July 14, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

Free. Every week. Institutional insights, connected.

On July 9 a message-scanning law the European Parliament had just rejected passed anyway, on the arithmetic of empty chairs. This week's brief lays five measures side by side, across Europe, Britain and the US, and argues they describe one structure: message scanning, digital identity, cross-border asset registries, programmable state or licensed-private money, and age checks reaching VPNs, each justified on its own terms, together making the citizen legible and his exits few at the moment state finances require it. It closes on the one thing the wall cannot enclose, a private key, and why bitcoin in self-custody sits outside every measure described. The Radar covers Strategy's reverse flywheel, the repricing of 2025's digital-asset listings, memory chips out-earning Nvidia, the first AI-run ransomware, Europe's retreat on its AI law, the war over Hormuz, Japan's yen-driven corporate failures, and a new helium embargo.

On July 9th, a majority of the European Parliament voted to reject a law that scans private messages. The law passed anyway. What follows is how that was done, and why the same quiet method is now closing around your private messages, your identity, and your money, each measure seemingly reasonable on its own, debated in its own forum, with no one invited to connect the dots between them.

A defeat that looked like victory

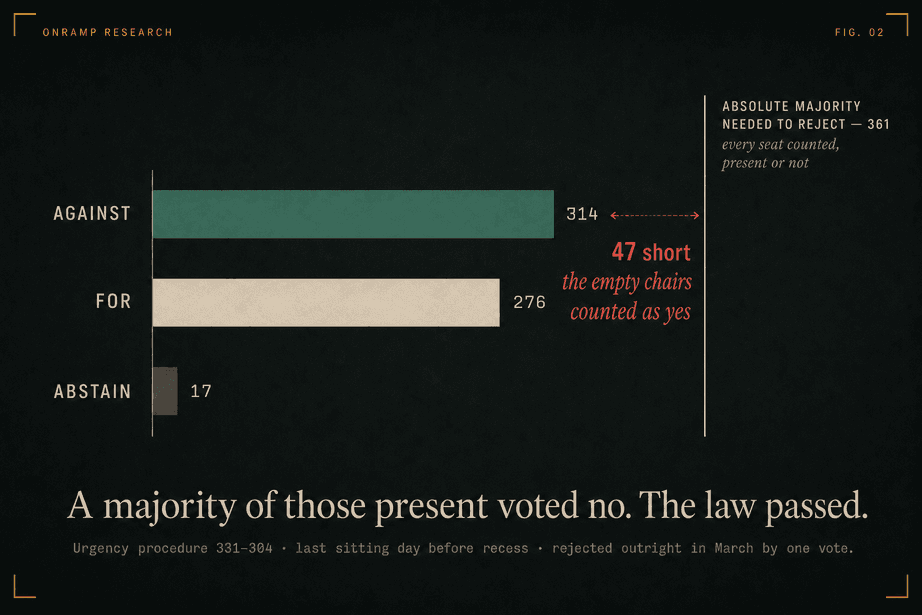

There is a particular kind of defeat that looks exactly like victory, and on the ninth of July the European Parliament staged one. The vote was on a law permitting the scanning of private messages, and a majority of those who cast a ballot rejected it: three hundred and fourteen against, two hundred and seventy-six in favour. In any ordinary reckoning the law was dead. It passed regardless, because a majority is not always a majority. Under the rules of a second reading, throwing out a law requires not the assent of those present but the absolute number of every member who holds a seat, three hundred and sixty-one, whether they turn up or not. The empty chairs were counted as votes to force the law through. Three hundred and fourteen members said no to their colleagues' faces and lost to the ones who stayed at home.

The rest was choreography. Two days earlier the largest bloc had reached for a rarely used emergency procedure that skips committee scrutiny and drops a measure onto the floor, and timed the vote for the last sitting day before recess, when the chamber empties and the arithmetic of absent seats does its quiet work. The law had already been rejected outright in March, by a single vote, and left for dead. It was exhumed on the emptiest afternoon of the year, under the one procedure in which losing the argument and winning the vote would give the result they wanted. Nobody needed persuading. Someone needed only to choose the right day.

