October 3, 2024 Roundup: Money Printers Warming Up

Mark Connors | Managing Director, Head of Global Macro Strategy

Free. Every week. One story that matters, read all the way down.

Remember the Titans

It’s the fourth quarter and gains are harder to come by, inviting bold schemes by coaches and rancor among the players.

Last week we saw Team China cut their risk fast as Q3 drew to a close, effectively punting on 1st down with the biggest liquidity pump since 2008. The surprise move was meant to distance themselves from the type of loss that engulfed the Japanese equity market earlier in the quarter.

And the fans loved it.

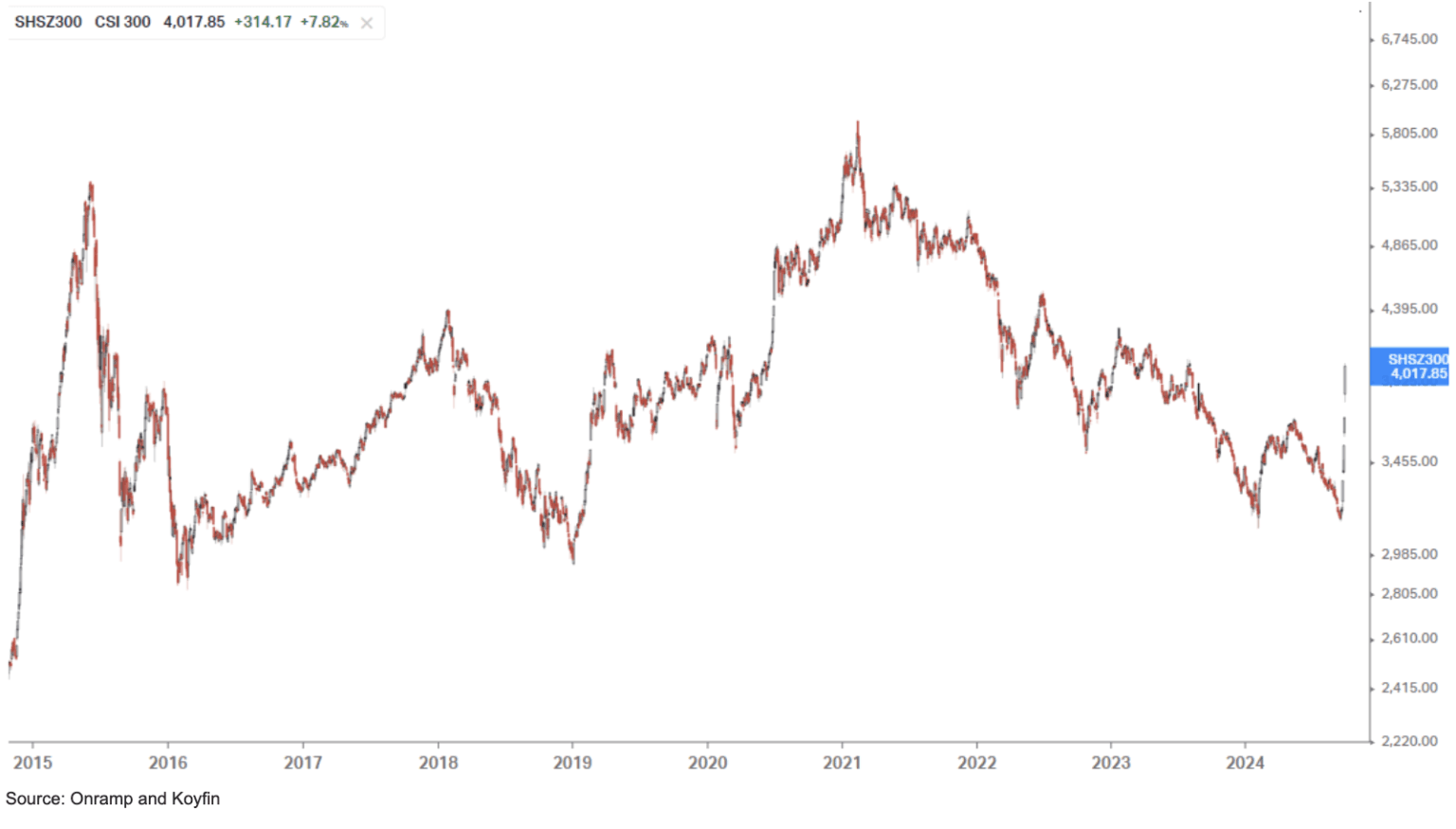

As our scorecard shows, Chinese equity investors lifted the CSI 300 to an 18% gain in just 5 days, pulling YTD gains into positive territory, now up 17.1%. So in 5 days, the CSI 300 went from virtually flat to up 17%…too easy, maybe.

