June 16, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

Financial repression has two requirements, a cap on what savings earn and a way of keeping them from leaving, and a bitcoin held in self-custody is the first exit asset the inherited control stack cannot reach. This week's brief maps the three methods governments are using to close that exit, forbidding it, watching it, or replacing it with a custodial receipt, from South Africa's courtrooms to Europe's registers to America's ETFs. The contrast for allocators is the point: the same coins are a political fact when families hold their own keys, and a line in a forfeiture filing when a few custodians hold them.

Financial repression has two requirements: a cap on what trapped savings earn, and a way of keeping them trapped. Three weeks ago our weekly brief mapped the mechanisms being put in place to cap yields below the real rate of inflation. This week we cover the other half: the exits, and what is being done to close them.

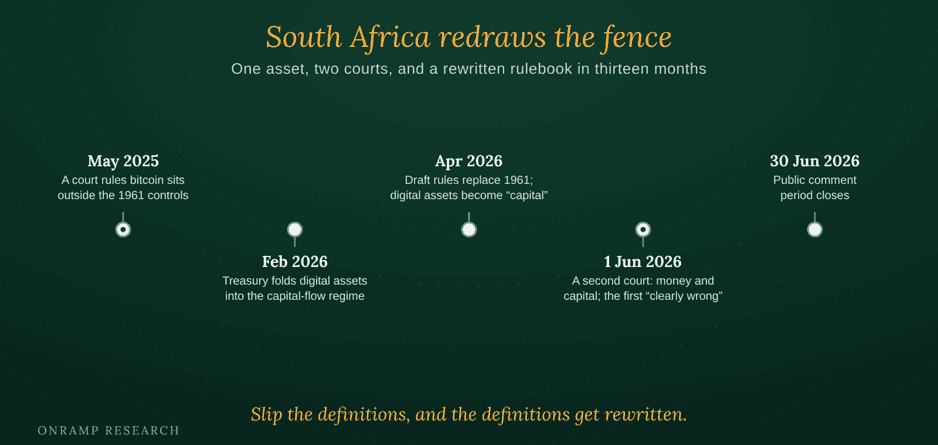

Something has been happening in South Africa this year that almost nobody outside the country has registered, and anyone with savings should.

Between 2018 and 2020, a South African named Square Mangundhla moved about 1,680 bitcoin out of his accounts at a local exchange and into wallets the state could not reach. They were worth roughly 182 million rand at the time. In 2022 the Reserve Bank seized what it could still reach, just under 6 million rand of bitcoin and cash left in his domestic accounts. The coins he had moved were already beyond government reach. He challenged the seizure, and for a while the law was with him: in May last year, in a related case brought by Standard Bank, a judge of the Pretoria High Court read the Exchange Control Regulations of 1961, the rules that govern what may leave the country, and found they say nothing about bitcoin. The asset, the judge held, was neither money nor capital as the regulations define them, and where a law that confiscates property is unclear, the doubt must favor liberty. The Reserve Bank appealed. The appeal is still pending.

The state did not wait for it. In February the finance minister announced that digital assets would be brought inside the capital flow framework, and in April the Treasury published the draft: a wholesale replacement for the 1961 regulations, classifying digital assets as capital for the first time, with new reporting duties and stiffer penalties. Then, on the first of June, a second judge of the same court decided Mangundhla's own case and reached the opposite conclusion, ruling that bitcoin is both money and capital and that the earlier judgment was "clearly wrong." The forfeiture stood. So as the law sits today, one judge says the asset is outside the fence, another says it was always inside, the appeal court will settle it eventually, and the Treasury has rewritten the fence in the meantime to make the argument moot. The public has until the thirtieth of June to comment on the new rules.

The natural reaction, reading this from London or New York, is a small shudder of relief. How heavy-handed. How unlike home.

