June 23, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

Everyone argues about the interest rate, but the number that quietly defines money is settlement: how long until a payment is truly, finally done. This week's brief traces that hidden variable from a 300-million-dollar fiber-optic tunnel built to shave three milliseconds off a trade, through the 1968 paperwork crisis and the 1974 Herstatt failure, to the remittance corridors where the poorest still wait days at over 6 percent, and shows the delay is institutional, not physical. The stablecoin is finally closing the gap, settling in seconds for cents anywhere on earth, but it keeps a gatekeeper who can freeze a balance, leaving one instrument that settles finally for everyone and answers to no one.

Everyone argues about the interest rate. Almost nobody asks another question that defines money: how long until a payment is truly, finally done. Exploring the answer turns out to produce a map of who holds power and who waits.

In the spring of 2009, in the hills of Pennsylvania, a crew of around two thousand men began blasting a tunnel through rock. They were paid well and told almost nothing. The line they were laying had to run as close to a straight line as the geology allowed, more than 800 miles of it, from a data center in Chicago to one in Carteret, New Jersey, and the men were instructed to keep quiet and to report anyone who asked what they were building. When locals wondered aloud whether it was a government secret, no one corrected them.

It was not the government. It was a company called Spread Networks, and the thing it was building was a fiber-optic cable whose only purpose was speed. The existing cables between Chicago and New York zigzagged along railway routes and around mountains. Spread's would go nearly straight, and that straightness was worth, by the company's reckoning, about three milliseconds. The cable cost roughly 300 million dollars and it cut the round trip for a pulse of light between the two cities from about sixteen milliseconds to thirteen and a third. Three thousandths of a second, for 300 million dollars. The firms that leased access paid millions each and were not told what the line had cost or who else was on it.

Three milliseconds is about a twentieth of the time it takes to blink. Why would anyone pay a fortune for it? The answer to that is the subject of this week's brief, and it reaches far beyond a tunnel in Pennsylvania. What those traders were paying for is a feature of money itself, one almost nobody thinks about, and it shapes far more than the price of a trade.

The number nobody watches

Ask an expert what determines the value of a currency, and you will hear about the interest rate. It is the most watched number in the world. Central banks move it, markets hang on it, we talk about it a lot. But the interest rate is only half of what makes money behave the way it does. The other half is settlement: the speed at which a payment becomes final, irreversible, and truly yours.

Most people assume money moves the instant they send it. It does not. When you tap a card or send a transfer, what travels first is a message, a promise that the money will follow. Between the promise and the settlement there is a gap, sometimes seconds, sometimes days, and inside that gap the payment is not yet real. It can fail. It can be reversed. The person who is owed does not yet have the money, and the person who owes it still does. It is this gap between a promise and settlement that is the most underrated thing in finance, because it is where the risk and the profit exist.

A trade and its settlement are two different moments. The traders care about the speed of the signal that lets them buy before a rival. But the more important detail relevant to monetary operations is the hard problem of deciding when a payment is done.

The invention of done

It is easy to forget how recently "final settlement" was invented, because we now take it for granted. For centuries a payment was a provisional thing, a paper claim that could bounce, be lost, or be clawed back.

Wall Street nearly drowned in exactly this problem within living memory. Through the 1960s, every share traded on the New York Stock Exchange settled by physically moving a paper certificate from seller to buyer, carried by messengers up and down the street. As trading volume climbed past twelve million shares a day, the back offices, known without affection as the cages, could not keep up. Certificates piled up unprocessed. They were misdelivered, lost, and stolen by the hundreds of millions of dollars; the attorney general of the day estimated that organized crime had made off with some 400 million dollars of securities in the chaos. Trades routinely failed to settle within the five days the rules allowed. The exchange's response, in the second half of 1968, was to stop trading every Wednesday and shorten its hours the rest of the week, simply to let the paperwork catch up. It was not enough. When volume fell in the bear market that followed, the weakened brokers went under, and by 1970 roughly one in six member firms had failed, merged, or been swallowed. The bull market that followed exposed the truth that the plumbing of the world's largest exchange could not actually settle the trades it was making.

The cure was to stop moving the paper. In 1973 the industry created a central depository that held the certificates still in one vault and simply changed the names in a ledger, the model that underpins markets to this day. But all it really did was shorten the gap between trade and settlement. It did not remove it. The United States took until 1995 to move stock settlement to three days after a trade, until 2017 to get to two, and only in May 2024 to reach one. More than half a century after the cages, the most advanced equity market on earth still does not settle a share trade until the next day.