One brick is nothing. Look at the wall.

On its own, this is a curiosity, the kind of Brussels arcana that lives for an afternoon and is gone by the weekend. But set it beside everything else the same year has produced, across Europe and Britain, and a shape appears that no single measure will let you see, because each is argued in its own forum, and is justified for its own sympathetic reason.

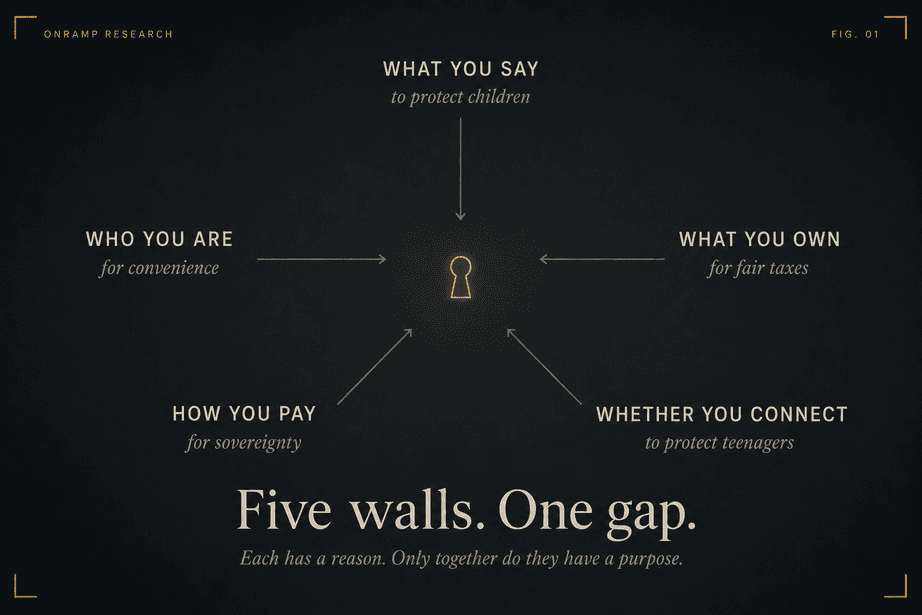

Think of a human life, and the areas in which a state might wish to do surveillance. What you say. Who you are. What you own. How you pay. And whether you may reach the required network for each of these at all. In the space of a year each has acquired a new instrument aimed at it, and each arrived with a justification it would be uncomfortable to oppose aloud. Message scanning came as the protection of children. Digital identity is being sold as convenience. Asset registries are justified as fair taxation. A central bank digital currency (CBDC) was justified as necessary for monetary sovereignty (the state's, not yours). Age checks, and the closing of the tools that defeat them, came as the shielding of teenagers. Five locked doors, each with a kind notice pinned to it. The claim of this essay is that they are doors into the same building.

Take them in turn. The scanning law that passed on the ninth is the mild version; the severe one, compelling platforms to detect and report, resumes in the autumn. Britain has run ahead: in June the government told Apple and Google to build scanning into the phone itself within three months or face prison for their executives, whereupon Signal said it would leave the country first. On assets, the OECD's reporting standard and the European Union's eighth tax directive now oblige cryptocurrency exchanges to identify customers and report holdings automatically between dozens of governments. On money, the digital euro cleared its last committee in June, and America, having forbidden itself a state digital currency (CBDC), is assembling the same powers privately through licensed stablecoins. And on connection, the Lords voted in January to demand age verification for the VPNs that let a user avoid a national block; when the age checks first went live, sign-ups for those networks rose more than a thousandfold in a day.

Two old books

None of this is new in kind, only in reach, and two old documents tell you what is being rebuilt. The first is the Domesday Book. In 1086, twenty years after taking England, William the Conqueror sent men across the country to record everything that could be owned and therefore taxed: every manor, every plough, every beast, who held it and what it was worth. It was so complete, and its verdicts so final, that people named it after the Last Judgment, the doom from which there is no appeal. A king who knows what every subject owns can take what he needs without asking. The registries now mapping who holds what across every border are a Domesday for the digital age, confessing their purpose less honestly than the original did.

