke in September 1999, when fifteen European central banks signed the Washington Agreement capping their gold sales and lending. The lease rate spiked from roughly two percent to nine within hours as bullion banks realised they might have to return metal they could not source. Gold ran from $257 to over $330 in days, and from a 2001 base of $250 to $1,900 by 2011, a sevenfold re-rating once the paper could no longer absorb the buying.

Why it lasted, and why it could last again if employed

The gold suppression ran for the better part of three decades, and the reasons it lasted are visible again now. It lasted because every participant was paid to let it continue: central banks earned a lease income and a flattering low price for the currencies they issued, the bullion banks earned the carry, and no single party had reason to call it. It lasted because the cost fell on a diffuse, uncoordinated group, the holders of paper gold, who could each always redeem and so never collectively tested the system.

And it lasted because the macro backdrop required it. A monetary system built on suppressed real yields cannot tolerate a freely rising hard-money signal, because the hard-money price rising is precisely the market pricing the real yield the system is holding down. The two are the same fact from opposite sides. That is the incentive that many overlook. The mid-2020s, fiscal dominance, a long sovereign-debt overhang, and real yields held below where a free market would set them, is structurally the same environment that made gold suppression useful after the war and Vietnam. The lesson is not that suppression is permanent. It is that it ends on a timeline determined by holders enforcing the underlying scarcity, not a timeline determined by how widespread the complaints are.

The toolkit, abstracted

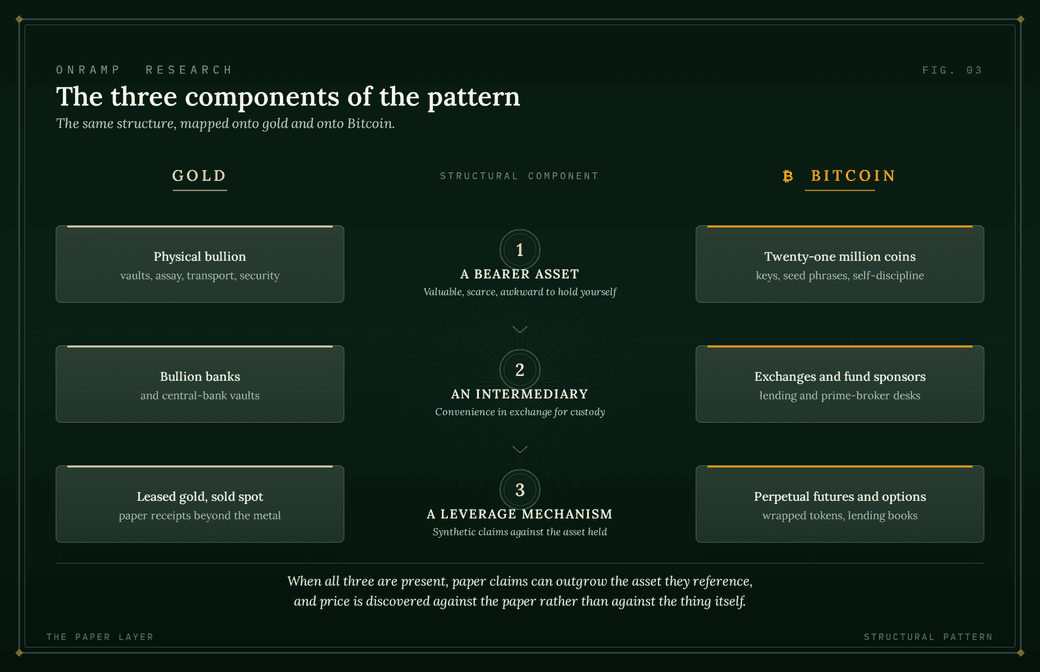

Strip the two gold episodes to their structure and the same three components appear every time.

First, a bearer asset that is expensive, complex, risky or inconvenient to custody directly, which makes intermediation attractive: gold needed vaults and assay, Bitcoin needs keys and operational discipline. Second, an intermediary that offers convenience in exchange for custody: goldsmiths and bullion banks then, exchanges, fund sponsors and lending desks now. Third, a leverage mechanism that issues synthetic claims against the held asset: paper receipts and leased gold then, derivatives, wrapped tokens and rehypothecated books now. When all three are present, paper claims can outgrow the asset and price can be set against the paper rather than the thing. None of it requires intent. It requires only that each participant's incentives point the same way.

