May 21, 2026 Roundup: The Bond Vigilantes Return

Brian Cubellis | Chief Strategy Officer

Free. Every week. One story that matters, read all the way down.

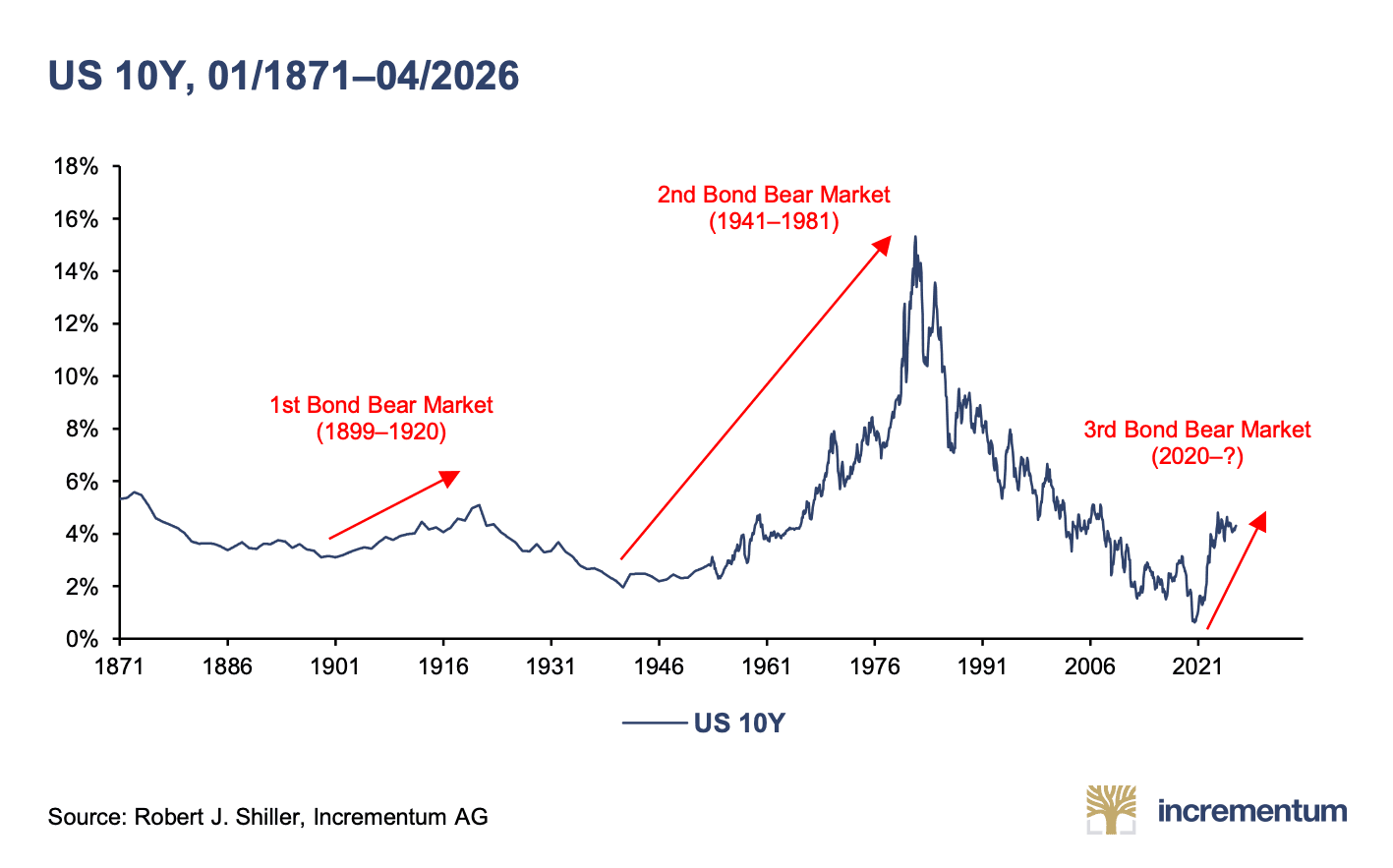

The thirty-year Treasury hit 5.2 percent on Tuesday, the highest level since 2007, before easing to 5.12 percent at Wednesday's close. The ten-year touched 4.69 percent intraday Tuesday, a sixteen-month high, and settled at 4.58 percent after Trump signaled "final stages" of Iran negotiations and oil sold off. Market-implied odds of a Fed hike by December now sit near fifty percent, a complete reversal from the multi-cut path priced in January. Bond vigilantes are back.

Below we unpack what the long end is actually telling us, why the CBO arithmetic has finally caught up with the market, why gold ran while bitcoin still sits below its all-time high, and what Iran's launch of 'Hormuz Safe' this week says about bitcoin's fundamental properties. Followed by our standard Chart, Quote, and Podcasts of the Week.