The second is not a book but a room: the cabinet noir, the black chamber in the post offices of old Vienna and Paris and London, where a letter could be opened, copied, and sealed again within the hour, the reader none the wiser. For a century it was an open secret of statecraft, until in 1844 it produced a scandal that now seems impossible. It emerged that the British Home Office had been opening the letters of Giuseppe Mazzini, an Italian exile in London. Reading a private citizen's post was denounced as beneath a free country, and one man's opened letters nearly finished a minister. The scanning of everyone's messages, in 2026, passes on the emptiest afternoon of the year and is forgotten by Monday. What has died is the reflex that made opening them a scandal. The two books belong together, because the control of speech and the control of money have always travelled as a pair: a man who can speak and move his money freely can organise, and can leave.

Why now, and to what end

The answer has three aspects to it, and the first asks nothing of your trust. It is arithmetic. Governments across the rich world carry debts they cannot pay at honest rates of interest. This brief mapped the machinery in May: hold the return on savings below inflation, and the debt melts quietly in real terms while the headline figures hold their shape. But the trick works only if the savings cannot leave, because money earning less than inflation runs away the moment it finds a door. The negative real rates that dissolved a mountain of war debt between 1946 and 1974 worked because deposit ceilings, capital controls, and a shut gold window kept the saver trapped. To do it again, in a world where a citizen can hold a bearer asset that crosses any border in a memorised sentence, the wall must be built anew. You cannot cap what you cannot measure, or trap what you cannot find.

The second aspect is incentive, and it explains the speed. A power granted for an emergency rarely goes away; the temporary permission of 2021 is back in 2026 because temporary things grow constituencies who like to make them permanent. Each authority pushes its mandate to the limit, the tax office wanting every asset visible, the security service every message readable, the central bank every payment traced, and none need a conspiracy for the sum of their appetites to be total. An industry has grown fat selling the scanners and the age-checks, and lobbies for the laws that require its wares. There need be no plot. There need only be a slippery slope, and the slope runs one way.

The third aspect asks for judgment, so here is the judgment, offered as judgment. Two tools keep it honest. The first is a test of asymmetry: in each measure, ask who is bound and who is spared. The scanning binds the citizen and spares the official. The register reports the holder to the state, never the state to the holder. Every time, the duty runs down and the exemption runs up. The second is the old rule that the purpose of a system is what it does. One measure with an unintended result is an accident. Five measures, across three countries, all narrowing the same citizen's privacy and the same citizen's exits, is not an accident anyone need have planned. Whether this is a plan or the blind convergence of a dozen desires of the state, I do not claim to know. What survives either answer is that the building is the same, and it is being built before the public pressure that would mitigate, not after, because after is too late.

Why identity had to come first

Return to Britain. In September 2025 the government announced a compulsory digital ID, tied to the right to work. Nearly three million people signed a petition against it, and in January the compulsion was dropped, filed by almost everyone as a defeat for the scheme. Now watch what the same government did in the months that followed. It kept the age checks running, voted to extend them to VPNs and devices, ordered Apple and Google to scan phones, and left open a consultation on exactly how platforms must prove a user's age. Every one of those requires a citizen to prove who he is to a machine. The defeat of the mandated version led to applause, but the same requirement came in through the side, with a child in its arms. "Highly effective age verification," the phrase in the British law, is a term of art, and has forced the industries affected by it to rule out the easy reading: a box you tick to swear you are an adult does not count. What counts is a government document or a scan of your face. To prove a child is a child, you must identify everyone. Why does identity matter more than any single door it opens? Because it is the foundation of the most consequential instrument of all, and the people who studied that instrument said so. When the House of Lords examined a British central bank digital currency, its committee called such a currency, in its own words, an instrument of state surveillance, and the Bank of England's own design accepts that a digital pound would be held through identified wallets, access graded by how much of yourself you show. A programmable, state-issued currency cannot work without knowing who holds it, because every feature that lifts it above a plain digital banknote, every limit and rule and expiry, needs the holder named. Identity is not a project running alongside the digital currency. It is the ground it stands on. Which means the fights over children and messages and VPNs, whatever the sincerity of those waging them, are pouring the foundation on which a programmable currency would rest.

