October 10, 2024 Roundup: Bond Reversal & BTC Dominance

Mark Connors | Managing Director, Head of Global Macro Strategy

Free. Every week. One story that matters, read all the way down.

All the King's Horses

Last Friday’s decline in unemployment and growth in jobs dashed the Fed’s recent commitment to lower rates. The result is a hamstrung Fed that may not be able to piece together a fracturing financial system being battered by the rising tide of debt.

Last Friday’s favorable employment print accelerated a reversal in treasury bonds that started in mid September, leaving the UST10Y up +30 bps since that low of 3.62% to 4.06% with knock-on effects including:

- Re-inverting the U.S. Treasury yield curve as measured by the 2Y yield (4.00%) less the 10Y yield (4.06%).

- Reversing half of the 60 bps rally in the UST10Y that commenced after Chair Powell’s dovish Jackson Hole speech in late July.

Today’s CPI release is unlikely to offer any respite for bondholders. The expected 2.3% print would be lower than last month’s 2.5%, but we think irrelevant as it does NOT include the 5.0% rise in oil this month. Additionally, we point to the sticky shelter component that posted a 5.2% gain last month as MORE important than the headline 2.3% expectation.

U.S. Treasury volatility jumped to the highest level since January 3rd of this year. As the graph below illustrates, U.S. Treasury Volatility as measured by the MOVE index has remained elevated ever since the Fed started hiking rates in Q1 2022.

source: Onramp & TradingView

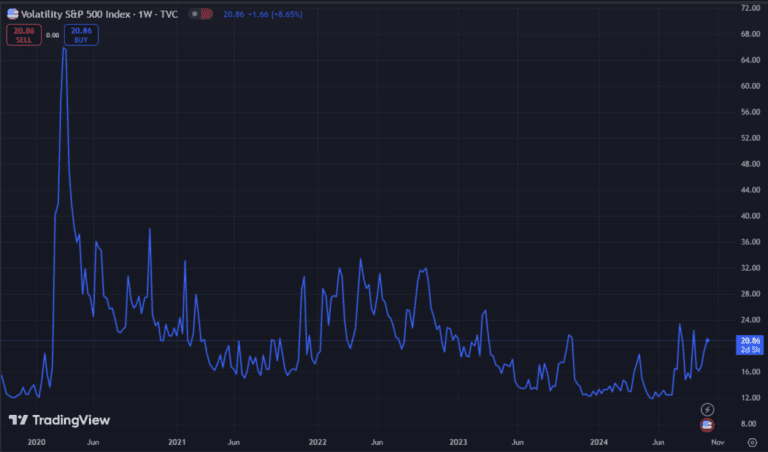

Conversely, U.S. equity volatility has been relatively subdued, but clearly on the rise again.

source: Onramp & TradingView

The distinctly elevated U.S. Treasury volatility is a signal to markets that NOT all is well with the growing pile of treasuries we discuss in greater detail below.

Unfortunately the only remedy appears to ‘print’ more debt, which may very well result in higher Treasury volatility.