That reaction is the blind spot. The same thing is underway in the reader's own country, and in most of the developed world, in forms that have not been recognized as the same thing, because they do not look like a man losing his coins in a Pretoria courtroom. South Africa is not a curiosity happening to other people. It is the version honest enough to be visible. Everywhere else, the work is quieter, and further along.

Repression needs a prisoner

Three weeks ago, this weekly brief described the machinery being assembled to hold America's debt at suppressed real yields: the doctrine, the conduit, the stablecoin bid. That is the cap, the first requirement of a financial repression, which works by paying savers less than inflation and letting the gap quietly erode the debt. But a cap on its own does nothing, because money that can flee a bad return will. When Carmen Reinhart and Belen Sbrancia at the IMF catalogued the repressions that cleared the debts of the last century, every one rested on a second requirement alongside the cap: savings that could not leave. The negative real rates that erased 87 points of American debt-to-GDP between 1946 and 1974 did the work only because Regulation Q capped deposits at home, capital controls watched the border, and the gold window had been closed to citizens since 1933. A repression with a working exit is not a repression. It is a price signal.

So the question that decides everything is what is happening to the exits. And here is what is new. For most of modern history the exits were already closed, quietly, by the ordinary plumbing of finance. Gold is heavy, declarable at every border, and held for most people by someone else; it was the classic escape, until 1933 showed how easily a custodied escape route is shut. Foreign bank accounts stopped being an exit when America made them visible in 2010 and the world's banks began turning Americans away. Property is registered by definition. Every traditional refuge was reachable, because every one of them runs through an institution that answers to the state.

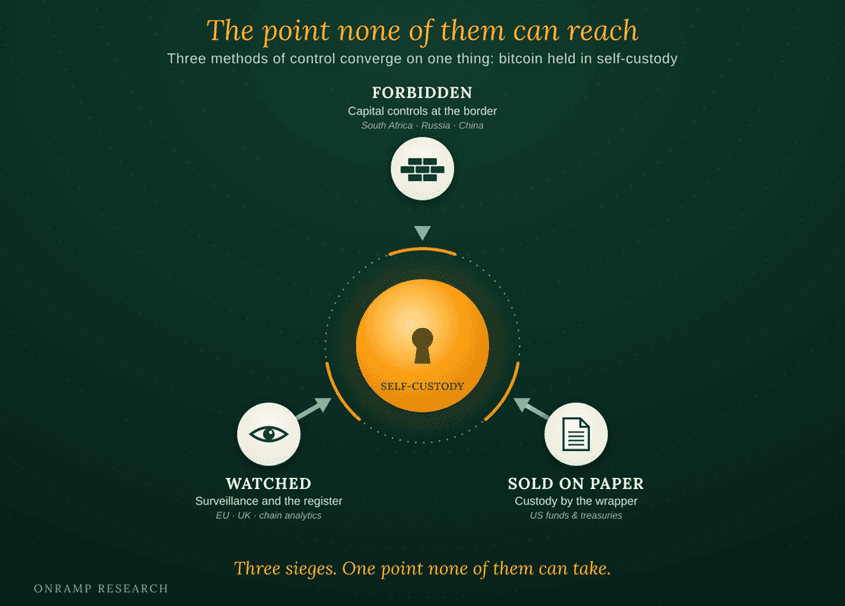

A bitcoin held in self-custody is the first exit asset that does not. It crosses any border with no custodian, no counterparty, and nothing to declare, carried in a memorized phrase or a file: the first store of value in a century that the inherited control stack does not reach. That is the reason governments are building what they are now, and the reason it is happening in so many countries at once. They are all focused on the same exit, and the exit is the same everywhere. What follows is how they are attempting to guard that exit route: three methods, in rising order of sophistication.

The exit can be forbidden

The first method is the oldest and the bluntest. The state declares that the asset may not cross its border, or makes the crossing so costly that few attempt it.