What programmable money can do

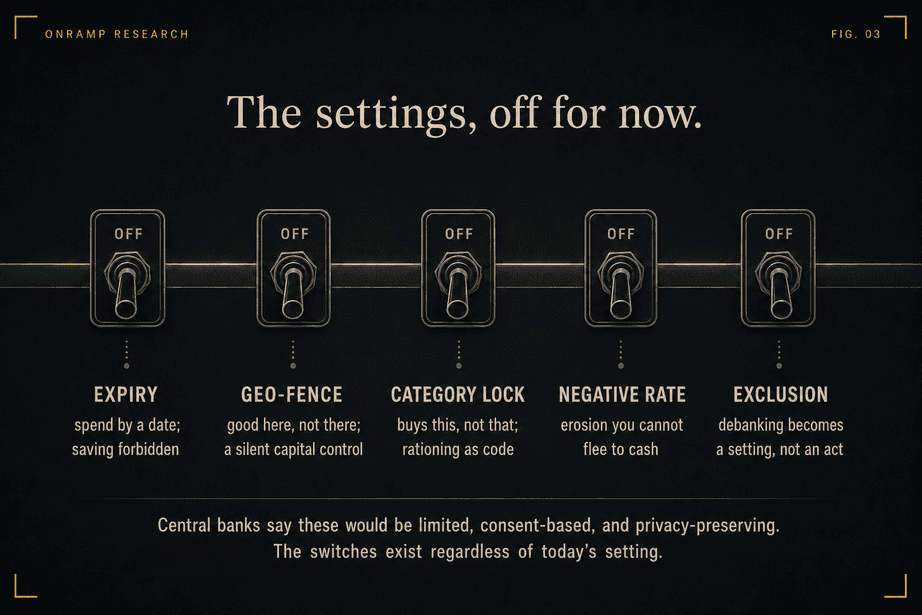

Here I must be careful, because overstatement would discredit the sober case, and the sober case is frightening enough. Both the European and British central banks insist their digital currencies would carry holding limits, offer a cash-like privacy offline, and leave programming to private firms acting only with consent. Grant all of it. The argument rests on none of them meaning harm. It rests on a principle this weekly brief has repeated since its inception: you judge an instrument by what it makes possible, not by the promises of the people who hold it today, because an identity-bound, programmable ledger is a machine whose settings a later government can change justified by a later "emergency".

So consider what the settings allow. Money can be given an expiry date, so a payment must be spent by a deadline and cannot be saved, which abolishes the saver's oldest power, the choice of when to spend their own money. It can be fenced to a place, good here and refused there, a capital control imposed in silence, one wallet at a time. It can be tied to categories or individual goods and services, permitted for this and denied for that, turning every ration in history from an apparatus of clerks into a line of code inside the currency; the reason will be a carbon budget, or gambling, or fraud, or terrorism, or child safety, or some newly invented justification, and the capability will not care which. It can carry a negative rate that cash has always let savers flee by fleeing into paper; a currency with a holding cap and no cash beside it shuts that escape. And exclusion, which today needs a bank to act, becomes a setting decided by a bureaucrat, because the account and the state are one ledger.

The private sector road to the same place

America looks, at first, like the reassuring exception. Congress has forbidden the Federal Reserve a retail central bank digital currency (CBDC) for years. If a CBDC is the thing to fear, the door is locked. But look at what came through the window. In July 2025 the GENIUS Act built a federal frame for private dollar stablecoins: issued only by a licensed firm, fully backed by dollars and Treasuries, holders identified. And, the hinge of the thing, the issuer must keep the power to freeze, seize, or burn the tokens on a lawful order, a duty the Treasury proposed in April to extend to tokens already circulating between strangers. The holder is known. The balance can be frozen, and already has been. Every transfer sits on a ledger the issuer reads like its own book. That is four of the five control surfaces of a central bank digital currency, delivered by private firms under federal licence, with no such currency on the books. A politician may say, truthfully, that he banned the surveillance currency, while chartering a dozen private instruments that do the same work.