If the 1968 crisis showed what happens when settlement is too slow, an afternoon in Cologne six years later showed what happens in the gap when one side fails. On 26 June 1974, German regulators pulled the license of Bankhaus Herstatt, a mid-sized bank that had lost badly trading currencies. They closed it at half past three in the afternoon, Frankfurt time, which was chosen to minimize panic at home. It did the opposite abroad. That morning, banks around the world had paid Herstatt Deutsche marks, expecting US dollars in return when New York opened. New York was just starting its day when the bank's doors shut. The marks were gone. The dollars never came. Counterparties lost what would be close to a billion dollars in today's money; one American bank alone faced 156 million. Herstatt was only the thirty-fifth largest bank in Germany, and its failure in the settlement gap nearly seized the entire global payment system.

The industry gave the danger a name, Herstatt risk, the risk that you pay one leg of a deal and your counterparty vanishes before paying the other. And it spent the next twenty-eight years building machinery to close the gap, culminating in a utility called CLS that settles foreign-exchange trades on a strict principle: both legs at the same instant, or neither. CLS describes its own work, accurately, as unglamorous plumbing. That is what mitigating settlement risk took: not a breakthrough but plumbing, built slowly and at great cost to compress a gap that nobody outside the system ever sees.

Russia has built the most extreme version, and it is the most revealing. Under a law taking effect this year, domestic payments are banned, retail buyers capped at roughly four thousand dollars a year, transfers to personal wallets restricted by design, and from 2027 unregistered digital currency becomes a criminal offense carrying prison or forced labor. Yet the same law legalizes digital currency for the state's own cross-border trade, formalizing the channel through which Russia routes an estimated 240 billion dollars of sanctioned commerce around the banking system. The citizen's exit is criminalized. The state's exit is built into national infrastructure. That contradiction gives the game away. This was never about the dangers of the asset, which the state is happy to use. It is about who is permitted to leave.

The trouble with forbidding is that it leaks. Nigeria proved it; a determined holder routes around a prohibition, and the coins move anyway. A wall stops the law-abiding and the lazy, not the motivated. Which is why the more capable states have moved on to a method that does not try to stop the exit at all.

The tiers of speed

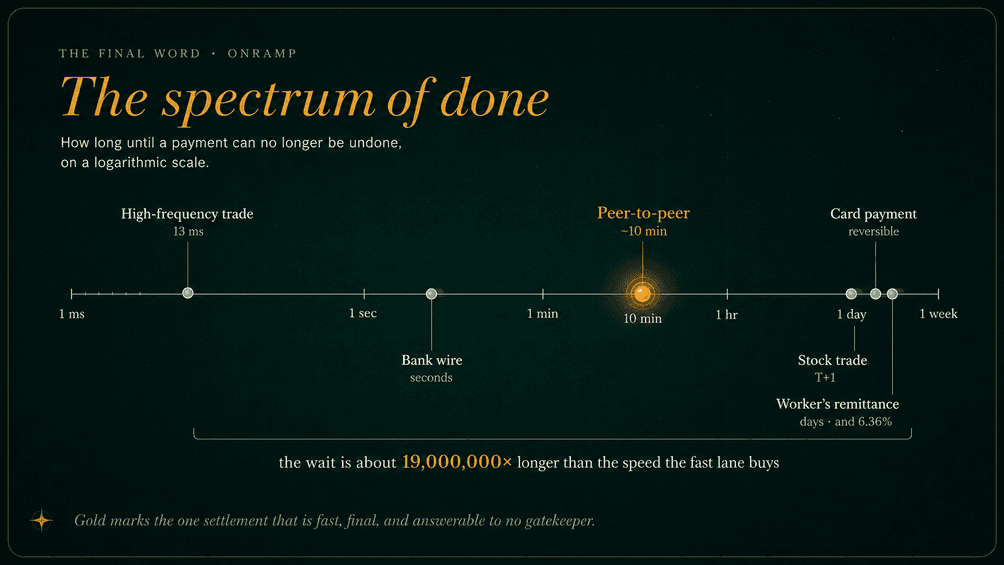

Here is where the hidden variable becomes a hierarchy, because the speed of settlement is not handed out evenly. It is rationed, and where you sit in the rationing is a precise measure of your power.

At the top, banks pay each other over systems like Fedwire, which settles in real time and with finality: the money moves, irrevocably, in seconds, during business hours. This is the fast, final settlement that the rest of the system only imitates. A tier down, large dollar payments between banks can run through netting systems that tally up all day and settle the difference at the close, which is efficient but reintroduces exactly the end-of-day gap that killed Herstatt's counterparties.