This is South Africa's method, dragged into the open by litigation, and it is the common shape across the emerging world. China sits behind a ban on trading and mining, stacked on the fifty-thousand-dollar annual limit that has fenced household savings for decades. Turkey, where citizens flee the lira through dollar stablecoins, now holds every withdrawal of digital assets for two days and caps stablecoin transfers at three thousand dollars daily. Nigeria built the wall and watched it fail. The central bank cut exchanges off from the banks, blocked their websites, and froze the accounts of citizens selling naira for dollars, all framed as a defense of the currency. The trade moved to peer-to-peer channels and kept going, so Nigeria gave up forbidding and switched to licensing and taxing instead, abandoning the first method for the more sophisticated ones.

Russia has built the most extreme version, and it is the most revealing. Under a law taking effect this year, domestic payments are banned, retail buyers capped at roughly four thousand dollars a year, transfers to personal wallets restricted by design, and from 2027 unregistered digital currency becomes a criminal offense carrying prison or forced labor. Yet the same law legalizes digital currency for the state's own cross-border trade, formalizing the channel through which Russia routes an estimated 240 billion dollars of sanctioned commerce around the banking system. The citizen's exit is criminalized. The state's exit is built into national infrastructure. That contradiction gives the game away. This was never about the dangers of the asset, which the state is happy to use. It is about who is permitted to leave.

The trouble with forbidding is that it leaks. Nigeria proved it; a determined holder routes around a prohibition, and the coins move anyway. A wall stops the law-abiding and the lazy, not the motivated. Which is why the more capable states have moved on to a method that does not try to stop the exit at all.

The exit can be watched

The second method abandons the border and goes after something subtler: the privacy that makes the exit usable. It does not forbid the coins from moving; it makes sure every movement is seen.

In Europe this is now law. The Anti-Money Laundering Regulation, in force from 2027, bars regulated platforms from handling anonymous accounts or privacy coins, requires identity verification on transactions with self-hosted wallets above a thousand euros, and by 2029 will stand up a central register of digital asset holders across the bloc. The United Kingdom runs a parallel registration and travel-rule regime. The OECD's reporting framework will have dozens of jurisdictions automatically swapping account data from 2027, doing for digital assets what an earlier framework did for offshore bank accounts. None of this stops anyone from leaving. It removes the thing that made leaving worthwhile, which is the absence of a watcher.

And the watching is not only the state's. A private industry has grown up to do what the protocol's public ledger invites, selling deanonymization to governments as a service. Chainalysis, the largest, has earned tens of millions from federal contracts across nearly every American agency that enforces anything, from the FBI and the IRS to the DEA, the SEC, and the Air Force, with at least one contract aimed squarely at breaking the privacy tools that frustrate tracing. Observers have likened it to a Palantir for the blockchain. The scale is telling in its disproportion to the stated cause: by the surveillance industry's own measure, illicit activity was around a seventh of one percent of all flows in 2024, a fraction far too small to explain a monitoring apparatus that large. The apparatus is not built for the fraction. It is built for everyone, so that the chain becomes as legible to the authorities as a bank ledger.

This is the quiet destination of the second method: a digital asset watched so completely that it gains the central feature of a central bank digital currency, total visibility to the state, with no one having to issue one.