The Bond Vigilantes Return

The bond market spent April and the first half of May doing something it has not done in a generation. It started pricing fiscal reality.

The ten-year Treasury touched 4.69 percent on Tuesday, a sixteen-month high, before settling at 4.58 percent Wednesday after Trump signaled "final stages" of Iran negotiations and oil sold off. The thirty-year hit 5.2 percent intraday Tuesday, the highest level since 2007, and closed Wednesday at 5.12 percent.

Yields like that do not belong to an economy enjoying disinflation under a patient central bank. They belong to a market that has stopped believing the Fed has a free hand and started demanding a premium to fund a government that cannot stop borrowing.

Futures now price roughly a fifty percent probability of a Fed hike by December, a complete reversal from the multi-cut path priced in January. It's easy to blame the Strait of Hormuz, where the standoff with Iran has kept oil bid and pushed April consumer inflation to a three-year high. Energy shocks come and go, though. The arithmetic underneath them does not.

The Arithmetic Nobody Wants to Read

The Congressional Budget Office published its updated baseline in February.

The federal deficit will run $1.9 trillion this fiscal year, 5.8 percent of GDP. That follows $1.8 trillion deficits in each of the prior two fiscal years. That's the steady-state operating cost of the modern American state.

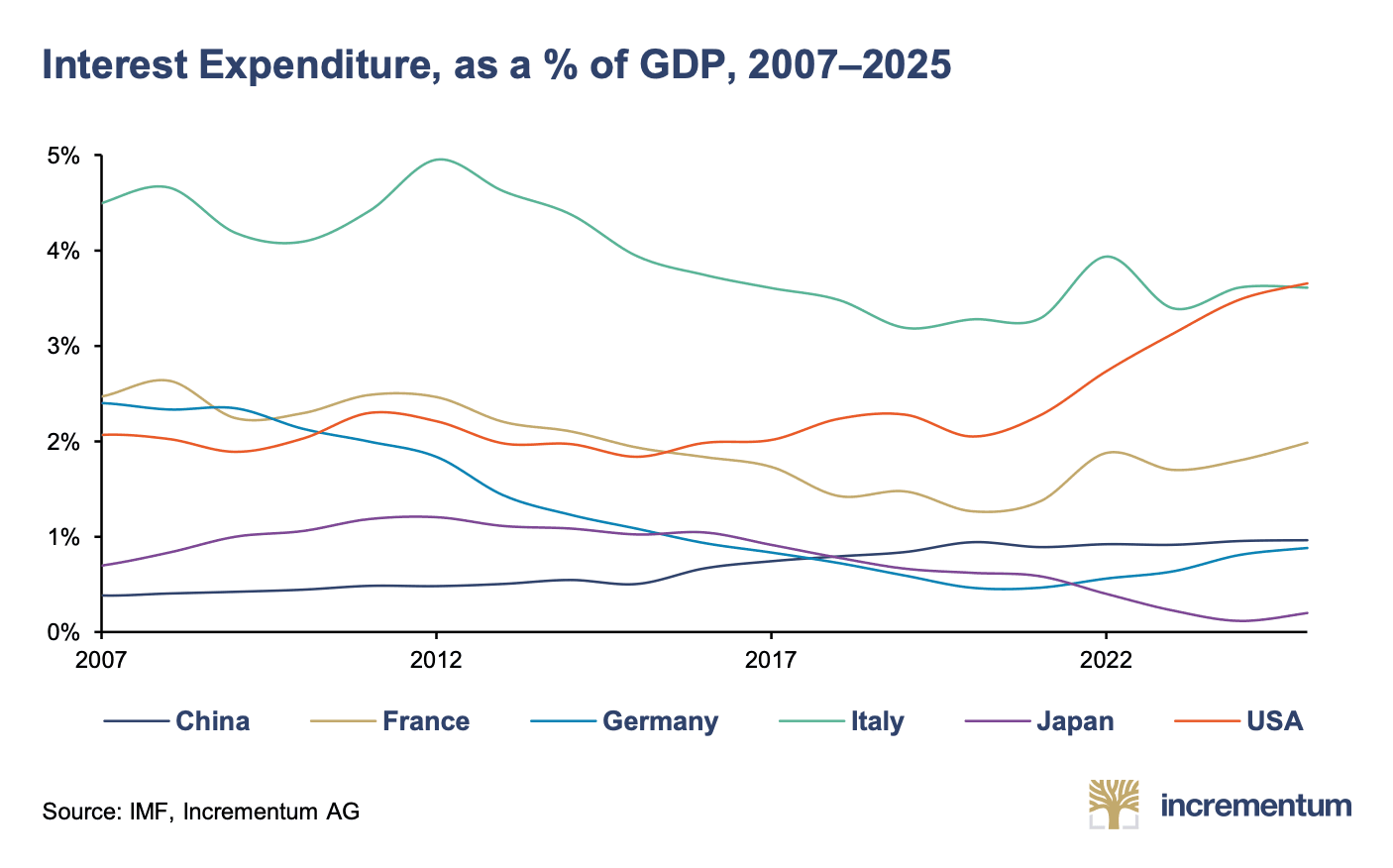

Net interest expense crosses $1.0 trillion this year and reaches $2.1 trillion by 2036 under current law. Interest is now the second-largest line item in the federal budget, ahead of defense, ahead of Medicare, behind only Social Security. Through the first six months of fiscal 2026, interest costs ran 6.1 percent above the prior year and keep climbing as the Treasury rolls lower-coupon paper into the current rate environment.