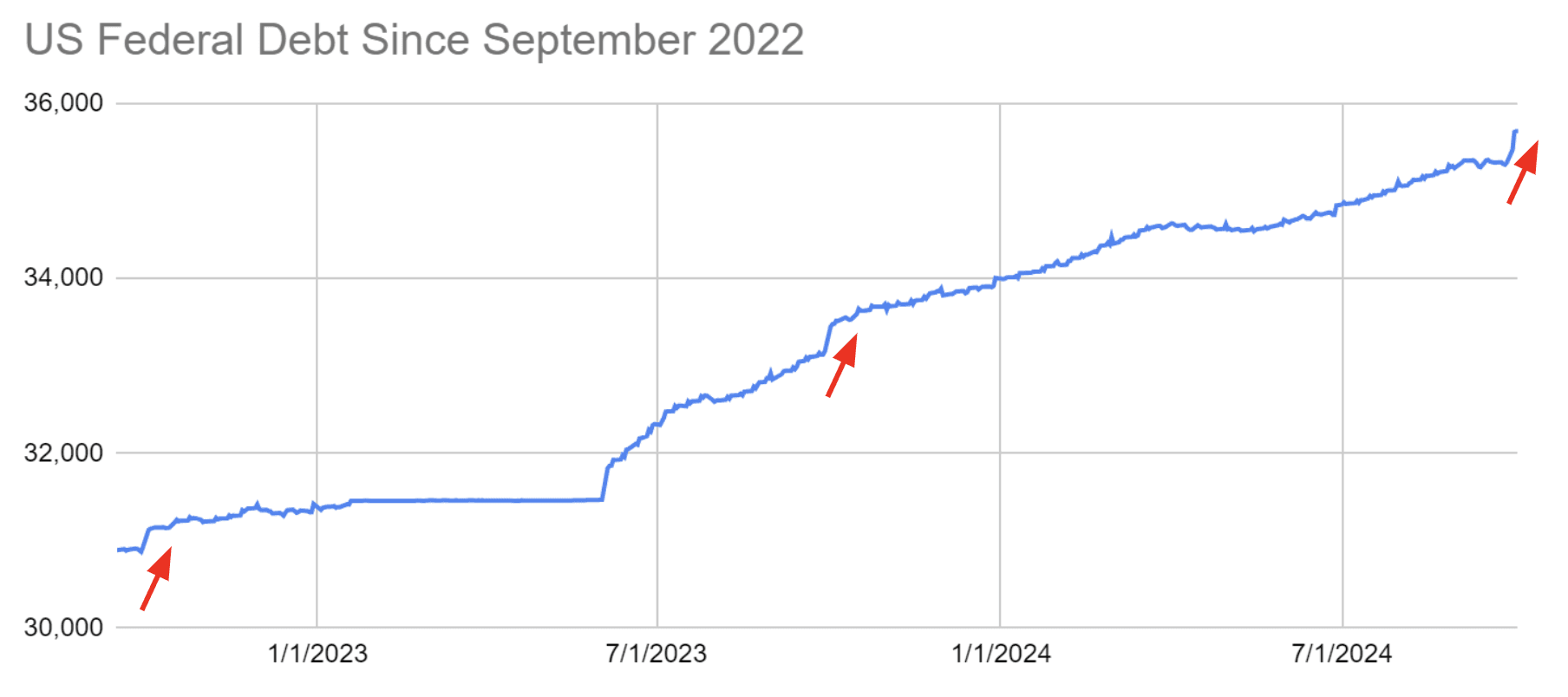

Two patterns in the above chart illustrate a growing reliance on debt that is negatively impacting Treasury markets.

First, the debt ceiling impasse from January 19th, 2023 to June 2nd temporarily stalled the rise in debt, remedied only after a congressional vote to ‘raise’ the debt ceiling. Much has been written about the role that the aggressive Fed hiking campaign had on the March 2023 bank failure as the heavy slug of U.S. treasuries that banks hold fell faster than liabilities.

Less discussed is the overlap of the bank failures and the 2023 debt ceiling standoff. Remember that Janet Yellen was searching for all manner of cash to pay government obligations, even suspending payments to Federal Employee retirement systems…so cash was dear, was Yellen’s message. The subsequent rapid rise in debt showed the government wasted no time in playing catch up.

Second, at the start of every fiscal year in October, the U.S. Federal debt jumps as we see highlighted by the three arrows representing the start of FYs 2022, 2023 and 2024, which was last week.

The sustained commitment to grow debt (+7.2% YoY) more than GDP (+5.2% YoY) based on data through Q2 2024 is negatively impacting markets, as we see in Tuesday’s outsized spike in Treasury volatility noted above. The result is a growing deficit that will exceed 7% (or over $2 trillion on an annualized basis) in short course.