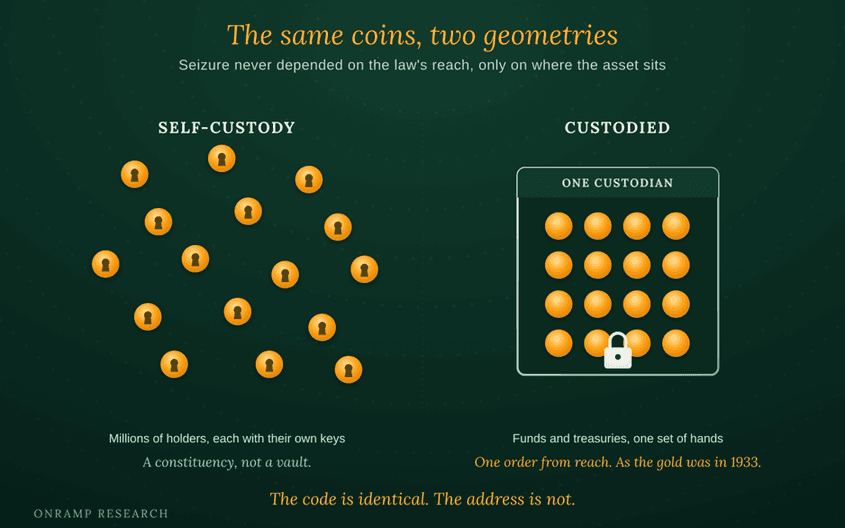

But watching has a limit, and it explains the third method. Surveillance maps the coins; it does not gather them. After all the registers and the tracing, the coins are still sitting in millions of separate wallets, each holding its own keys. The state knows where they are and still has to reach them one at a time. A million holders are a constituency, not a vault. To close the exit completely, you do not want to know where the coins are. You want them in your hands, and the holders glad to have put them there.

The exit can be replaced with a receipt

The third method is the most sophisticated, and it is the American one. It needs no ban and no surveillance pointed at citizens, because the citizens arrive willingly. You simply let the demand for the asset flow into instruments that hold it on the buyer's behalf.

This is the great American adoption story of the decade, the spot funds (ETFs) and the treasury companies, and it deserves to be seen for what it also is. Every rail carrying serious money into the asset is custodial by construction. A retirement account cannot hold a memorized phrase. A registered adviser must use a qualified custodian. A corporate treasury answers to auditors who require one. So every dollar of institutional adoption, however much it is celebrated, is by definition custodied adoption. The funds hold their coins at custodians, overwhelmingly at one. The largest corporate holder owns about three percent of all the bitcoin there will ever be. Stack the disclosed mandates together and, by credible estimates, more than a tenth of the entire supply now sits behind a single custodian, in a single jurisdiction, within reach of a single order.

The third method delivers what the others cannot, all at once: the coins' location is known, because they sit in reporting brokerages; they are concentrated, because a few custodians hold them; and the custodians are controllable, because they are regulated businesses that can be directed, quietly, by the authorities that license them. Forbidding leaks and surveillance only maps, but this gathers, and it gathers while the holder believes he has bought the very thing he has surrendered. A fund share cannot be redeemed by its holder for the coins behind it; that right belongs to a few authorized firms. A treasury company's stock is a claim on a corporation that owns coins, which is not a claim on the coins at all. The buyer holds a receipt for an exit he cannot take, and when he sells, what reaches him is dollars, the currency he was trying to leave.

This is the precondition of 1933, rebuilt. The gold order of that year did not work by searching houses. It worked because decades of custodial habit had already gathered the metal into banks, so the seizure ran through the banks' own ledgers and tellers; the gold in mattresses largely stayed where it was. Concentration in trusted institutions is what makes an exit closeable later, by a single instruction. The American method is assembling exactly that concentration, voluntarily, at market prices, with the holder grateful for the convenience of not holding his own keys.