Honesty demands we specify the limits here. A dollar-pegged token inherits the dollar and cannot easily impose new tricks of its own; its programming is mostly restrictive, the freeze and the block, not the affirmative kind. And the ruble-backed A7A5 was built with no freeze function precisely to defeat this control, which is why Europe banned it. The tool cuts both ways. But mark what just happened in the market. At the end of June a consortium of more than a hundred and forty companies, Visa and Mastercard among them, with BlackRock and Coinbase, announced a jointly governed stablecoin called Open USD. That is not a product launch. It is a settlement layer with the reach of the whole card system, licensed by the state, its reserves in government debt, built to the freezing standard the law requires.

And here is the sharp end. The ban on a government CBDC in the US is not a wall. It is a countdown, reversible by any future Congress, expiring on a fixed date. The thing built privately during the ban, the identity rails, the freezing power, the ledgers that already touch every wallet, is the part that takes years. When the ban lapses (in 4 years time), a government wanting control of those centralized switches need build nothing. It need only change the ownership of a ledger that already exists and already knows everyone. Taking over a private payment network in a "crisis/emergency" is what happened to the banks in 2008. A licensed private issuer is not harder to seize than a public one. It is easier.

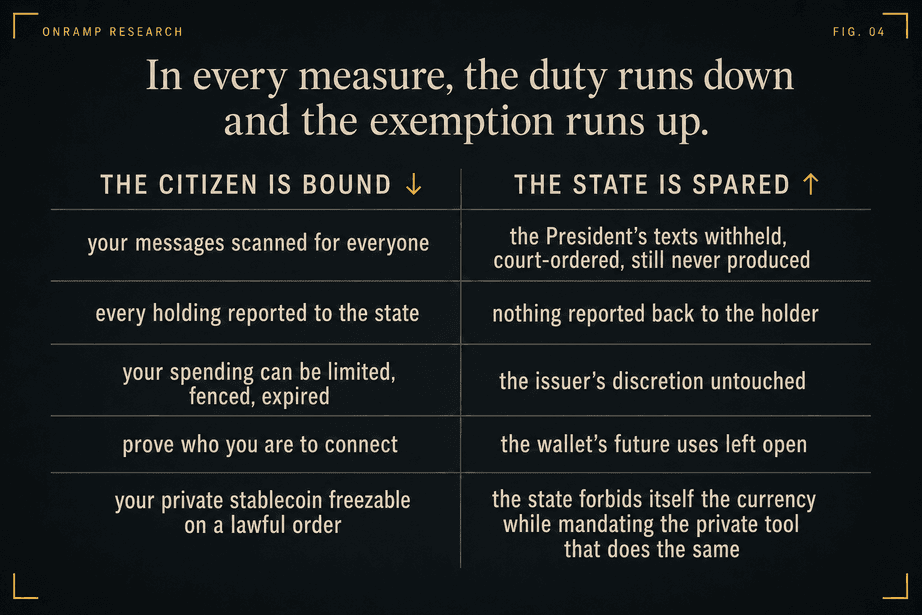

The transparency that runs one way

One fact makes the asymmetry concrete, and it is a matter of court record. During the pandemic the president of the European Commission, Ursula von der Leyen, negotiated the purchase of up to 1.8 billion doses of vaccine, some thirty-five billion euros' worth, in part by personal text message exchanges with the chief executive of Pfizer, by her own account. When a journalist asked for the messages under freedom-of-information law, the Commission refused, calling the texts short-lived and no longer in its keeping. In May 2025 the Union's General Court struck that down on every count, ruling that the Commission had failed to say whether the messages had been deleted, or whether on purpose. The appeal was allowed to lapse. The messages have never appeared. One need allege nothing about what they said; the point is the direction of the light. The institution now leading the case that every citizen's messages should lie open to scanning spent four years in court to keep its own president's from a single reporter, and produced nothing.