China saw what happened when the Bank of Japan (BoJ) played by the old rules, with a hawkish miscue earlier in Q3 that drove equities lower, the largest downward move since 1987. But China’s pop in equities may be just another sugar high, if the past is prologue.

As the below graph shows, China’s CSI 300 has chopped sideways for the better part of a decade, punctuated by sharp spikes that eventually give way. The largest spike was 2015, when the government injected liquidity to boost the moribund equity market.

It didn’t last then, nor when the government injected liquidity in the wake of the covid shutdown. Playing for the easy win with easy money can be short sighted, as we shared in September 12th’s Roundup.

The widening gap between wages, which are pegged to CPI and rent, was evident in the last U.S. release showing increases for shelter (+5.2%) in the U.S. were 2x the core inflation print of 2.5%.

The decades-long decline in purchasing power may have been a contributing factor to this week’s strike by dockworkers. Recent concerns of replacement from breakthroughs in AI and robotics have been cited, but we see the long running erosion of buying power from a living wage as core to the growing number of strikes globally.

Attitude Reflects Leadership

If China, Japan, the U.S. and other governments continue to take the easy route of money printing, expect more rancor by the asset-light wage earner.

There is little doubt that technological innovation is core to breaking this destructive cycle and it’s not lost on industry participants, and even some politicians.

From Europe, to Ohio, some politicians recognize that innovative industries are crucial to sound governance and economic sustainability. Last month, former Prime Minister of Italy and President of the European Central Bank, Mario Draghi, penned several hundred pages as to why Europe is facing an existential crisis and why innovation is the way out.

Closer to home, Ohio Senator Niraj Antani proposed a bill to require the state of Ohio and all its subdivisions to accept cryptocurrencies, including bitcoin. Antani gave a shout out to former Ohio State Treasurer, Josh Mandel, who spearheaded a similar effort in 2018 that was passed, but reversed a year later due to unclear regulations.

In the U.S., traditional market incumbents are pressing ahead. The approval of listed options on BlackRock’s BTC ETF (IBIT) may be more impactful than the anticipation and launch of spot BTC ETFs this past January in the U.S.

First, the notional value of derivative instruments are multiples more than their underlying spot or funded instruments.

Second, the bitcoin ETF options will provide institutions with a key tool to manage the asset’s volatility, potentially increasing the pace of adoption. Listed options also often require less margin than OTC options and tend to be more liquid. One caveat we note is the mismatch of option market hours to the 24/7/365 nature of the underlying spot asset, bitcoin.

This is relevant as the vast majority of the S&P 500’s gains over the past decade have been ‘on open’, meaning the price change occurs when the market is closed. Bitcoin’s volatility is ~65%, ~4-to-5x that of the S&P 500. We mention this as call overwriting is a Wall Street staple, employed by institutions and high net worth individuals for decades. But with bitcoin options on your IBIT, caveat emptor.

Bitcoin’s positive skew paired with that liquidity mismatch could make for some very unhappy call sellers that miss out on the type of large, sustained moves bitcoin has posted. We deem the introduction of listed IBIT options as a positive. Knees will be skinned, but it is clear that Wall Street is slowly appreciating the novel technology of the decentralized, scarce, digital asset that is bitcoin.

Bitcoin and the Election

With just 33 days left until the U.S. Presidential election, we share our prediction:

More printing.