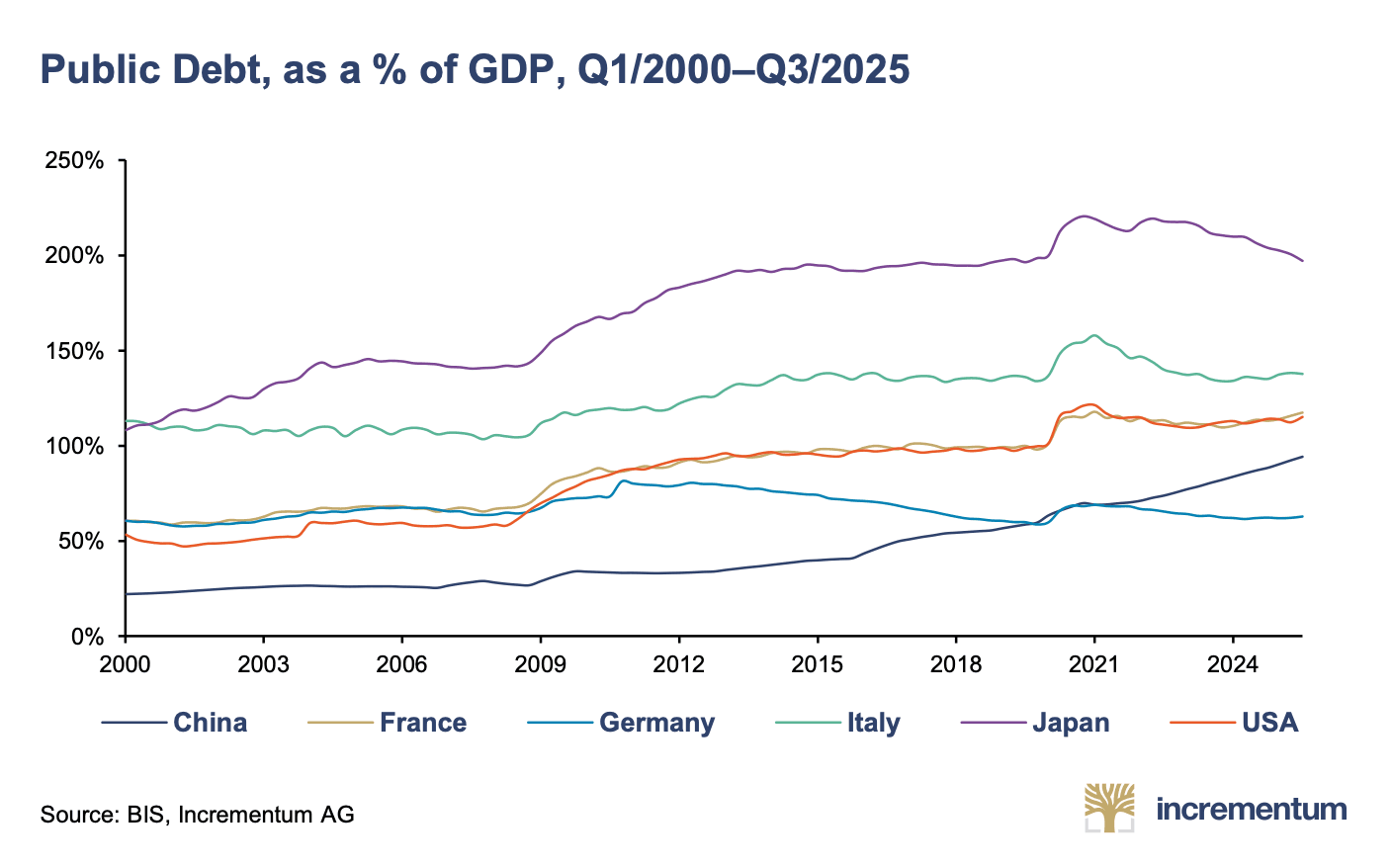

Debt held by the public sits at 101 percent of GDP and tracks toward 120 percent by 2036, eclipsing the World War II peak. CBO now expects the average interest rate paid on federal debt to exceed the rate of nominal economic growth by fiscal year 2031. This reads like a textbook debt spiral. Interest costs push deficits higher, which pushes debt higher, which pushes interest costs higher. The mechanism requires neither malice nor incompetence. Only time.