What the toolkit looks like around Bitcoin today

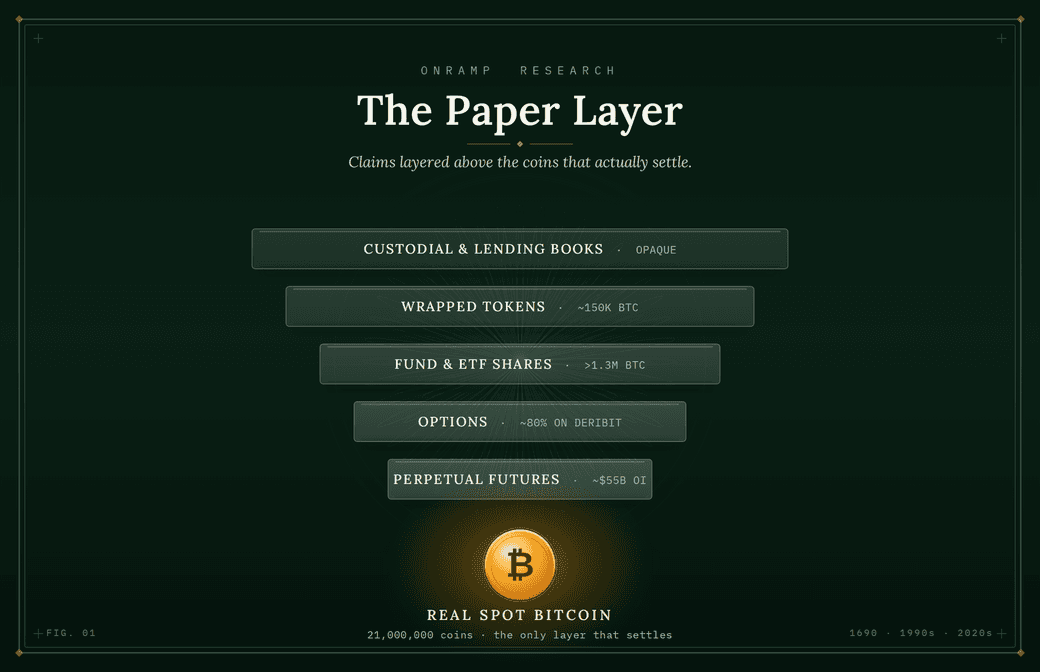

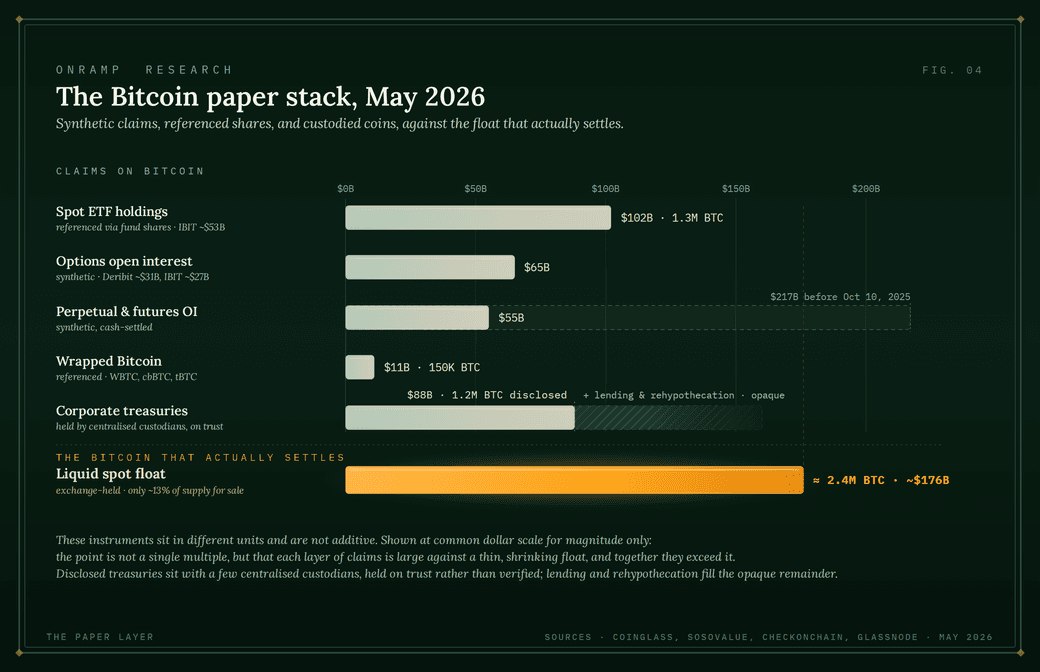

Every component is now present around Bitcoin, and every layer is measurable from public data. Each is unremarkable on its own. The question is what they total.