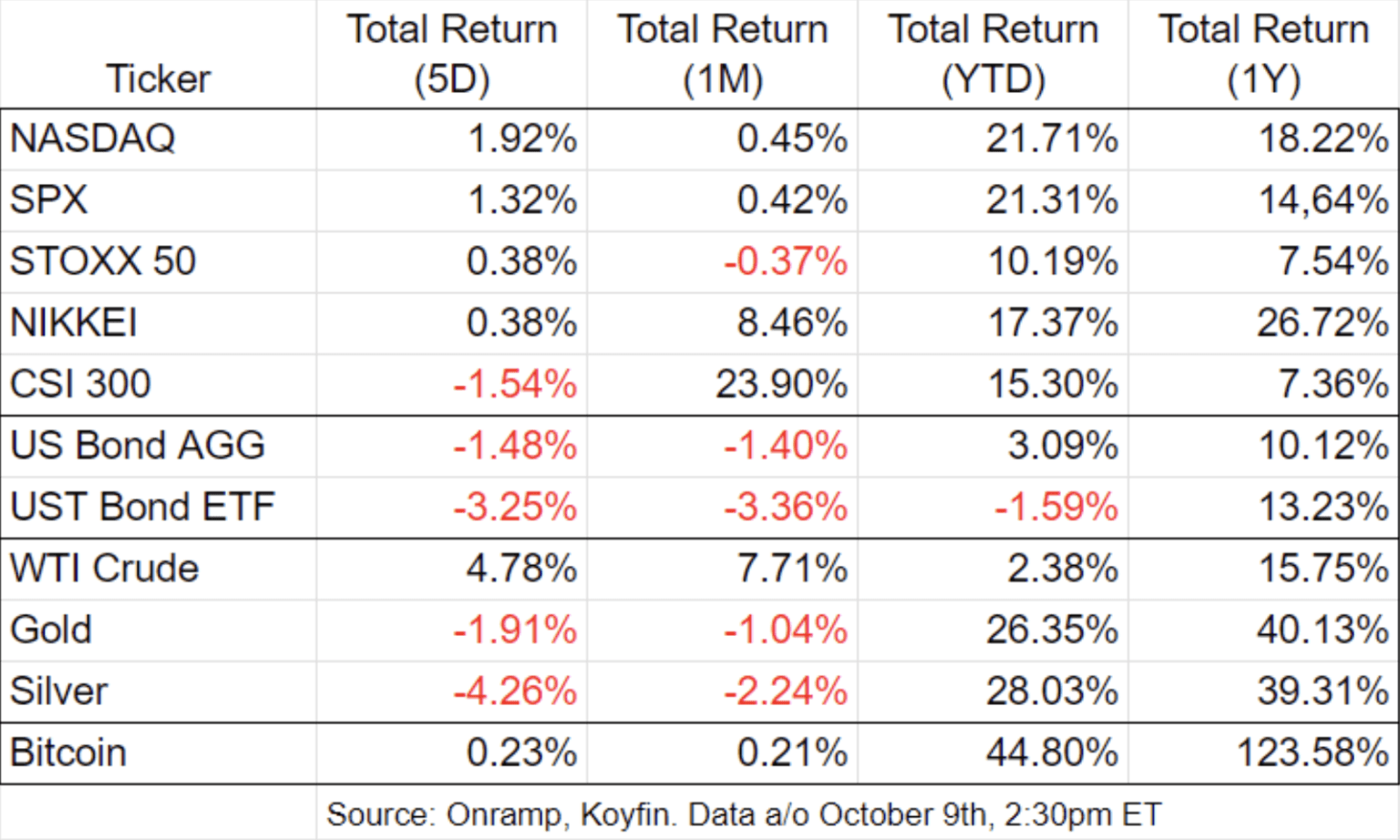

Market Scorecard

The knock-on effects of the U.S. growing pile of debt shared above is NOT all negative.

One beneficiary has been bitcoin (BTC), which enjoys a codified cap on supply protected by the most secure and decentralized computer network in the world. These qualities likely contribute to BTC being the only asset to post positive returns across all four time frames detailed below, with the highest YTD and trailing 1-year returns of 44.8% and 123.6%, respectively.

Geopolitical and central bank actions played a big part in recent prices moves, including:

- Oil rising +4.8% on the week, +7.7% over the past month on escalation in the Middle East

- Bonds falling as the Fed is unlikely to delivery on its promise to cut rates

- The CSI 300 holding onto its +23.9% 1-month gain after an epic series of dovish actions to support banks

Network Effects

Bitcoin’s integrity may be the driving force behind its growing dominance across the digital asset ecosystem.

As the below graph from the Onramp Terminal illustrates, both bitcoin’s price and its dominance over the entire $2.2 trillion digital asset ecosystem have risen since the December 2022 lows.

For a network effect to take hold, it has to survive, compound its benefits over time, and no protocol has done that better or longer than the bitcoin network, something the market is slowly appreciating as measured by BTC’s growing dominance.

A Failed Network

On Monday, U.S. Bankruptcy court Judge John Dorsey approved the FTX bankruptcy plan which will return “100% of bankruptcy claim amounts” according to John J. Ray III, CEO and Chief Restructuring Officer of FTX. Mr. Ray first came on the FTX scene as the Judge who signed the November 11th, 2022 bankruptcy filing, commenting on the lack of credible record keeping and control at FTX.

But in less than two years the courts are ready to distribute between $14.7 and $16.5 billion dollars, with Monday’s approval being, in the words of Mr. Ray, a “significant milestone” for creditors.