This is the backdrop against which the long end is repricing. Moody's stripped the United States of its final triple-A rating a year ago and the market shrugged. The market is shrugging less now.

The Hard Asset Rotation Is Already Underway

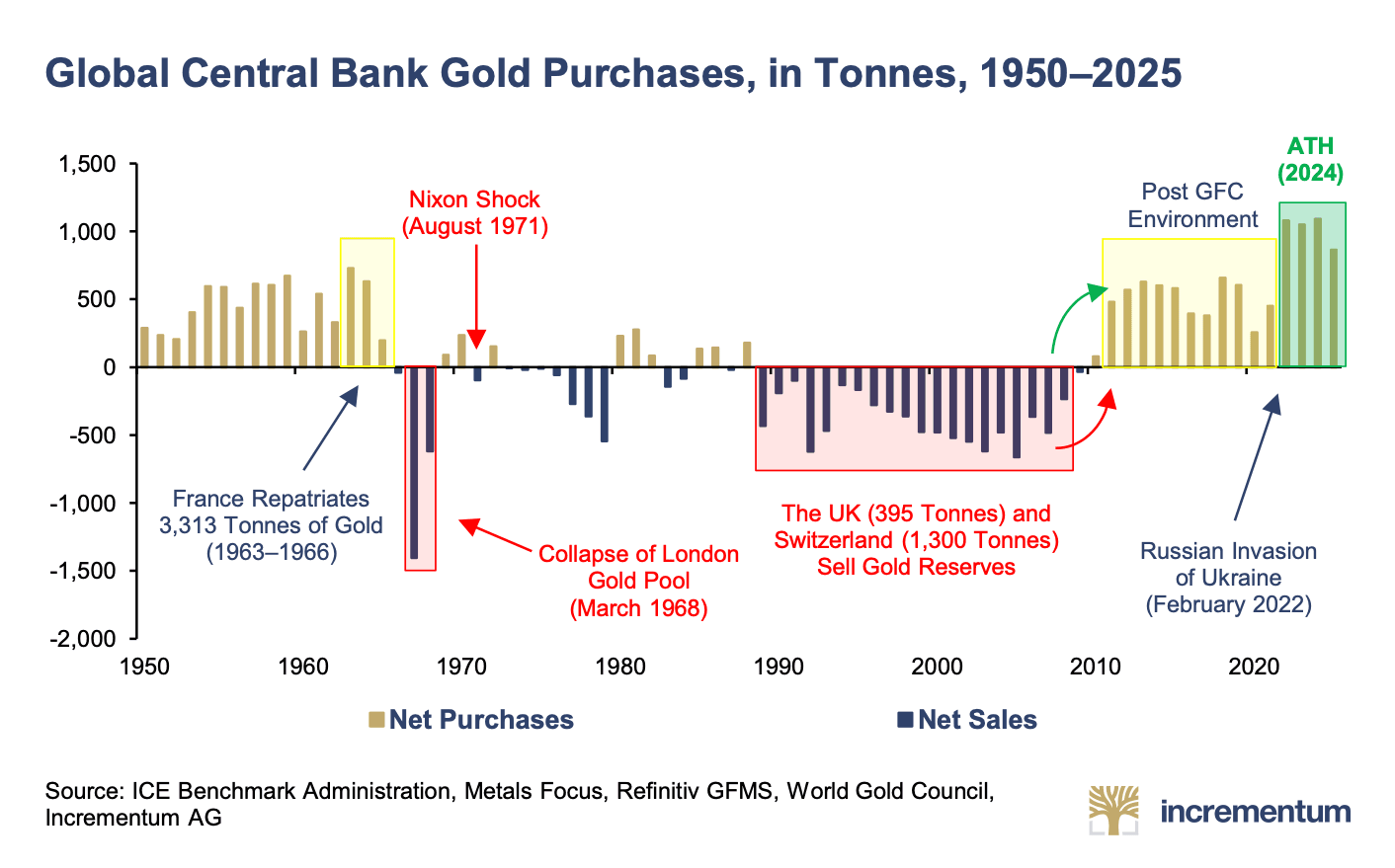

Gold printed an all-time high of $5,595 per ounce on January 28, pulled back to roughly $4,705 by early May, and remains up sixty-five percent over the trailing year. Central banks have been the marginal buyer, accumulating at the fastest pace since the Bretton Woods unwind. The price action is sovereign, not retail.

Silver has tracked gold with the leverage characteristic of a smaller market. Industrial metals have firmed. Energy has obviously bid. Even agricultural commodities have moved. Across the hard-asset complex the signal is consistent. Capital that used to sit comfortably in the long end of the Treasury curve is looking for somewhere else to live.