The purest synthetic layer is offshore perpetual futures, where open interest sits near $55 billion today and reached $217 billion the night before the October 2025 cascade; most contracts are cash-settled, so a short need never source a real coin. The eleven US spot ETFs together hold over 1.3 million BTC, with BlackRock's IBIT near 785,000 at its peak. Global options open interest, once concentrated on Deribit, is now split roughly evenly between Deribit and BlackRock's listed IBIT options, where dealer hedging on the regulated side feeds back into the spot tape. Around $11 billion of Bitcoin has been wrapped into token form. And the collateral beneath much of this is itself paper: Tether's roughly $190 billion of USDT, most of it held in Treasuries, is the pool the perpetual market is largely margined against, so a perpetual short is a synthetic Bitcoin position backed by a paper dollar backed by paper Treasuries. Beneath all of it sits the custodial layer, whose floor is at least disclosed: public companies report holding over 1.2 million BTC, almost all of it with a handful of centralised custodians, on the custodian's word rather than the holder's keys. The lending and rehypothecation below that floor stay opaque, reconstructable only in fragments from quarterly filings.

These do not sum to an honest single multiple against 21 million coins; derivatives net, and some custody is properly backed and attested. The answerable question is narrower and more useful: how much of the buying that appears to clear against spot is in fact clearing against synthetic supply that did not exist when the order was placed? That number is not 21 million, but it is not zero, and it is larger than it has ever been.

The natural experiment

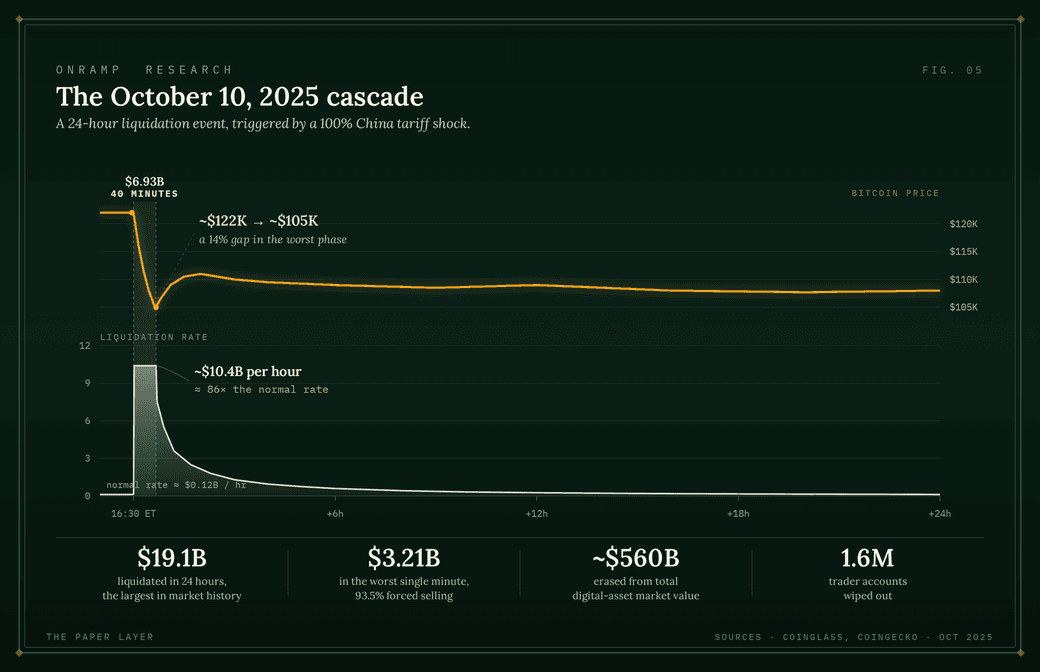

On October 10, 2025, the paper layer was briefly forced to meet spot, and the result is instructive whatever one concludes about intent.