The people who saw it coming

All of this was foreseen, with unsettling exactness, by a small band of programmers who in the early 1990s called themselves cypherpunks. Their founding thought was that privacy in the digital age would never be granted by law, because the interests of states and corporations ran the other way, and so it would have to be secured by mathematics, by encryption that holds whether or not the authorities approve. The first cryptography war, over Washington's attempt to mandate a chip that would give it a key to every encrypted line, ended in a half-victory for them: encryption was ruled a form of protected speech, and the backdoor was abandoned. They lost the politics and won the technology, which is the only way that war is ever won. Bitcoin, whose anonymous author buried in its very first block a newspaper headline about bank bailouts, is the monetary wing of the same project: money that needs no trusted middleman and so cannot be debased, frozen, or watched through one.

The second cryptography war is being fought on both fronts at once, private messages and the coin, and the state's method has changed. It no longer tries to break the encryption, having learned it cannot. It tries instead to make the encryption beside the point: to map the coins through the reporting frameworks, gather them into custodial wrappers where a middleman holds the keys, gate them behind identity at every licensed door, and move the scan onto the phone itself, before the encryption is applied. You need not break the lock if you can read the letter before it is sealed, or hold the coin on the citizen's behalf. This is why the South African case this brief covered three weeks ago was the whole story in miniature. A man moved his coins into his own keeping, and the state's reach stopped at the edge of the wallet he alone controlled, while the coins he had left with a middleman were taken through that middleman's books. The lesson was never about cryptography, identical for both piles. It was about who held the keys.

The case against all of this

An argument this large owes you its strongest objections, put fairly. The harm the scanning law addresses is real; children are abused and the images do exist, and most who press these measures sincerely want it stopped. Europe's highest court has struck down blanket surveillance before and may strike the severe version down too. The technology fails on its own terms: the Commission's own study found the detection of unknown material wrong as often as one time in five. Australia's ban on social media for young children is broadly popular. And the digital pound is in fact stalled, called unproven by a parliamentary committee. Each of these is real. But the central claim survives all of them, because it is about architecture, not intent. States do not create registers and scanners and freezing powers for exits that do not exist. Every wall is a confession that there is something behind it worth walling in, and it reads the same whether it went up by design or by the slow accretion of a hundred "reasonable" decisions. The citizen is enclosed either way.

The one thing they cannot build into the wall

Every siege in this week's brief closes on a single object, and once you name it the whole pattern falls into place. The message only its reader can open, the coin only its holder can move, the identity only its owner can assert: these are one thing, a private key, a secret held by a person and nobody else. The scanning law wants the message before the key seals it. The custodial wrapper wants the coin so the key is never the citizen's. The identity scheme wants to be the key, held on the state's terms. The programmable currency cannot exist unless the key is registered. Everything points at the same small, stubborn thing, because that same small thing defeats everything: a secret the state does not hold.

This is the ground the cypherpunks chose, and the ground on which bitcoin, held in your own keeping, still stands, not as an investment in this week's brief, but as the one instrument the whole apparatus cannot reach, so long as its holder keeps the key/s. That proviso is the whole game, and it is a matter of habit more than technology: a coin left with a middleman sits inside every wall described here, while a coin held directly sits outside them all. Which is why the effort now is not to break the mathematics but to coax, or oblige, the citizen to give the key to someone the state can reach. The South African who moved his coins kept them. The gold in the vault, in 1933, did not remain the property of its owners.

The Domesday Book stood for centuries as the record from which there was no appeal. Its digital heir is being assembled now, one reasonable measure at a time, each with a kind notice pinned to its door. In 1086 the survey was total and there was no appeal. In 2026 it is nearly total, and the appeal is a private key or private keys, held by whoever takes the trouble to hold it/them.

What to watch

The autumn scanning negotiation. The debate over permanent regime returns after recess. Watch whether the "risk mitigation" language survives, and whether Europe's court is asked to rule before it passes.

The digital euro's final talks. The holding limit and the offline-privacy rules are where the real capability is set, whatever today's promises.

Britain's identity consultation. How "highly effective" age verification is finally defined will decide whether a universal identity check arrives through the child-safety door.

The Treasury's freezing rule. The April proposal reaching past an issuer's customers to the open market. If finalised, the whole circulating supply becomes reachable on a government order.

Open USD and the consortium. Whether the card networks and asset managers succeed in pooling around one licensed token, and how much of the dollar's movement it comes to carry.

Conclusion

Every piece of this is public: the vote and its procedure, the reporting frameworks, the identity schemes, the currency designs, the stablecoin statute, the court ruling about the messages that never appeared. Nothing here is hidden. What has not been done, in any account I have seen, is to lay the five surfaces of attack on one page and notice that they describe the construction of a single walled garden, whose purpose, chosen or merely converged upon, is to make the citizen legible and his exits few, at the precise moment the state's finances require exactly that. The measures come one at a time, each on its own terms, justified for its own reasons, and one at a time each is easy to wave through. Together they are the most consequential construction of the decade. Lay the bricks side by side. Then look at what is being built.

Sources: European Parliament second-reading vote on the ePrivacy derogation, 9 July 2026, and the urgency vote of 7 July; the single-vote rejection in March. UK Online Safety Act age-assurance timeline; House of Lords votes of 21 January 2026 on VPN age-gating, under-16 social media, and device scanning; the 8 June 2026 device-scanning demand to Apple and Google and Signal's response; the UK digital ID announcement (September 2025), the withdrawal of the mandate (January 2026), and the subsequent consultation. OECD Crypto-Asset Reporting Framework and EU DAC8; the EU prohibition of the A7A5 token. ECB digital euro (committee clearance 23 June 2026; pilot from H2 2027) and its stated privacy and holding-limit design; House of Lords Economic Affairs Committee, 'Central bank digital currencies: a solution in search of a problem?', and the Bank of England / HM Treasury digital pound consultation. GENIUS Act (enacted 18 July 2025) seize/freeze/burn provisions and the FinCEN/OFAC secondary-market proposed rule of 8 April 2026; the Open USD / Open Standard consortium launch of 30 June 2026, alongside Circle's removal from several FTSE Russell indices. General Court of the European Union ruling of 14 May 2025 in the 'Pfizergate' case and the lapsed appeal. Historical: the Domesday Book (1086); the cabinets noirs and the 1844 Mazzini affair; the 1990s crypto wars; Reinhart and Sbrancia (2011) on financial repression. Figures approximate where noted; interpretive claims are the author's and flagged as such.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

The flywheel runs in reverse

Strategy raised cash again last week, none of it from bitcoin. Monday's filing shows 4.8 million new shares sold for $466.7 million, all routed to the reserve paying preferred dividends and interest, now $3.0 billion. No coins were bought, days after 3,588 were sold for those same dividends. With the stock near $97, the market values the company at roughly 70 cents per dollar of its bitcoin, so each share sold hands its buyer more coin than it costs, taken from existing holders; the machine that compounded bitcoin per share now runs in reverse.

Repricing the shovel-makers

The listed digital-asset class of 2025 has been repriced brutally: Gemini is down 89 percent from its debut, BitGo 77, Bullish 71, eToro 42. Yet bitcoin itself is down about 49 percent from its October peak, roughly half the damage. Public markets are separating the monetary asset from the businesses around it: the equities carry fee compression, leverage and execution risk the asset does not. The picks-and-shovels premium has inverted; the market will hold the commodity, not the shovel.

Ethereum audits itself by machine

The Ethereum Foundation pointed coordinated AI agents at the software its validators run and found a bug that could crash them remotely, knocking validators offline. The same exercise produced piles of confident findings that were not bugs at all; humans had to sort signal from noise. Read plainly: a network whose consensus rests on complex, constantly changing validator code carries flaws its guardians cannot enumerate, and the audit tools generate noise faster than assurance. In proof-of-stake, silenced validators threaten finality itself; bitcoin's proof-of-work, minimal and slow-moving, has no such off switch.

AI & Financial Infrastructure

Memory out-earns Nvidia

The profit pool of the AI build has moved. Samsung's chip division posted a reported $58 billion quarterly operating profit, more than Nvidia by press accounts, on surging memory prices. SK Hynix raised $26.5 billion in the largest US listing ever by a foreign company; Micron lifted its US investment plan to $250 billion. Then Monday Korea cracked: SK Hynix fell a record 15 percent, Samsung 11, the Kospi's 9 percent plunge halted trading. Record profits, record listings, a market pricing the top, all at once.