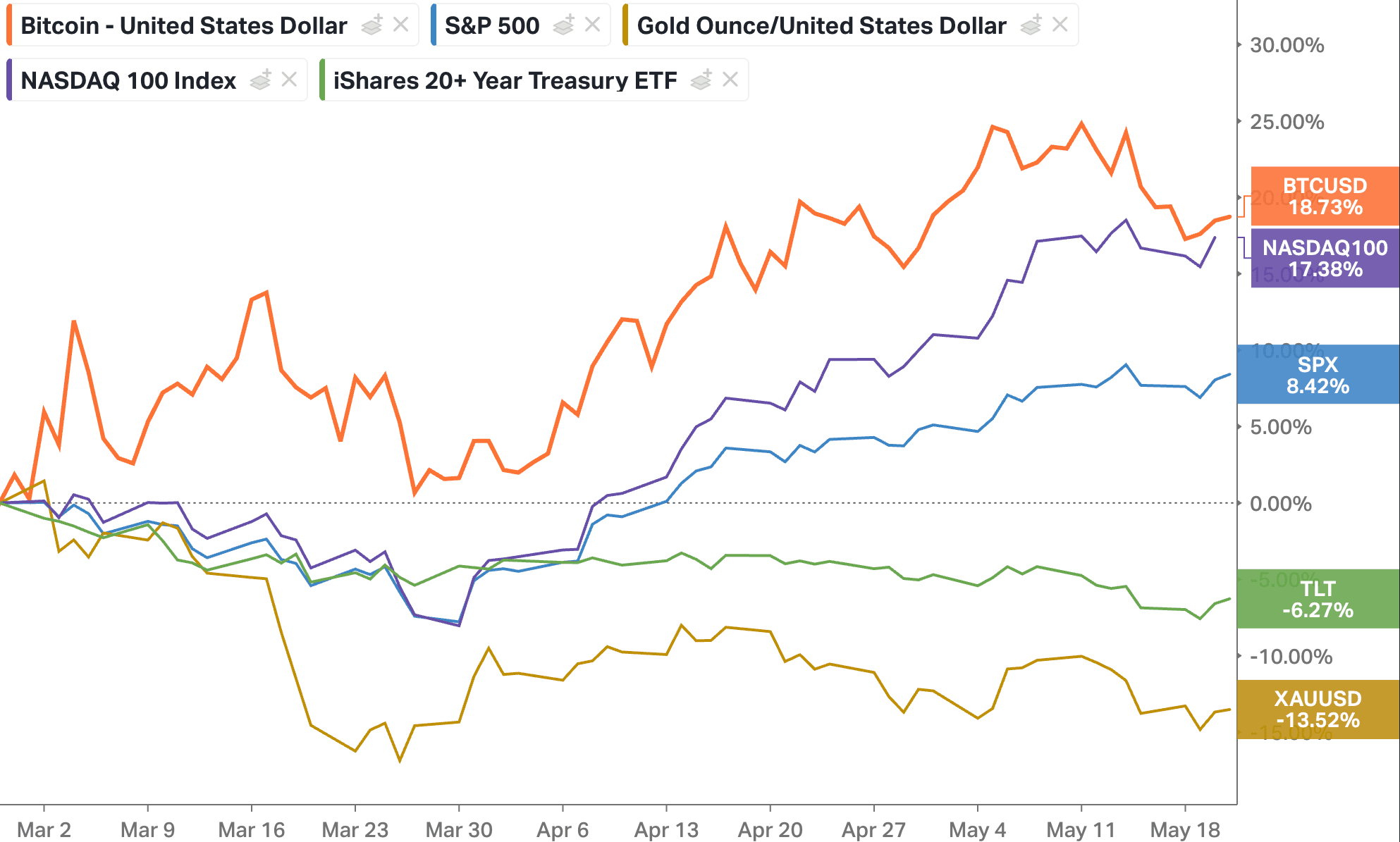

Bitcoin's price tape requires a more careful read. After crossing $126,000 last October, the asset spent the first quarter of 2026 trading like a high-beta risk asset rather than a defensive one. January was down ten percent. February down nearly fifteen. When the United States and Israel launched Operation Epic Fury against Iran on February 28, Bitcoin gapped lower with the rest of the risk complex and printed a local low near $60,000 in the days that followed.

From those late-February lows the asset has worked its way back to the high seventies, recovering more than thirty percent off the bottom while the war has escalated rather than de-escalated. The recovery has been jagged. Every hawkish headline out of Washington or Tehran has produced a selloff. The floor has risen with each cycle, though. Sixty-four thousand became sixty-eight. Sixty-eight became seventy-two.