Then there is the rail that ordinary people use. In much of the world a normal bank payment still travels by batch systems that take one to three days to settle, which is why your transfer "pending" on a Friday lands on a Tuesday. A card payment feels instant, but the authorization and the settlement are different events: the merchant waits days for the money, and a chargeback can reverse it after the fact. You did not actually have the money when the screen said approved. You had a promise.

And at the bottom of the hierarchy sit the people with the least, paying the most and waiting the longest. A migrant worker sending wages home does not move money so much as hand it to a chain of intermediaries. Cross-border, there is no single network; banks hold accounts with each other, a message passes down the correspondent chain, and each link takes its time and its cut. The result is a global remittance market that moved about 905 billion dollars in 2024, larger than all foreign aid and direct investment combined, at an average cost of 6.36 percent, rising near 9 or 14 percent if you are unlucky enough to use a bank, and far higher than that in the poorest corridors of Africa. On the most-quoted rate, the fees alone skim something on the order of fifty billion dollars a year from the people who can least afford it, and the money can take days to arrive. The World Bank still classes "less than five days" as a speed category worth measuring. The poorest people in the system are living, in 2026, with the settlement times of 1968.

That is the pattern, once you see it. The same act, sending money, settles in seconds for a bank, in days for a worker, and in three thousandths of a second, at the very top, for a trading firm that paid 300 million dollars to shave the last sliver of delay. Inside every one of those gaps, someone else holds the money and earns on it, the income called the float.

What is physics and what is hierarchy

You might assume these delays are technical, the unavoidable friction of moving value across distance. They are not, and the proof is in the tunnel.

Spread Networks got the Chicago-to-New York round trip down to about 13.3 milliseconds. That is not a little above the physical limit; it is essentially at it. Light through glass travels at about two thirds of its speed in open air, and on that 827-mile route the laws of physics permit a round trip of roughly 13 milliseconds and no faster. Spread had built a cable that ran almost as fast as physics on that route allows. Which is exactly why its advantage died within two years: rivals realized that radio through open air beats light through glass, because air slows light less than fiber does, and microwave towers leapfrogged the cable. Spread, having spent 300 million dollars, sold itself a few years later for 127 million, less than half. It had reached the limit physics set, and once a route is that fast there is no more speed to buy.

Hold that against the worker's remittance. There is no physical reason a payment from London to Lagos should take three days. The signal could cross that distance in well under a tenth of a second. The three days are not the speed of light. They are the speed of trust, the time it takes for a chain of institutions that do not fully trust each other to send messages, check balances, manage their risk, and reconcile their ledgers. The fast lane is limited by physics; the slow lane is limited by intermediaries. And the difference between them is staggering. The wait the poorest endure is something like nineteen million times longer than the delay the richest spend fortunes to remove. Almost none of that gap is physical. It is institutional. The delay is a choice, not a law of nature.

The gap is closing now

This week's brief is not an historical piece. The gap between a promise and a payment is still, at this moment, the most contested ground in finance, and the thing closing that gap, is the stablecoin.

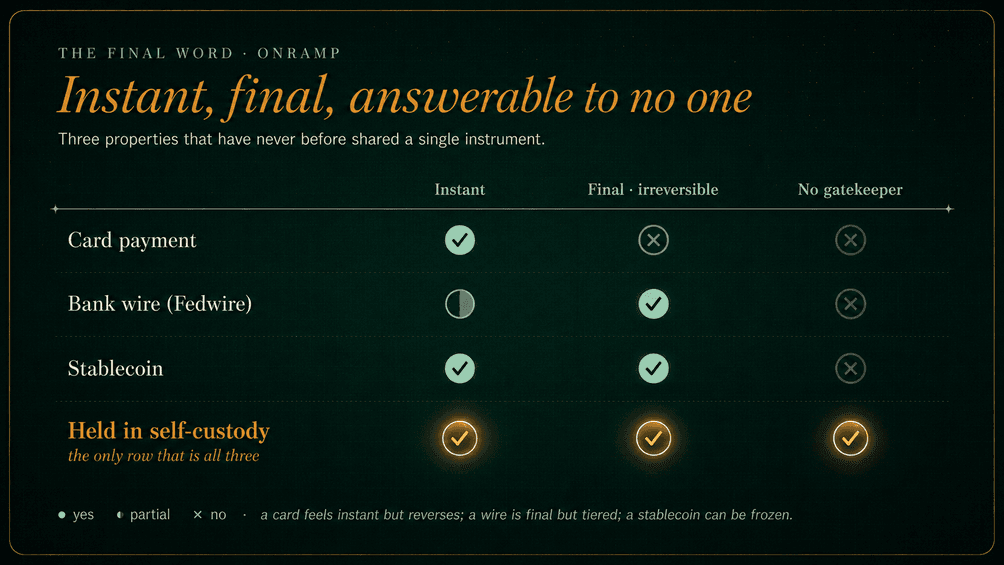

A stablecoin is a dollar issued as a token on a public network, and it settles the way the old system never could: in seconds, at any hour, on any day, for cents, anywhere on earth, with no chain of correspondent banks taking days and percentages in the middle. The market has noticed. By 2025 stablecoins were settling somewhere between ten and thirty trillion dollars a year depending on how you count, rivalling or exceeding Visa even on the conservative measures that strip out trading churn, and the slice that is real-world payment rather than speculation doubled to around 400 billion dollars, most of it between businesses. The United States wrote them into law with the GENIUS Act in 2025, and as this column publishes the Senate is weighing the bill that would finish the framework. Their issuers, parking the reserves in Treasury bills, have quietly become one of the largest holders of US government debt on earth. After half a century of unglamorous plumbing, the settlement gap is collapsing in real time, for exactly the cross-border and business flows the correspondent system left stranded at three days and six percent.

But let's look more closely at how the gap to final settlement is actually being closed, because the method being used exposes what's not being noticed. A stablecoin settles instantly and finally, and yet the balance sits at the mercy of its issuer, who can freeze it, and in practice does freeze it, at a request from law enforcement, with a single line of code. Roughly nine in ten stablecoin dollars are issued by just two companies. The delay has been removed and a gatekeeper installed in its place, one who can reverse what looked final and seize what looked like yours. It is a real and enormous improvement on three days and a chain of banks. It is not the same thing as money that no one can stop.

The oldest question

Money has always been an answer to a single question: how do I give you value in a way that is final, that you can trust, that cannot later be undone. Gold answered it by being a physical thing that changed hands; settlement was instant because possession was the settlement, but it could not move across the world at the speed of light. The entire apparatus of modern finance, the depositories and the wires and the clearing houses and the unglamorous plumbing of CLS, is an attempt to get the finality of handing someone a gold coin while also moving it at the speed of light, and to do it for a system far too large to settle by hand. For a century, and at great cost, the system has narrowed that gap without ever closing it. It has only rationed it, handing speed and finality to those at the top and leaving everyone else to wait.

So it is worth asking what it would mean to actually close the gap. To have settlement that is final, the way a gold coin is final, with no counterparty who can vanish in the afternoon and no chain of intermediaries taking days and percentages. To have it run at the same speed for everyone, the bank and the worker alike, with no privileged tier that buys its way to the front. For all of history that was impossible, because final settlement required a trusted third party to stand in the gap and declare the payment done, and a trusted third party, by its nature, decides whom to serve quickly and whom to keep waiting, and keeps the power to undo what was meant to be final. The gap was never only technical. It was the space the intermediary occupied, charging for the wait and deciding who had to endure it. The stablecoin, for all its speed, removes the delay but keeps the centralized gatekeeper.

There now exists one form of money that does better. It settles with finality for anyone who holds it, anywhere, in the same handful of minutes; it asks no intermediary's permission; and it offers no one, not even its makers, the power to reverse the payment or freeze the balance. Newer layers settle it faster than you have read this sentence. Instant, final, and answerable to no gatekeeper: three properties that have never before shared a single instrument.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

Wall Street's plumbing moves on-chain

The story in digital assets this year is not bitcoin's price. It is how fast traditional finance is rebuilding itself on blockchain rails. Tokenized real-world assets, mostly US Treasuries wrapped as tradable tokens, hit a record near 32 billion dollars in June, up more than 200 percent in a year. Tokenized Treasuries make up roughly 15 billion, and Circle's USYC, near 3 billion, has overtaken BlackRock's BUIDL for the lead. The appeal to an institution is plain: a yield near 3.4 percent, redeemable around the clock, that settles in minutes and doubles as collateral. The base layer of finance is quietly moving on-chain.

The frontier moves to private markets

With tokenized Treasuries proven, the harder prize is equity in companies ordinary investors cannot buy. Now that SpaceX has gone public, the race has moved to the private AI giants: platforms are wrapping claimed exposure to OpenAI and Anthropic, both of which have just filed to go public, into tradable tokens. The pitch is access; the catch is the legal claim behind the token. In May, tokens tracking the two firms fell about 40 percent after both companies said the share transfers behind them were unauthorized and possibly worthless. A token is only as good as the shares it claims to hold.