A 100 percent China tariff announced on Truth Social triggered $19.1 billion of forced liquidations in twenty-four hours, the largest in digital-asset history; inside it, a forty-minute window cleared $6.93 billion at roughly $10.4 billion an hour against a baseline near $0.12 billion. About $560 billion came off total market value, and a single trader who shorted minutes before the post made roughly $200 million. Whether that was foresight or something else is unresolved, and the structural lesson does not depend on resolving it. When the leverage stack was forced to clear, spot could not absorb it at the prevailing paper price, and the price gapped to where it could. The loss fell on holders of paper, not holders of the asset. Bitcoin reached about $124,000 in October 2025 and trades near $73,600 today, a forty-one percent drawdown that needs no conspiracy to explain, only the observation that the paper layer absorbed the marginal monetary-premium bid and then broke. Howver 1 bitcoin still equals 1 bitcoin.

Two sides of the same evidence

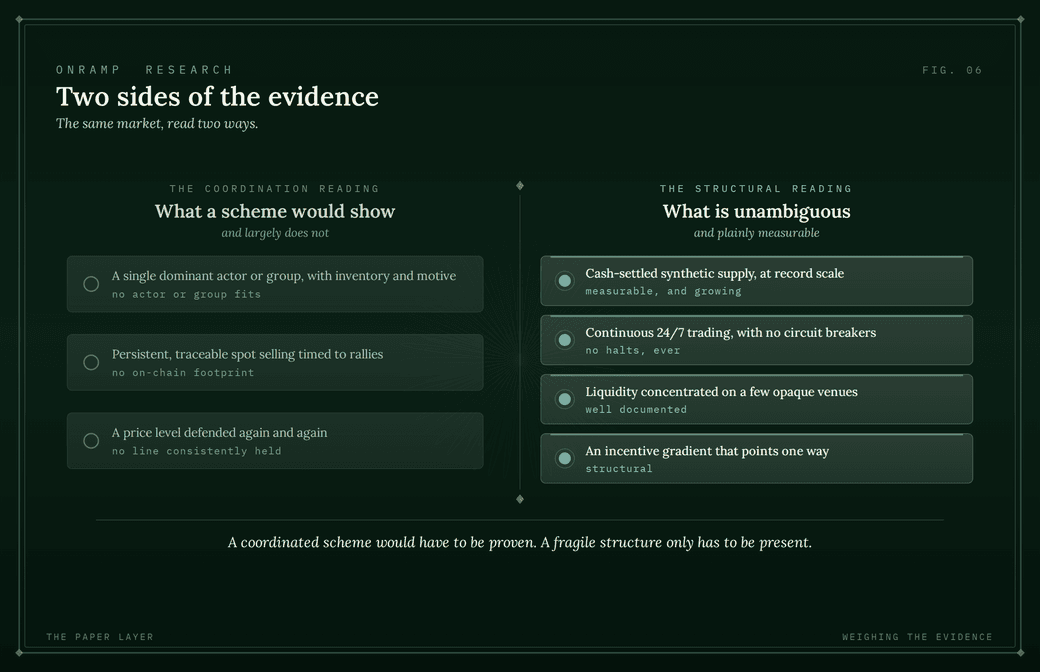

The question of whether Bitcoin's price is being deliberately suppressed deserves both sides of an honest answer, and the split is cleaner shown than argued.

If a coordinated scheme were running, you would expect a single dominant actor or group with both inventory and motive, persistent and traceable spot selling timed against rallies, and a clearing mechanism defending a specific level. The honest reading is that those fingerprints are not clearly present; much of the price action can be explained by ordinary positioning, deleveraging, and a genuine rotation of the debasement bid into gold, which has outperformed Bitcoin since the high.

What is unambiguous is the other half. The structural capacity for price to be set by paper rather than spot now exists at a scale it never has, and in a market that trades around the clock with no circuit breakers, with synthetic volume many multiples of genuine liquid spot supply and liquidity concentrated on a few opaque venues, a handful of large actors each optimising against the same weaknesses can produce the effects of suppression with no coordination at all. You do not need a conspiracy. You need an incentive gradient, and it points one way. Where each reader places today's price on that line is a fair matter for disagreement. That the capacity exists, and is growing, is not.

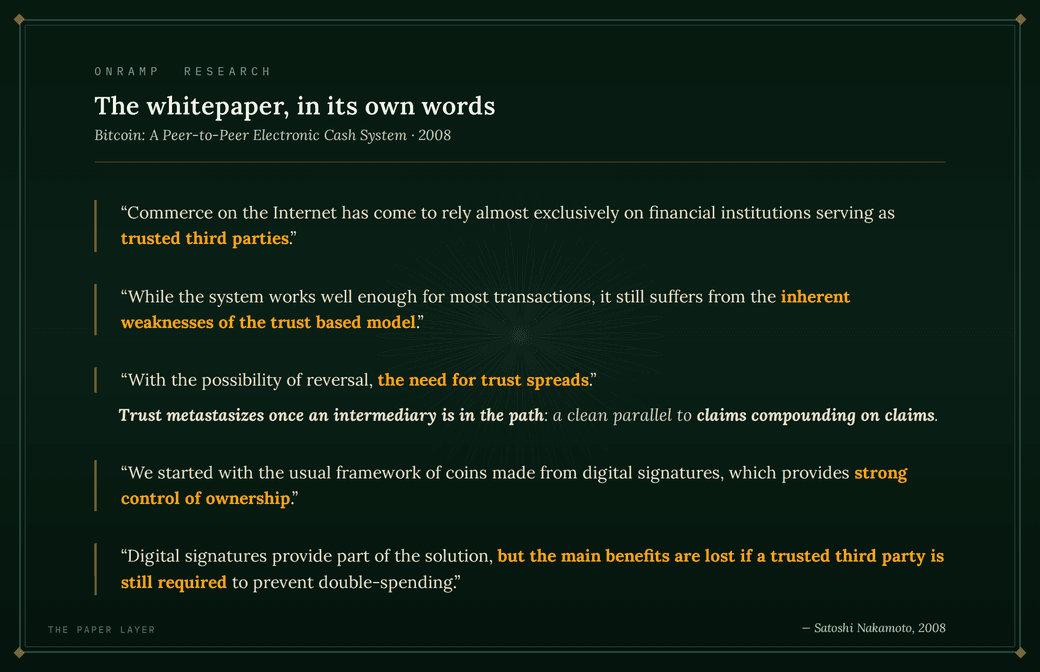

The whitepaper already addressed this

Read with the goldsmith pattern in mind, the whitepaper is not only a payment-network design but a structural critique of intermediated money: its opening words name the trusted third party that produced fractional reserves in seventeenth-century London and gold leasing in the 1990s. Every intermediary between the holder and the coin reintroduces, in part, the thing Bitcoin was built to remove. The bearer property is preserved only when the holder controls or distributes the control to the keys to independent holders who can only act under the authority of the holder, and where the coins can be independently verified 24/7/365 by direct reference to the Bitcoin blockchain; every other arrangement is a referenced claim on someone's promise. This is not a moral failing of any institution (although it could be) but a structural fact about what a claim is versus what a coin is. The toolkit works on claims. It has no purchase on a coin held directly.

What this means for the holder

The implications follow from the structure, not from any view about intent, and they hold whether or not the toolkit is being used deliberately.

Hold Bitcoin in a form that cannot be rehypothecated. Only two structures qualify, and both are below.

Understand what each wrapper is. A spot-fund share is a regulated claim on a custodied pool, not a coin; a Digital Asset Treasury common share is a residual equity claim sitting behind the company's preferred and convertible holders, referencing Bitcoin typically held with a single custodian that can, under some structures, be a contemplated source of funds. The collateral for a credit or hybrid credit instrument references a single custodian not chosen by the holder which cannot be independently verified. None of this is hidden, it is in ordinary filings, and for many holders the leverage is the point. The distinction is simply that these are referenced Bitcoin, not bearer assets.

Do not out-leverage the system. The holder's one structural edge is time horizon, and leverage surrenders it, as October 10 showed for everyone who was long a contract rather than a coin.

Demand proof of ownership, not just proof of reserves. Proof of reserves was a real step after FTX, and the credible programs deserve recognition, but it certifies what an entity held on a given day, not that the holdings are safe. Nor does it measure the other side of a counterparties balance sheet, its liabilities. Audited financial statements are a red herring in this respect, just look up any of the names of the big 4 auditors and one of these words "scandal", "fine", "negligence", "cheating", "misconduct", "malpractice", fraud" or "conflict of interest". Even a liability-inclusive Merkle-tree attestation (assuming the entities only liabilities are bitcoin owed to its clients) is silent on whether your coins are segregated, titled to you, and beyond unilateral control; Bybit published a clean audited attestation above one hundred percent the day before losing roughly $1.5 billion in the largest exchange theft on record. The binding test is ownership: a segregated on-chain address, legal title, and control split across independent institutions so no single party can move or lend the coins. A coin that passes that test is also a coin the paper layer cannot rehypothecate

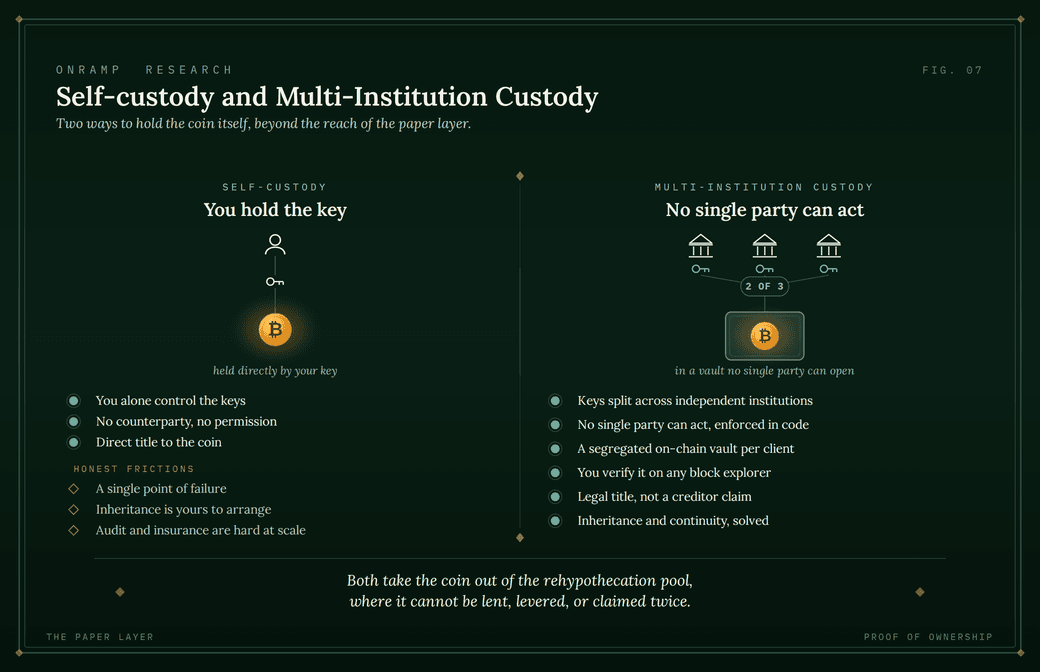

The two solutions that make the toolkit irrelevant

Two custody structures, and only two, preserve the bearer property the whitepaper was built to protect. Both make the holder invisible to the paper layer. The choice between them is not which is better Bitcoin but which operational profile fits the holder.

Self-custody is the original design: the holder controls the keys and the coin sits in an output only they can spend, with no intermediary and no counterparty. Its frictions, single point of failure, inheritance, and the audit and insurance requirements institutions cannot ignore, are honest, and they are why it does not fit everyone.

Multi-Institution Custody: distributes the keys to move Bitcoin across several independent institutions, none able to act alone because the multi-key requirement is enforced cryptographically rather than by policy. The holder keeps legal title to a segregated on-chain vault, can download the descriptors and verify the balance on any block explorer at any time 24/7365, and in a custodian failure owns the coin rather than a creditor claim. The same distributed-key model that removes rehypothecation also solves the single-point-of-failure and inheritance problems that make self-custody hard. Segregation, legal title, distributed control, and permissionless on-chain verification are what proof of ownership means in practice: not a snapshot that an entity held reserves on some past date, but standing evidence that the coins are yours and beyond any single party's reach.

A self-custodied coin and an MIC-custodied coin are identical in the property that matters: neither is available to the paper layer. Every other arrangement leaves the coin under an intermediary that can lend or reference it. Each coin that moves into either structure shrinks the toolkit's addressable supply at the margin, the same way the gold scheme ended in 1999 when the lendable inventory ran out. On a long enough timeline that point is arithmetic, because Bitcoin's supply is fixed and the paper layer is not.