The asset that supposedly trades like a risk asset has, over the active phase of a regional war, outperformed gold, the S&P 500, and Asian equities measured from the day the bombs started falling. JPMorgan's data desk has documented outflows of roughly 2.7 percent of AUM from GLD over that window and inflows of 1.5 percent of AUM into IBIT.

Some of this is mechanical. Seller exhaustion is a real feature of markets, and forty percent off the all-time high in an asset with Bitcoin's structural demand profile flushes weak hands and leaves a cleaner book of holders behind. Mechanical exhaustion does not explain the relative performance against gold and equities, though. Something else is going on, and it deserves to be named clearly.

What Bitcoin Has Actually Demonstrated

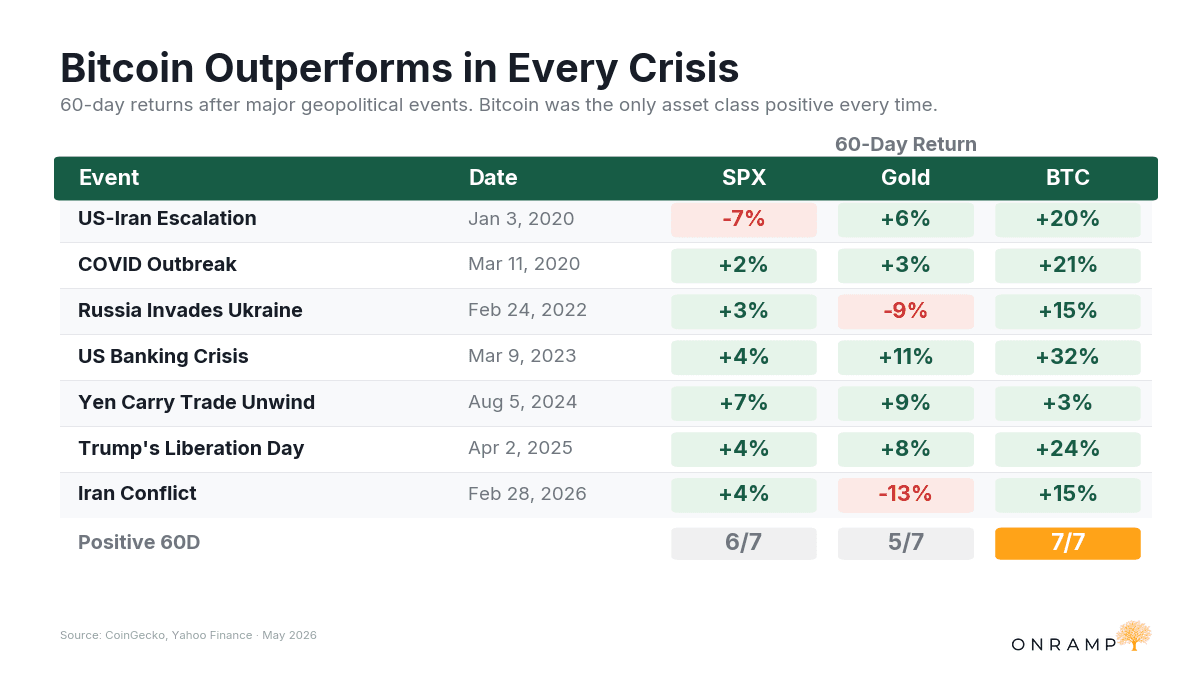

Step back from the price tape and look at what Bitcoin has done across every monetary stress event since 2020. COVID liquidity crisis. The inflation shock of 2021 and 2022. The regional banking failures of 2023. The current Iran conflict and the broader fiscal repricing underway right now. The pattern repeats with enough consistency to be called a pattern. Sharp drawdown in the acute phase, alongside everything else that gets sold when correlations run to one, followed by a recovery that takes the asset to new highs over the next twelve to twenty-four months.

That track record reflects the properties of the asset. Bitcoin is the most censorship-resistant monetary instrument in history. Its payment network operates without the permission of any intermediary. Its supply schedule is fixed in a way that no other monetary asset has ever been or can ever be. These are testable claims, and seventeen years of adversarial pressure have tested them.

Nation-state pressure on the mining network. Exchange failures from Mt. Gox through FTX. Regulatory crackdowns in China, India, and across the Western banking system. The largest correlated risk-asset drawdown in a decade. The protocol came through each of them without an unscheduled inflation event, without a successful double-spend, without a halt to block production, and without losing the properties that define it.

This week delivered the most consequential validation of those properties to date. On May 16 Iran's Ministry of Economy and Financial Affairs launched Hormuz Safe, a state-backed maritime insurance platform that settles policies in Bitcoin for vessels transiting the Persian Gulf and the Strait of Hormuz. The ministry projects more than $10 billion in annual revenue if the platform captures meaningful share. Reports through April had floated the concept. This week it became a published ministry document, and a Bloomberg story carried into every institutional terminal in the world.