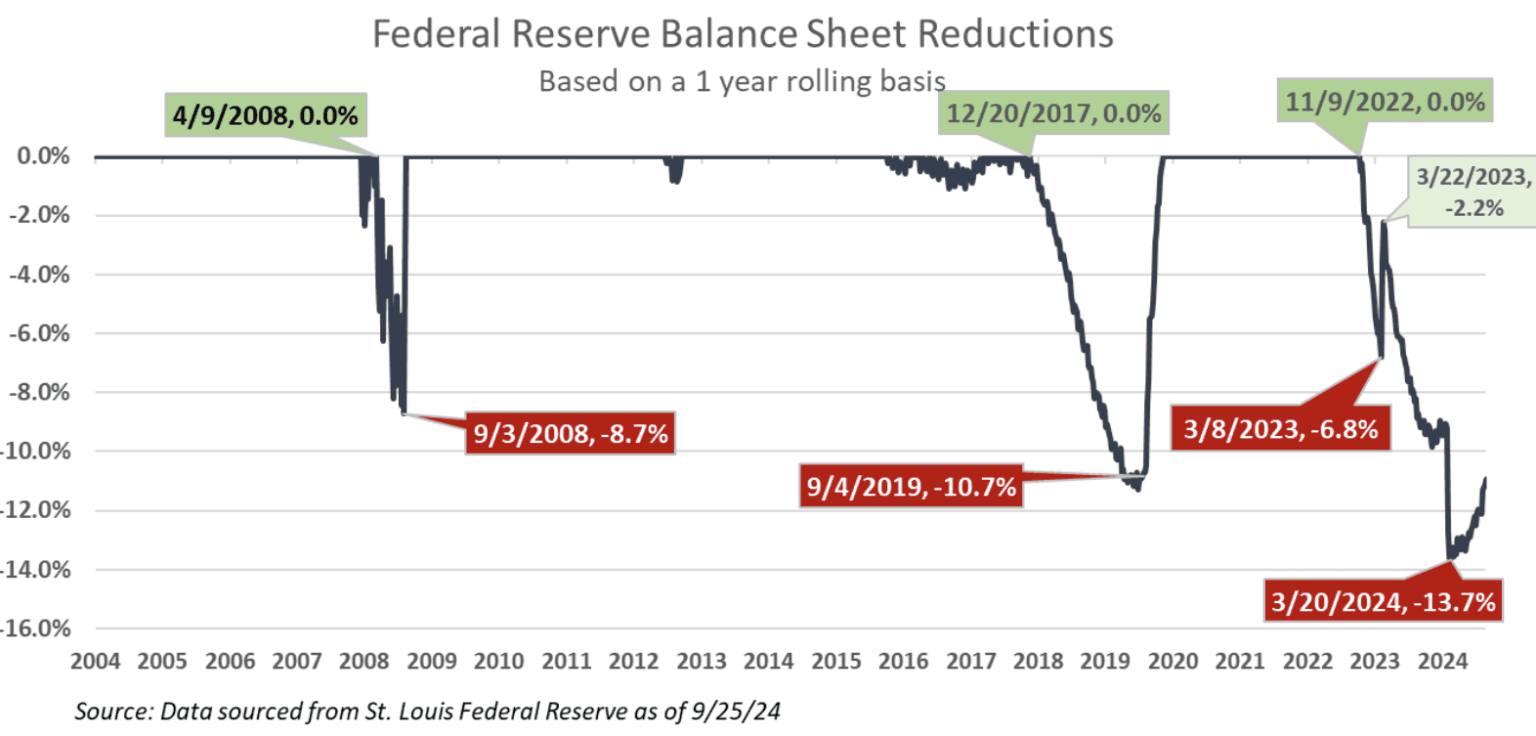

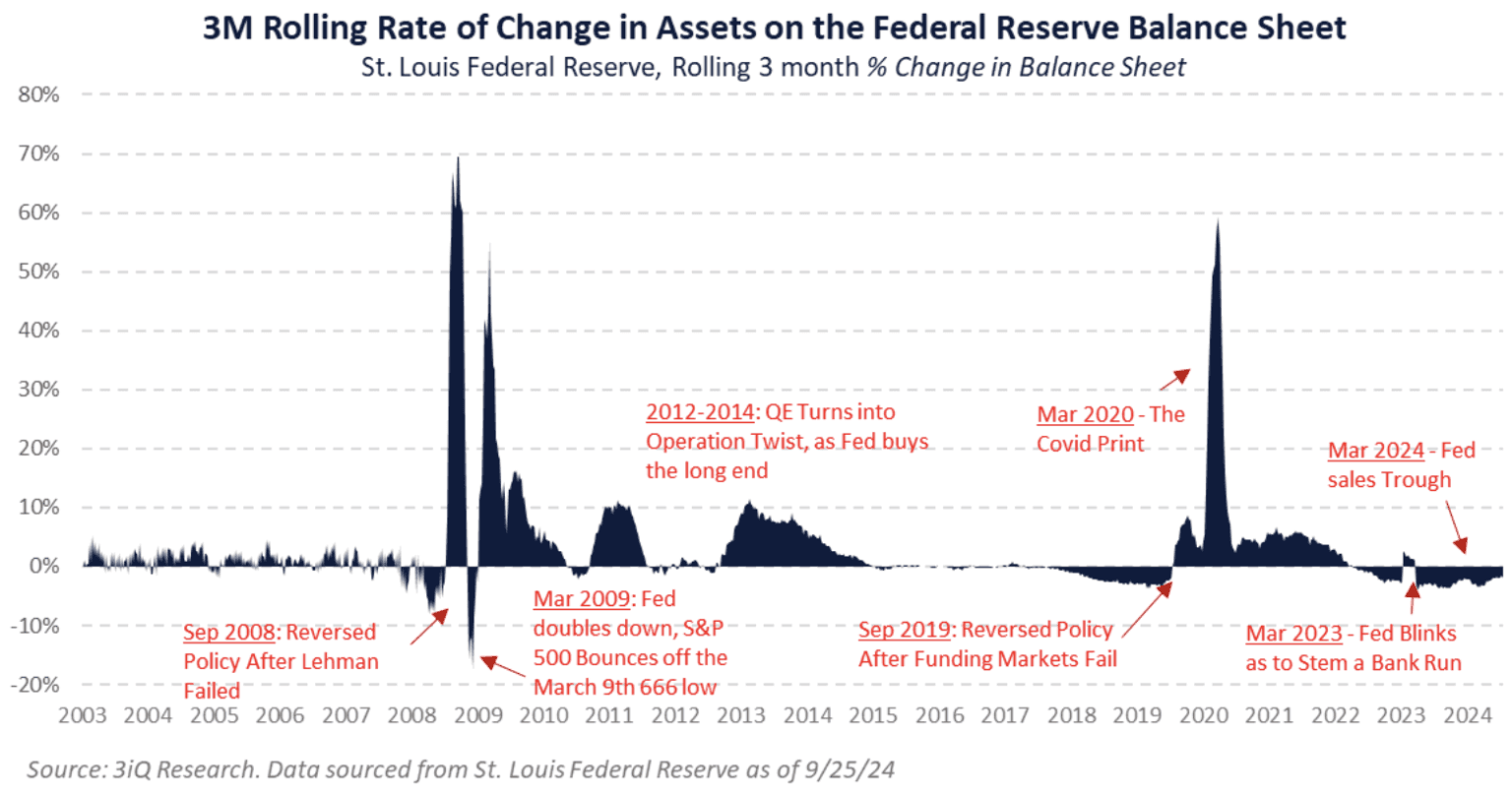

Both candidates are likely to continue deficit spending, supported by an accommodative Federal Reserve. Below we see that the Federal Reserve has decreased their sale of securities sharply. In the past, such moves were forced by a market event, but not this time. Back filled by Treasury liquidity, M2 has already reversed its largest 1 year decline since the great depression, now up year over year. Since renewed liquidity often prompts risk-on rallies, we suggest paying attention to global M2, a.k.a. liquidity.

As we shared last week, bitcoin also reacts favorably to liquidity, in fact, more so than any asset in Sam Callahan’s recent study commissioned by Lyn Alden.

Within days of Trump’s election on November 8th 2016, the UST 10Y Treasury spiked, rising from 1.88 to a peak of 3.22% two years later on well placed concerns of twin deficits.

Biden’s record after taking office in 2021 was no better, with fair arguments it was worse, and some giving his administration a pass because of covid.

Looking forward, the recent adoption of the liquidity playbook by China and Japan shows that easy money has caught on faster than the west coast spread offense.

Good for entertainment, bad plan for an economy.

Bitcoin remains the logical exit valve, as the purest form of outside money, immune to continued debasement.