Perpetuals come onshore

For a decade the most heavily traded instrument in digital assets was one Americans could not use: perpetual futures, a roughly 90-trillion-dollar-a-year market, entirely offshore. In June that changed. Kalshi, the regulated prediction-market exchange, launched the first US perpetuals with the blessing of the CFTC. Demand was startling: more than 5.5 billion dollars in two weeks, with three straight days above a billion, helped by World Cup and NBA Finals contracts. The waitlist had topped a million.

AI & Financial Infrastructure

The boom's electricity bill arrives

The cost of building artificial intelligence is showing up on household power bills, and the politics are turning. Wholesale electricity on PJM, the largest US grid, jumped 76 percent in the first quarter from a year earlier, driven by data-center demand; residential prices nationally are up over 40 percent since 2019. Senator Elizabeth Warren blames the hyperscalers; the industry points to aging grids and market design. On June 18, federal regulators voted to speed data centers onto the grid while ordering them to pay the full cost of their upgrades. The proof will be in monthly bills.

The grid cannot keep up

Even with the money, the boom is hitting physics. The wait to connect a large new data center now runs four to six years in the United States, and up to ten in Tokyo, because power plants take years to build while a data center takes months. The result is backlash and retreat at once: Maine has banned new large data centers, Virginia is fighting over who pays, and a record number of projects were cancelled in the first quarter. Demand could reach 1,300 terawatt-hours by 2035, near triple 2024, but the gap between announced and powered keeps widening.

The scramble for power

To escape the queue, the hyperscalers are buying their own electricity, and increasingly that means nuclear. Meta has signed for up to 6.6 gigawatts; Microsoft is paying to restart a reactor at Three Mile Island; and Amazon is buying power straight from a Pennsylvania nuclear plant. Only nuclear offers the round-the-clock power a frontier model needs. It is a striking turn for an industry that promised to run on wind and sun.

Geopolitics & Markets

Beijing aims at America's rare-earth exit

China answered Washington this week, and it aimed precisely. On June 22, Beijing's commerce ministry added ten American firms to its export-control list, retaliating for the Pentagon expanding its list of Chinese military companies. The targets were telling: MP Materials and USA Rare Earth, the two firms Washington funds to cut its dependence on Chinese rare earths. The Pentagon owns about 15 percent of MP. Beijing chose to constrain the very companies built to escape its grip. The leverage is real: China makes 94 percent of the world's permanent magnets. Markets shrugged, but the message was unmistakable.

Iran war ends, the strait reopens

After nearly four months, the Iran war is ending. The United States and Iran signed a framework agreement in Switzerland on June 19, and the Strait of Hormuz, shut since late February, is reopening. Oil has been pricing the relief for weeks: Brent, which averaged 107 dollars in May, has eased toward the high 80s as the war premium drains away. The terms include sanctions relief, and Washington has signaled China may keep buying Iranian crude. For the first time since winter, the Gulf is moving toward calm.

Europe rearms on a borrowed supply chain

Europe's rearmament is now hard to overstate. Germany's 2026 defense budget will reach about 117 billion euros, double its 2021 level, and military spending has grown for twelve straight years. The driver is Russia and a newly unreliable American patron. But the buildout rests on an awkward dependency the week underlined: the magnets in its missiles and drones rely on rare earths China controls, at up to six times China's own prices. It is the largest buildup since the Cold War, on a rival's supply chain.

The Week in Numbers

| Indicator | Reading |

|---|---|

| Tokenized real-world assets on-chain, a record | ~$32B |

| Kalshi's regulated perpetual-futures volume in two weeks | $5.5B |

| Wholesale power on the largest US grid, PJM, in Q1 | +76% |

| Wait to connect a new US data center to the grid | 4-6 yrs |

| Rise in US residential electricity prices since 2019 | +42% |

| Data-center power demand projected by 2035, near triple 2024 | 1,300 TWh |

| Germany's 2026 defense budget, double its 2021 level | €117B |

| Brent crude, as the Iran war premium unwinds | ~$87 |

What to Watch This Week

| Date | Why it matters |

|---|---|

| This week | Whether China actually grants rare-earth export licenses to the ten newly listed US firms, or quietly slow-walks them. The list is symbolic; the licenses are the leverage. |

| Ongoing | The Strait of Hormuz reopening under the signed framework, and how fast oil retraces toward pre-war levels. Aramco warns full normalization may wait until 2027. |

| Watch | FERC's follow-through on the data-center grid rules, and whether more states copy Maine's ban or Virginia's fights over who pays. |