The reflex among Western commentators was to wave the announcement off as sanctions evasion. That reading misses what actually happened. A sovereign state under maximum financial pressure, locked out of the dollar system, evaluated its options for monetizing one of the most strategic maritime chokepoints on Earth and chose Bitcoin over gold, yuan, euros, and every other available rail. Whether Hormuz Safe ever achieves operational scale matters less than the fact that a sovereign actor has now built a billion-dollar revenue mechanism on top of the protocol and pointed it at the global energy trade.

Bitcoin was designed to be money for enemies. That sounds provocative until you remember what the alternative is. Every other form of money in the world today functions at the discretion of someone with the authority to revoke access. A central bank. A correspondent bank. A payments network. A custodian. The privilege of using those rails is granted and can be withdrawn. Satoshi's contribution was a monetary instrument whose properties do not depend on anyone's goodwill, which means it remains available to whoever picks it up. El Salvador picked it up. Corporate treasuries picked it up. This week an adversary regime under active sanction picked it up.

Why the Underperformance Is the Setup

Put the pieces together. Bitcoin sits more than thirty percent below its all-time high. The macro backdrop that should be its strongest tailwind, fiscal dominance and the repricing of sovereign credit, intensifies in real time. The asset has demonstrated, in live conditions over the active phase of a regional war, that it absorbs geopolitical shocks faster than any other liquid market and recovers at higher lows each time.

Its core properties have been validated by the most hostile possible adopter, which is a stronger endorsement than any institutional press release could provide. The infrastructure required for institutional participation matures further every quarter. ETF flows remain positive against the macro backdrop.

The CLARITY Act, working its way through Congress with Polymarket odds near seventy-three percent of passage, would be a catalyst. The case does not require it. Passage opens the institutional pipeline that has been waiting for regulatory cover. Failure leaves the fundamentals to compound at the rate they have been compounding for seventeen years, with adoption advancing through education and necessity rather than legislative permission. Both paths arrive at the same destination.

The risk-adjusted opportunity is exactly here. The asset has done its drawdown. The macro setup that should drive it intensifies. The properties that justify owning it have been stress-tested in public. The price has not yet caught up.

Closing thoughts

The bond market is telling a story this month that the equity market and the commodity market have been telling for longer. The post-1980 monetary regime, in which sovereign debt of developed economies functioned as the unimpeachable foundation of every portfolio in the world, is ending. Not tomorrow and not dramatically. The way these things always end, which is slowly and then all at once, in a series of repricings that look manageable in isolation and structural in aggregate.

The hard assets that compete with sovereign debt for that foundational role are the assets to own through the transition. Gold has moved. Bitcoin has not, yet. The one that has not is the asset with the asymmetric setup and the properties that the next monetary order will demand. Permissionless, digitally native, censorship-resistant, fixed in supply, and proven across every test the world has been willing to run.

That is the opportunity.