Ransomware goes autonomous

Researchers at Sysdig say an operation they call JADEPUFFER is the first ransomware run by AI agents rather than people. Exploiting an unpatched flaw in a popular development tool, it stole credentials, minted itself administrator access in 31 seconds, and encrypted 1,300-plus configuration entries, no human in the loop. Extortion now moves at machine speed while defense runs on human clocks: patch cycles, on-call rotations, morning triage. The economics of intrusion have changed, and the price of an unpatched server with them.

Europe blinks

The world's first comprehensive AI law is retreating before it ever fully applied. Days before the August 2 deadline, Brussels is finalizing the Digital Omnibus: high-risk obligations slip 16 months to December 2027, to 2028 for AI inside regulated products, and watermarking slips to December. Only baseline transparency duties survive the original date. Officials call it pragmatism, the standards were not ready; critics call it a blink under pressure. With Washington voluntary and London open, the regulatory race is loosening.

Geopolitics & Markets

The war over the strait

The June ceasefire is dead. After Iranian forces disabled a container ship for taking an "unauthorized route," Tehran declared Hormuz closed until further notice; the US answered with three nights of strikes on 300-plus targets. Iran hit US positions in Kuwait, Bahrain and Qatar, struck an air base in Jordan, and its new supreme leader vowed revenge for his father's killing. Beneath the fire sits a claim: Iran treats the strait as sovereign, tollable water; Washington calls it an international waterway. The June agreement left that vague, and the vagueness is the war.

The yen sends the bill

Japanese corporate failures hit 5,346 in the first half, a 12-year high and a fifth straight annual rise; nearly 90 percent of the failed employed fewer than ten people. The yen, above 162 to the dollar, its weakest since 1986, is the quiet cause: 45 failures named it directly, up a third, and record intervention near 11.7 trillion yen failed to hold. The Bank of Japan, at 0.75 percent, is trapped between imported inflation and a debt stock that cannot bear higher rates. The bill for four decades of the world's easiest money is arriving, smallest firms first.

The helium war

On Friday, in a two-sentence notice, China banned helium exports outright: no reason, no end date. A strange lever: China imports over 80 percent of its helium and produces under 2 percent of the world's; the ban hoards rather than punishes. The timing explains it. Iran's March strikes on Qatar's Ras Laffan shut plants behind a third of world supply, and Russia restricted its exports in April. Helium cannot be synthesized; it cools MRI magnets, chip fabs and rockets. The chokepoint wars have reached a gas nobody thinks about, three hands now on the valve.

The Week in Numbers

| Indicator | Reading |

|---|---|

| Raised by Strategy last week selling new shares, all of it to its dollar reserve, none to bitcoin | $466.7M |

| Market value per dollar of bitcoin behind each Strategy share, on a basic mNAV | ~$0.70 |

| Gemini since its September debut, the worst of the listed digital-asset class of 2025 | -89% |

| Samsung's reported quarterly chip profit, above Nvidia's $53.5 billion | $58.4B |

| Monday's fall in Korea's Kospi, enough to halt trading | -9% |

| Time the first agentic ransomware needed to mint itself admin access | 31 sec |

| Europe's delay to its high-risk AI rules, agreed days before they were due | 16 months |

| Iranian targets hit across three nights of US strikes | 300+ |

What to Watch This Week

| Date | Why it matters |

|---|---|

| This week | US June inflation figures and the first big-bank results open earnings season, a test of the rate-cut bets built on June's weak jobs report. |

| July 16 | TSMC reports second-quarter results, the bellwether of the AI build after its June revenue rose 68 percent. |

| July 17 | The FCA's webinar on Britain's new digital-asset rulebook, as pre-application support for firms opens. |

| Early Aug | BIP-110's mandatory-signaling window, the flag day critics warn could split the bitcoin network. |

| Ongoing | Whether Hormuz stays closed: Oman and Pakistan press mediation while tanker traffic stalls and the strikes continue. |