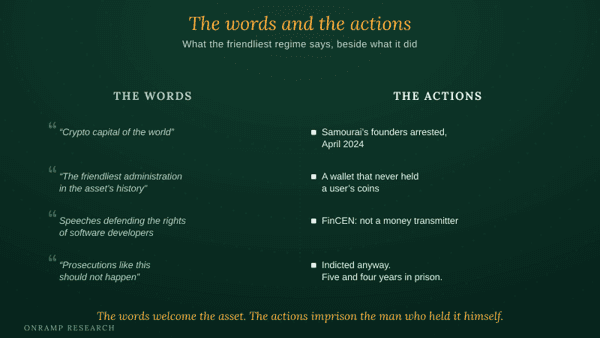

Watch what happens, then, to the people who build the tools that would let a holder step outside all of this. In April 2024 the two founders of Samourai Wallet, a service that let users hold their own coins and mix them for privacy, were arrested and charged with money laundering and running an unlicensed money transmitter. The software never took custody of a single coin. The agency that defines money transmitters, FinCEN, had told the prosecutors in writing that a non-custodial tool like this one does not qualify. The Southern District of New York indicted anyway, on the theory that the software exercised "functional control" it plainly never had. The founders pleaded guilty in July 2025 to the surviving charge, and in November were sentenced to five years and four years in prison.

The state's case was not imaginary. Prosecutors showed the founders promoting the mixer on a darknet forum and inviting hackers to send stolen funds through it, and the flows touched real crimes: fraud, sanctioned trade, the worst kinds of material. The tool was used for what its critics feared, and its makers knew. Grant all of that. Then set it beside the words coming from the same government in the same months. This is the administration that calls itself the friendliest to the asset in history, that promises to make the country the capital of the industry, whose own senior officials gave speeches defending the rights of developers and said prosecutions like this one should not happen. The words welcome the asset. The actions imprison the man who built a way to hold it privately and move it unwatched, on a legal theory the government's own expert agency had rejected, while the custodial wrappers that gather everyone else's coins are not merely permitted but championed.

There are two ways to read what's behind that gap, and it is not necessary to choose. One is design: a program to channel the asset into reachable form and criminalize the tools of escape. The other is incidence, no plan at all, only a set of agencies each pursuing its own mandate, a Treasury that needs buyers for its debt, an enforcement arm that needs sanctions to bite, an industry that wants a product to sell, the sum of their separate interests happening to gather the asset into custody and punish the alternative. The point worth sitting with is that the architecture is identical either way. Whether by intention or by the drift of incentives, the coins end up in the banks, and the man who offered a way around the banks ends up in prison. The words say one thing. The actions build the other.

What the three are aiming at

The three methods converge on a single point: the moment a coin passes into a wallet that only its holder controls. That moment is what the South African is being prosecuted over, what the European register is built to capture, and what the American wrapper is designed to prevent. It is the one thing none of the methods can tolerate, because it is the one thing none of them can reach.

The Samourai prosecution sits beneath all three as the floor, because the privacy tools it criminalized are what defeat every method at once. A coin held in self-custody and moved without a watcher slips the border control, blinds the surveillance, and was never in the wrapper to begin with.

There is information in the whole edifice. States do not legislate against things that cannot happen; no one forbids, surveils, or quietly gathers information about an exit that does not function. Every wall, every register, every wrapper is a confession that the exit is real, and that the people building the controls expect them to be used. The exit's strength was never in its cryptography, which is identical for the coins that left South Africa and the coins that stayed. It is in distribution. Ten million families holding their own keys are a political fact that no single order can undo. The same coins behind three custodians are a line in a forfeiture filing, the outcome of which is determined by a branch of the same government regulating those custodians.

Gold proved both halves of this long ago. It was the exit once, and it was closed, and the closing worked because the gold was already in the vaults. Its own escaping form, the coin in a drawer, was always too heavy to carry far, too obvious at the border, too small to matter at scale. The escaping form of bitcoin has none of those limits, which is why so much infrastructure, legislation and regulation is being built to guard the exits before the habit of holding it spreads. The coins that left Luno (the South African exchange) were not protected by their code. They were protected by who held the private keys to its new address.