We see the resolution of the FTX estate as a significant milestone for another reason and a potential catalyst for BNY Mellon being granted a waiver from the SAB custody restriction.

In John J. Ray III’s own words, “Today’s achievement is only possible because of the experience and tireless work of the team of professionals supporting this case, who have recovered billions of dollars by rebuilding FTX’s books from the ground up and from there marshaling assets from around the globe. It also reflects the strong collaboration we have had with governments and agencies from around the world that share our goal of mitigating the wrongdoings of the FTX insiders. Looking ahead, we are poised to return 100% of bankruptcy claim amounts plus interest for non-governmental creditors through what will be the largest and most complex bankruptcy estate asset distribution in history.”

The courts and the U.S. government learned a great deal about the inner workings of a digital asset exchange and are now able to make distributions to creditors across more than 200 jurisdictions.

This decision comes from a Judge with over 30 years of bankruptcy and restructuring experience that includes Enron. One claim for issuing SAB 121 in March 2022 was that there was NOT enough bankruptcy precedent. In addition to FTX, there are others, but we believe FTX is the lynchpin for legal precedence given its complexity and the successful resolution across regions.

One note to current bitcoin holders: the payout to creditors is 100% of their claim in USD at the time of the filing, November 11th, 2022, when BTC was trading around $16,000. A reminder that custody remains an integral component to your bitcoin investment.

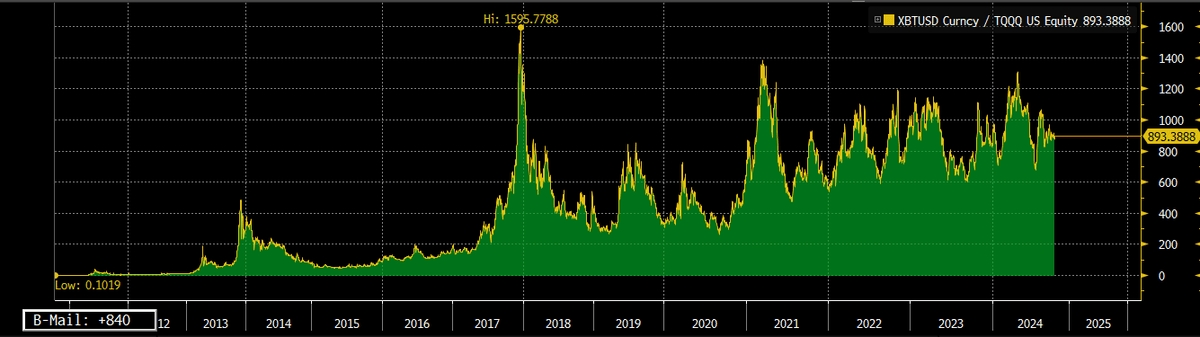

Chart of the Week

“Chart of bitcoin since inception denominated in $TQQQ (3x levered QQQ). Higher means bitcoin outperforming TQQQ, lower means bitcoin underperforming TQQQ. Up and to the right for most of the past 15 years, albeit with some vital volatility.”

— Bill Miller IV on X

Quote of the Week

“Every generation has its story asset — the thing that you never sell and it just keeps going up. For my grandparents, it was $GE. For my parents, it was $AMZN. For me, it’s BTC. #bitcoin”

Podcasts of the Week

The Last Trade E068: The Millennial Monetary Migration with Bram Kanstein

In this episode of The Last Trade, Bram Kanstein, host of the Bitcoin for Millennials podcast, joins to discuss paths down the rabbit hole, mechanics of bitcoin adoption, the life raft for millennials, societal implications of bitcoin, perils of the fiat system, & more.

Final Settlement E014: Flash & the Future of Payment Gateways with Pierre Corbin

In this episode of Final Settlement, Pierre Corbin, co-founder & CEO of Flash, joins the pod to discuss nostr’s potential for payments, Flash overview & roadmap, bitcoin’s layers & interoperability, catalyzing payment adoption, payment gateway monetization, & more.

Wake Up Call (10.7.24): Kevin Jiang, CIO of Virgo Digital Asset Management

In this episode of Wake Up Call, hosts Rich Kerr & Mark Connors are joined by Kevin Jiang, CIO at Virgo Digital Asset Management, to discuss the evolving institutional landscape, impacts of BTC ETFs, purchasing power, options market dynamics, & more.

Closing Note

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Find this valuable? Forward it to someone in your personal or professional network.

Until next week,

Mark Connors & Brian Cubellis