Conclusion

The whole question of whether the price is being managed, by whom, and how much, is one the holder of spot in self-custody or Multi-Institution Custody does not have to answer over a long term investment horizon. The toolkit operates on claims. It has no grip on a coin held directly. The goldsmiths spent two centuries pretending the receipts and the gold were the same thing, and the gold holders of the last century waited decades for a suppression that broke only when the vaults ran dry. The reader does not have to wait, and does not have to be right about intent. They only have to hold the coin rather than the claim. The whitepaper said so in 2008. The data lets us see it now.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

A sovereign bitcoin reserve is taking shape.

At the federal level it is still an executive action, not a statute: the Treasury holds about 328,000 BTC seized in enforcement cases, the largest known sovereign pile, under a March 2025 order that bars selling it. A bipartisan bill filed May 21 would write the reserve into law and authorize buying up to a million BTC over five years. The states moved faster. New Hampshire and Arizona passed the first reserve laws last year, and Texas went furthest, funding a standalone reserve outside its treasury that now holds about $10 million in bitcoin; this week it named an advisory committee and began seeking a custodian to hold the coins directly and buy more.

The $10 trillion retirement market is opening.

For a decade the roughly $12 trillion in 401(k) plans stayed walled off from bitcoin, less by rule than by liability, after a 2022 Labor Department warning froze plan sponsors. That reversed last year, and on March 30 the department proposed a safe-harbor rule protecting any fiduciary who follows a documented, six-factor process when adding alternatives, bitcoin among them. It is not yet final, and even supporters expect a crawl: benefits lawyers say sponsors will wait until courts confirm the safe harbor actually shields them, which could take years. The door is open, but the money arrives as a slow tide, not the wave that met the ETFs.

Bitcoin is becoming mortgage collateral.

In March, Fannie Mae, with the lender Better and Coinbase, unveiled the first program that lets a borrower pledge bitcoin toward a home instead of selling it, following a 2025 directive to count digital assets in mortgage underwriting. Because Fannie sets the rules for much of the US conforming-loan market, its acceptance pulls an asset class toward the mainstream. The guardrails are heavy: holdings are discounted, capped as a share of reserves, and must sit with a regulated custodian. It is cautious and small for now, but bitcoin is being wired into the plumbing of American housing finance.

The quantum clock moved, the threat did not.

On March 30, researchers from Google's quantum group and academic partners published a tighter estimate of what it would take to break the elliptic-curve signatures bitcoin relies on: under 500,000 physical qubits, down nearly an order of magnitude in a year. No machine is close to that today, and the paper is a resource estimate, not a break. The harder task is engineering a migration, where bitcoin carries less risk than most chains; the real exposure is old or reused addresses with visible public keys, including 2 to 3 million coins whose owners are gone. The industry targets readiness around 2029. The math got closer; the homework now has a deadline.

AI & Financial Infrastructure

Tech turned capital-intensive on a historic scale.

After first-quarter results in late April, the four biggest hyperscalers, Microsoft, Alphabet, Amazon, and Meta, are now guiding to roughly $700 billion of capital spending in 2026, up about 77% from last year's record and triple the level of two years ago. Three of the four raised their numbers in the same week, with Microsoft alone near $190 billion and attributing about $25 billion of it to rising memory and component prices. Two-thirds of Microsoft's quarterly capex went to short-lived assets, mostly chips. At 45% to 57% of revenue, this is the spending profile of a utility, not the asset-light software business investors once owned.

A $176 billion question sits in the footnotes.

Nvidia ships a faster architecture every 12 to 18 months, yet hyperscalers depreciate the chips over five or six years, which flatters earnings. Michael Burry, who closed his fund in November after betting against Nvidia, estimates the gap understates depreciation by about $176 billion across 2026 to 2028, enough to overstate sector profits by roughly a fifth. The rebuttal is that a chip retired from frontier training still earns for years on lighter work, so a longer life can be honest, and the change is a permitted estimate, not fraud. Tellingly, under the same facts Amazon shortened some server lives from six years to five, taking a $700 million hit, while Meta extended its own.

The money has begun to move in a circle.

Roughly $1 trillion of overlapping commitments now bind the same handful of companies: Nvidia is investing in OpenAI, which has committed to buy Nvidia chips and to rent some $300 billion of Oracle cloud, while Oracle and CoreWeave buy yet more Nvidia chips. Supporters, including Janus Henderson, call it a rational way to lock in scarce supply, a virtuous circle of vendor financing. Skeptics hear an echo of the dot-com telecom vendors who lent customers the money to buy their gear, and warn that when everyone is both buyer and seller the correlation risk is enormous. In February a report that the Nvidia-OpenAI deal had stalled briefly rattled the whole chain before both sides pushed back.

Spending keeps running ahead of revenue.

The gap between what is invested in AI and what it earns has widened from about $125 billion in 2024 to an estimated $500 to $600 billion on one running tally, while an MIT study found 95% of corporate AI pilots never reached production and only a small share of consumers pay for the tools. The bullish reading is that demand is real and early: cloud backlogs are enormous, with Google's alone above $460 billion and roughly doubling in a quarter, and AI revenue at the leaders is growing fast off a small base. The question is not whether the revenue is coming, but whether it arrives before the depreciation and the interest do.

Geopolitics & Markets

China is rationing the world's rare earths.

Beijing's hold on rare earths is an active lever now, not a latent one. Its April 2025 licensing regime over seven heavy and medium elements, the ones inside the magnets in jets, vehicles, and robots, remains fully in force; a broader second wave from October, reaching any product made with Chinese-origin material, was suspended only until November 10 under the current truce. China processes more than 90% of global supply and dominates the heavy elements outright, and roughly 70% of US imports trace back to it. The IEA estimates a full reimposition could put $6.5 trillion of annual activity outside China at risk, and analysts put a truly independent chain 10 to 20 years away.

Reshoring has not moved the chip chokepoint.

Despite tens of billions committed to new fabs in the US, Japan, and Germany, more than 90% of the world's leading-edge chips still come from Taiwan, the overwhelming majority from a single company, and the lithography machines that print them come solely from ASML in the Netherlands. That leaves two stacked monopolies beneath the entire computing stack, the same stack now absorbing some $700 billion of AI capex a year. The concentration is both Taiwan's shield and its risk: semiconductors are around a fifth of the island's GDP, which makes the chokepoint strategically vital and dangerously singular at once.

The dollar's reserve share keeps slipping.

Fresh IMF figures put the dollar near 56.9% of allocated currency reserves in 2025, its lowest since 1995 and down from more than 70% at the turn of the century. The decline is real but orderly, and the detail matters: by the IMF's own decomposition, roughly 92% of the recent fall reflects exchange-rate moves rather than central banks actively selling dollars. This is gradual diversification, not flight, and the dollar remains the world's reserve currency by a wide margin. What has changed is the direction of travel, and where the marginal reserve dollar now goes.

Central banks now hold more gold than Treasuries.

Official gold buying topped 1,000 tonnes for a fourth straight year in 2025, a pace that has lifted gold to about 30% of global reserves, up from roughly 13% in 2017. The cumulative effect crossed a symbolic line: central banks' gold, worth around $5.2 trillion, now exceeds their holdings of foreign US Treasuries, and once gold is counted the dollar's share of total reserves slips below half. None of this unseats the dollar, but it tells you what reserve managers reach for when they want an asset that is no one else's liability, a preference that has quietly compounded for years.

The Week in Numbers

| Indicator | Reading |

|---|---|

| Bitcoin, spot price | ~$73,500 |

| US govt bitcoin holdings | ~328,000 BTC |

| Texas state BTC reserve | ~$10M, buying more |

| Fed reserve bill target | 1,000,000 BTC / 5 yrs |

| Hyperscaler capex 2026 | ~$700B (+77%) |

| Dollar, share FX reserves | ~56.9% (low since 1995) |

| China, rare-earth share | >90% |

| Taiwan, chip share | >90% |

What to Watch This Week

| Date | Event | Why it matters |

|---|---|---|

| Wednesday, June 3 | ADP payrolls and ISM services | The first reads on May hiring and the services economy, a warm-up for Friday's report; soft prints would revive bets on a Fed cut and lift risk appetite. |

| Wednesday, June 3 | Fed Beige Book | The Fed's district-by-district survey of activity, out about two weeks before its June meeting and read for how tariffs and the AI build-out are reaching the real economy. |

| Thursday, June 4 | Weekly jobless claims | Continuing claims have drifted higher in recent months; another rise would reinforce the picture of a labor market cooling beneath the headline. |

| Friday, June 5 | US jobs report | The week's main event. May payrolls, the unemployment rate, and wage growth steer the dollar, Treasury yields, and the odds the Fed cuts this month. |