In Pretoria, the comment period closes on the thirtieth of June. The appeal will be heard in due course. The coins have not come back.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

The longest outflow streak yet

Spot bitcoin ETFs have never seen a month like the one that just ended. From May 15 to June 3 the funds bled money for thirteen straight sessions, the longest losing streak since they launched in 2024, shedding about $4.33 billion and 59,000 coins. The selling was not really about bitcoin. It tracked a change in what the Federal Reserve is expected to do: a hot jobs report and a 4.2% inflation print killed off any hope of a rate cut, the ten-year Treasury yield pushed to 4.82%, and the carry trades built on top of the ETFs unwound in a hurry. The coin fell from about $80,000 to $63,000, and the fear gauge dropped into single digits. Then, on June 12, the funds took in money again, an $86 million day led by BlackRock. The year's flows are now negative; the lifetime total is still firmly positive. The market is deciding which of those two facts matters more.

Clarity clears committee, races the clock

The most consequential digital-asset bill in US history is sitting on the Senate calendar, and the calendar is the problem. The Senate Banking Committee advanced the Clarity Act on May 14 by 15 votes to 9, all thirteen Republicans joined by two Democrats. To become law it still needs sixty votes on the floor, reconciliation with the Agriculture Committee's version, a merger with the House bill passed last fall, and the president's signature. The sticking point is an ethics provision restricting government officials from profiting off the industry, a clause whose origin is the president's own holdings, which Democrats demand and the White House will not accept if it is aimed at him. Roughly eight weeks remain before the summer recess. For scale, last year's stablecoin law cleared the Senate 68 to 30.

The fight over stablecoin yield

A quieter battle runs underneath the Clarity Act, and it is about interest. Last year's GENIUS Act barred stablecoin issuers from paying yield to the people who hold their tokens. But exchanges can still offer rewards that look a great deal like interest, and the American Bankers Association wants the new bill to close that gap. The banks' worry is competitive: a dollar token that quietly pays a return is a checking account that skips the bank. The industry wants the rewards kept. How it lands will decide whether stablecoins stay a payment rail or drift toward something closer to deposits, and who gets to hold the float. With those reserves parked in Treasury bills, the question is larger than it looks.

AI & Financial Infrastructure

A trillion dollars, off the chips

The AI chip trade had its worst week in years. The trigger was Broadcom: strong results, with AI revenue up 143% from a year earlier, but the company declined to raise its full-year AI target, and the stock fell 20% over two days, erasing roughly $450 billion in value, an entire Costco. The Philadelphia semiconductor index dropped 10.4% on June 5, its worst single day since March 2020. By the time a 4.2% inflation print landed on June 10, the rout had widened: Nvidia, AMD and Intel all fell hard, and the AI server maker Super Micro sank nearly 20% on its own $7 billion stock sale. One tally put the value wiped across AI chips at $1 trillion. None of it changed the demand story. What changed is the price investors will pay for earnings a decade out when rates are no longer falling. Oracle's results and Nvidia's June 22 entry into the S&P 500 are the next tests.

SpaceX lands the largest IPO ever

SpaceX, which folded in Elon Musk's AI company xAI in February, went public on June 11 in the biggest listing on record. It priced 555 million shares at $135 for a $75 billion raise, topping Saudi Aramco's old mark, then jumped 19% on its first day to close at $161. That lifted the company above $2 trillion, worth more than Tesla. Two things stood out for allocators. First, a line in the filing: the company "may issue a significant amount of equity in connection with future transactions," which Wall Street read as a signal that a Tesla merger, the largest in history, is on the table. Second, the quiet winner is Alphabet, whose 4.9% stake is now worth about $105 billion. The caution sits in the same documents: xAI lost $6 billion last year and is on track to burn $10 billion this one. OpenAI and Anthropic are expected to follow with giant listings of their own.

The squeeze reaches the shelf

The cost of building artificial intelligence is starting to show up in the price of ordinary electronics. Memory is the pinch point. With data centers absorbing supply, Gartner expects memory costs to climb sharply, and device makers are already passing it on. IDC warned that global smartphone shipments could fall 13% this year, which would be the lowest in a decade, as dearer components meet softer demand. The pattern is worth naming. The same buildout that lifts the chip stocks raises the bill for the phone in a buyer's pocket, and it does so through the supply side, where higher interest rates offer no help at all. It is inflation a central bank cannot tighten away.

Geopolitics & Markets

Oil slips as a deal nears

For the first time since February, the energy market is pricing peace rather than war. Brent crude, which averaged $107 in May, fell to about $87 by the weekend on reports that the United States and Iran are close to a deal. An Iranian draft, fourteen points long, would lift oil sanctions and commit Tehran to reopening the Strait of Hormuz within thirty days; a Trump administration official put the odds of a signing at 80%. Nothing is settled. The Iranian and American versions of the terms differ, and the president disputed the text that leaked. And even a deal does not bring the oil back quickly: Saudi Aramco's chief executive warned that if the strait reopened today the market would still need months to rebalance, and that any delay pushes normalization into 2027. The waterway has now been shut for more than three months. Prices remain over 20% above where they sat before the war began.

The Pentagon's list goes commercial

The Pentagon expanded its blacklist of Chinese military companies to 188 firms this month, up from around 130, and the new names are not defense contractors. They are the commercial heart of China's technology economy: Alibaba and Baidu, which underpin much of the country's AI infrastructure, the electric-car makers BYD and NIO, and the robotics firm Unitree. From June 30, the Department of Defense may not contract with any of them. The stated basis is "military-civil fusion," Beijing's policy of enlisting private firms for state ends, a doctrine broad enough that critics note it could sweep in almost any large Chinese company. The firms reject the label and have threatened to sue. The timing is awkward, landing weeks after the president met Xi Jinping and announced a trade truce. One lobbyist caught the unease: by this logic, he said, Ford and GM would be American military companies.

The war reaches the price level

The clearest economic legacy of the Iran war is no longer at the pump. It is in the inflation data. May's consumer prices rose 4.2% from a year earlier, the most in three years, and energy did the work, up 23.5% over twelve months. Strip energy out and the picture is calmer: core inflation cooled to 2.9%. That split is the whole problem for the Federal Reserve, which meets this week. A supply shock from a closed shipping lane is not something interest rates can fix; raising them does nothing to reopen the Strait of Hormuz. The European Central Bank has already tightened into the war. The Fed, under new leadership, now has to decide how much of an energy spike to look through, and how much to lean against. Geography has acquired a say in monetary policy.

The Week in Numbers

| Indicator | Reading |

|---|---|

| May US CPI, the highest in three years | 4.2% |

| Energy prices over 12 months, the inflation driver | +23.5% |

| Spot bitcoin ETF outflows over a record 13-session streak | $4.33B |

| Where bitcoin trades, down from $80,000 in mid-May | ~$66.5K |

| The fed funds range Warsh inherits, held since December | 3.50-3.75% |

| Futures-implied odds of a Fed rate hike by year-end | 56% |

| Broadcom's market value erased in two days | ~$450B |

| Value wiped from AI chip stocks in the selloff | $1T |

What to Watch This Week

| Date | Event | Why it matters |

|---|---|---|

| Wed, Jun 17 | FOMC Decision | The FOMC decision and Kevin Warsh's first press conference as chair. A hold is all but certain; the news is in the projections. The dot plot's last 2026 rate cut is expected to vanish, and Warsh may move to scrap the dot plot altogether. The most watched policy event of the year. |

| This week | Deal to Open the Strait of Hormuz | Whether Washington and Tehran sign the 14-point draft to reopen the Strait of Hormuz within thirty days. Oil's direction hangs on it, though Aramco warns the market needs until 2027 to fully normalize either way. |

| Mon, Jun 22 | Nvidia joins the S&P 500 | Nvidia joins the S&P 500, forcing index funds to buy the market's most rate-sensitive megacap into a hawkish Fed. |

| Tue, Jun 30 | Pentagon's Contract Ban | The Pentagon's contract ban on the 188 listed Chinese firms takes effect, with almost no runway for the US contractors that must comply. |