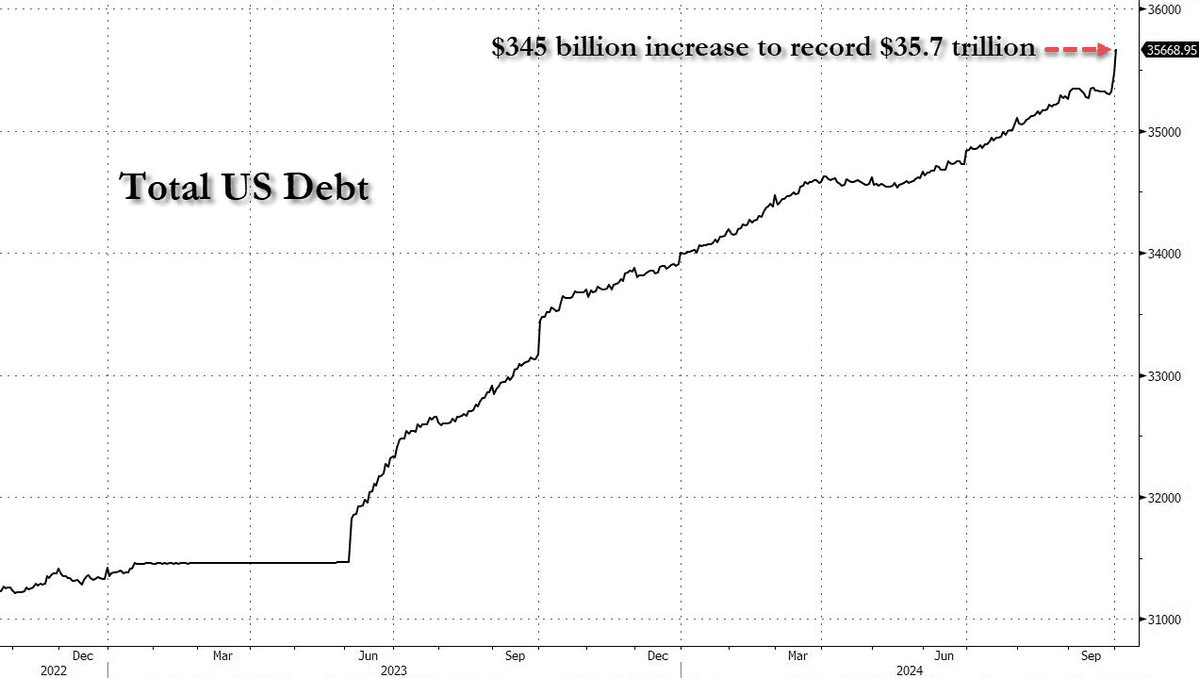

Chart of the Week

Total US debt explodes to $35.7 trillion on Oct 1, up $345 billion from Sept 27.

source: zerohedge on X

Quote of the Week

“A lot of people, and I don’t want to name names, but Solana, are taking good ideas and they’re just going…well what if we just centralized everything? It’ll be faster, it’ll be more efficient, it’ll be cheaper. And yeah, sure, it is, you’re right…but nobody’s using it, but for like memecoins and scams, because if anybody puts anything significant on it and then all the states begin moving towards it, it’s going to be a system that has levers that people can simply just take from you. You have to be thinking for the adversarial case, as opposed to the convenient case.”

— Edward Snowden, Token 2024 in Singapore

Podcasts of the Week

The Last Trade E067: The Dire Debasement Dilemma with Gary Brode

In this episode of The Last Trade, Gary Brode, founder of Deep Knowledge Investing, joins to discuss disinflation vs. deflation, government spending, gold’s resurgence, economic realities, Choke Point 2.0, & more.

Scarce Assets E019: Tomer Strolight – Bitcoin is Alien Technology

In this episode of Scarce Assets, hosts Andy Edstrom & Jesse Myers are joined by

author Tomer Strolight to discuss bitcoin’s life-like qualities, bitcoin as alien technology, bitcoin as an anti-fragile disruptor, educational progress & adoption, & more.

Wake Up Call (9.30.24): Ralph Gebran, Managing Partner of Onramp MENA

In this episode of Wake Up Call, hosts Rich Kerr & Mark Connors are joined by Ralph Gebran, Managing Partner of Onramp MENA, to discuss bitcoin’s role as a unique diversifier, BlackRock’s recent report on the topic, & commonly overlooked custodial considerations.

Closing Note

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Find this valuable? Forward it to someone in your personal or professional network.

Until next week,

Mark Connors & Brian Cubellis