CHART OF THE WEEK

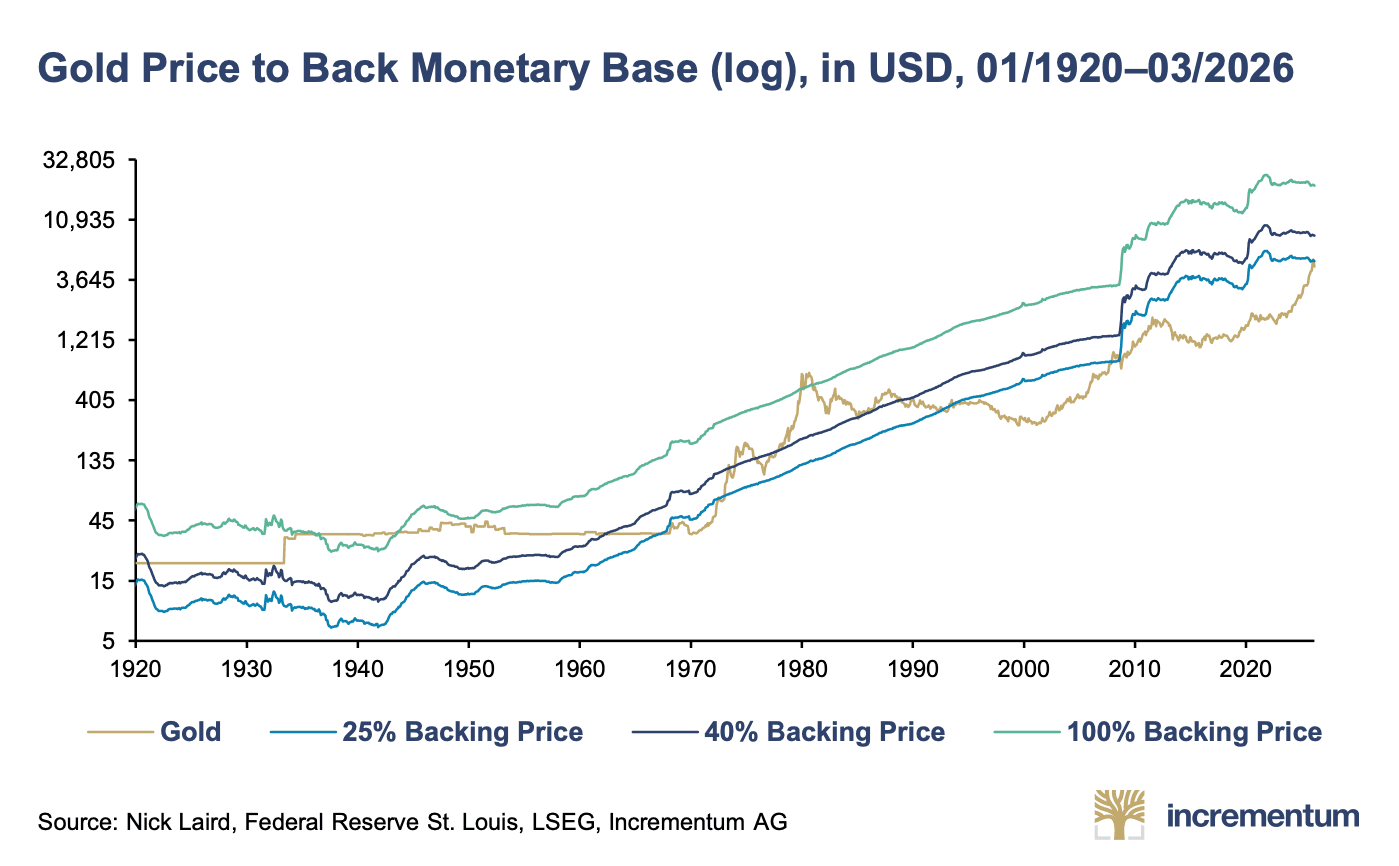

"The shadow gold price is the price level at which a return to a fully backed gold currency would be mathematically possible. We do not consider such 100% backing of M0, as is sometimes advocated, to be necessary; it would currently imply a gold price of USD 20,900 per ounce. During the era of the gold standard, the market forced central banks to maintain coverage ratios between one-third and one-half, which corresponds to a current gold price between USD 7,000 and USD 10,400 per ounce."

— IGWT Report 2026, Incrementum

QUOTE OF THE WEEK

"As fiscal pressures mount globally and politicians propose wealth taxes, the demand for 'outside money' – portable, jurisdictionless capital beyond the reach of discretionary rule changes – will likely intensify. Bitcoin was designed from its first line of code to serve precisely this function."

— IGWT Report 2026, Incrementum

PODCASTS OF THE WEEK

Morgan Stanley Now Recommends 4% Bitcoin Across $7T | James Seyffart

The Last Trade: James Seyffart of Bloomberg joins to break down the sentiment divergence between beaten-down crypto Twitter and a TradFi apparatus that's finally all in, Morgan Stanley launching MSBT at a market-low 14 bps with a 2-4% Bitcoin recommendation across 17,000 advisors and $7T+ in assets, Mike Wilson's 60/20/20 portfolio call adding 20% gold, and why the boomer diamond hands held through the drawdown while the basis trade collapsed from 10%+ to under 5%.

Iran Just Turned the World's Most Important Waterway Into a Bitcoin Market

Final Settlement: Liam, Brian, and Michael cover Onramp's $12.5M Series A, Iran's Bitcoin-denominated Hormuz Safe insurance platform, the Clarity Act's passage through the Senate Banking Committee, Hyperliquid's USDC pivot and partnership with Coinbase, Standard Chartered's acquisition of Zodia Custody, Gemini's mounting losses, and Prime Trust's $970M lawsuit against Swan Bitcoin.

Ray Dalio Is Wrong About Bitcoin & Bonds Are Breaking

In Episode 30 of The ₿roadcast, Bram Kanstein, Brian Cubellis, and special guest Liam Nelson break down the most important bitcoin and macro developments from the past few weeks.

Gold To $35,000? The Math Is Hard To Ignore | Josh Phair

The Last Trade: Josh Phair joins to break down the metal wars escalating between sovereigns, gold's run from $3,300 to $4,700 in nine months, why CLARITY's Senate markup tomorrow is a capital flight moment, Wyoming winning the state's first physical gold mandate over JP Morgan, and the Fair-Sinclair ratio pointing to $35,000 gold.

The Clarity Act Isn't Priced In: BNY, Morgan Stanley, & the End of Coinbase's Moat

Final Settlement: Liam, Brian, and Michael cover Coinbase's recent earnings report, the degradation of their competitive moat, the American Banking Association's panic due to the Clarity act, the implications of Circle's new token, and the significant moves made by institutions like BNY Mellon and Kraken.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis