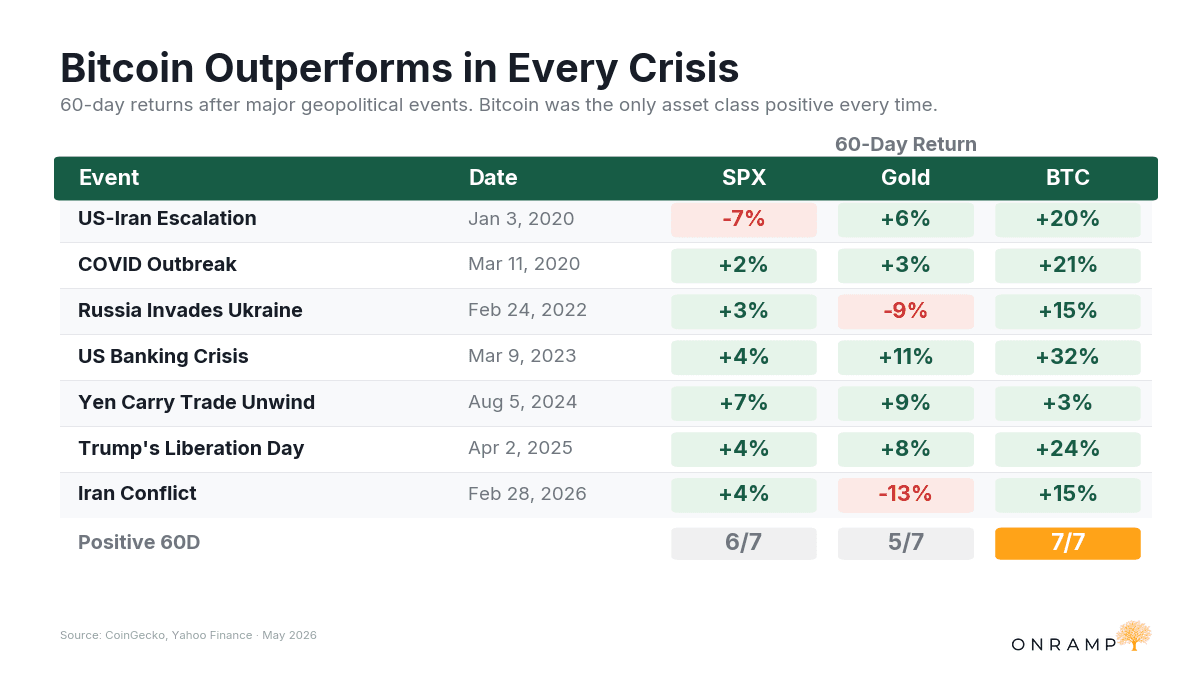

That track record reflects the properties of the asset. Bitcoin is the most censorship-resistant monetary instrument in history. Its payment network operates without the permission of any intermediary. Its supply schedule is fixed in a way that no other monetary asset has ever been or can ever be. These are testable claims, and seventeen years of adversarial pressure have tested them.

Nation-state pressure on the mining network. Exchange failures from Mt. Gox through FTX. Regulatory crackdowns in China, India, and across the Western banking system. The largest correlated risk-asset drawdown in a decade. The protocol came through each of them without an unscheduled inflation event, without a successful double-spend, without a halt to block production, and without losing the properties that define it.

This week delivered the most consequential validation of those properties to date. On May 16 Iran's Ministry of Economy and Financial Affairs launched Hormuz Safe, a state-backed maritime insurance platform that settles policies in Bitcoin for vessels transiting the Persian Gulf and the Strait of Hormuz. The ministry projects more than $10 billion in annual revenue if the platform captures meaningful share. Reports through April had floated the concept. This week it became a published ministry document, and a Bloomberg story carried into every institutional terminal in the world.

The reflex among Western commentators was to wave the announcement off as sanctions evasion. That reading misses what actually happened. A sovereign state under maximum financial pressure, locked out of the dollar system, evaluated its options for monetizing one of the most strategic maritime chokepoints on Earth and chose Bitcoin over gold, yuan, euros, and every other available rail. Whether Hormuz Safe ever achieves operational scale matters less than the fact that a sovereign actor has now built a billion-dollar revenue mechanism on top of the protocol and pointed it at the global energy trade.

Bitcoin was designed to be money for enemies. That sounds provocative until you remember what the alternative is. Every other form of money in the world today functions at the discretion of someone with the authority to revoke access. A central bank. A correspondent bank. A payments network. A custodian. The privilege of using those rails is granted and can be withdrawn. Satoshi's contribution was a monetary instrument whose properties do not depend on anyone's goodwill, which means it remains available to whoever picks it up. El Salvador picked it up. Corporate treasuries picked it up. This week an adversary regime under active sanction picked it up.

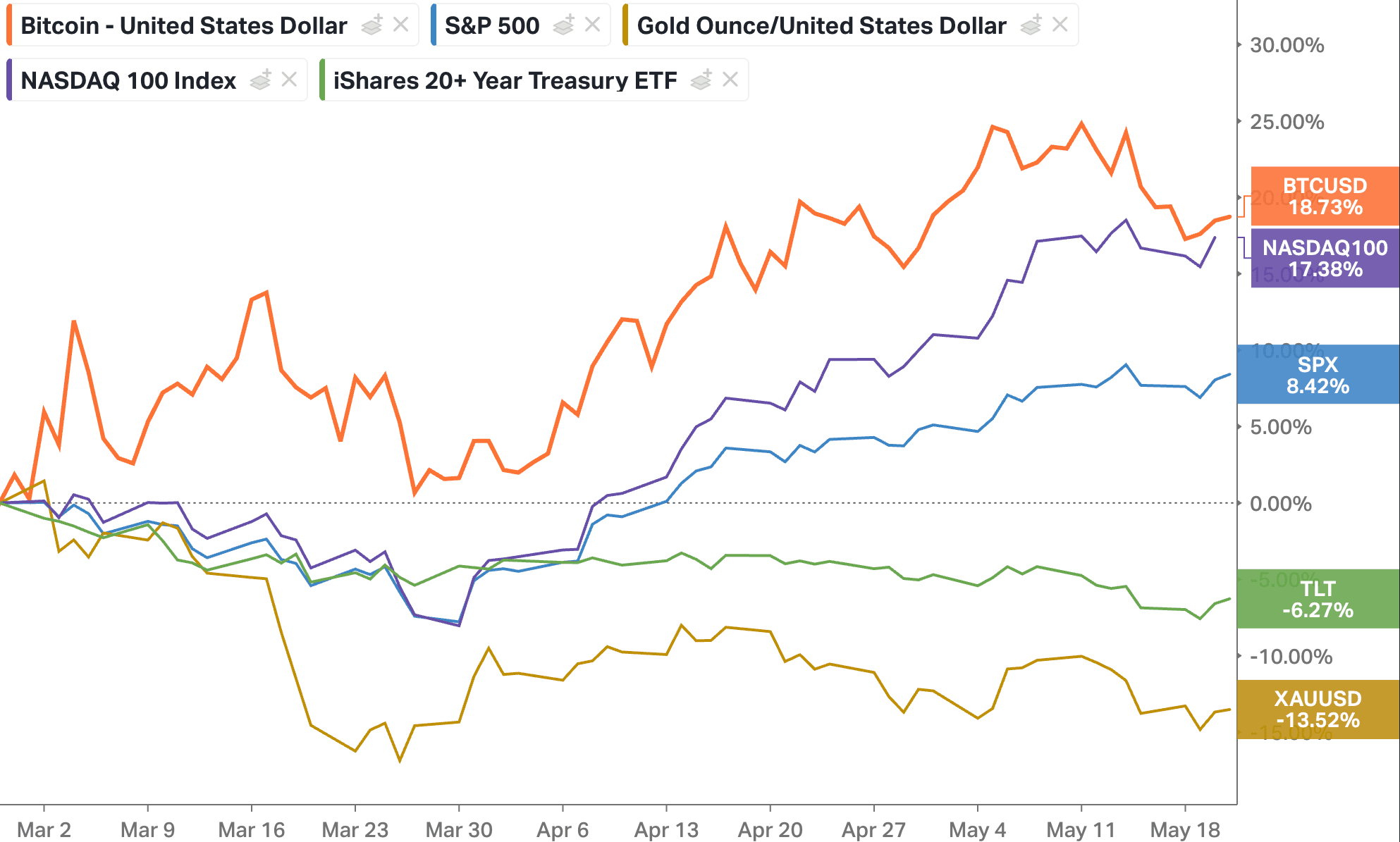

Why the Underperformance Is the Setup

Put the pieces together. Bitcoin sits more than thirty percent below its all-time high. The macro backdrop that should be its strongest tailwind, fiscal dominance and the repricing of sovereign credit, intensifies in real time. The asset has demonstrated, in live conditions over the active phase of a regional war, that it absorbs geopolitical shocks faster than any other liquid market and recovers at higher lows each time.

Its core properties have been validated by the most hostile possible adopter, which is a stronger endorsement than any institutional press release could provide. The infrastructure required for institutional participation matures further every quarter. ETF flows remain positive against the macro backdrop.

The CLARITY Act, working its way through Congress with Polymarket odds near seventy-three percent of passage, would be a catalyst. The case does not require it. Passage opens the institutional pipeline that has been waiting for regulatory cover. Failure leaves the fundamentals to compound at the rate they have been compounding for seventeen years, with adoption advancing through education and necessity rather than legislative permission. Both paths arrive at the same destination.

The risk-adjusted opportunity is exactly here. The asset has done its drawdown. The macro setup that should drive it intensifies. The properties that justify owning it have been stress-tested in public. The price has not yet caught up.

Closing thoughts

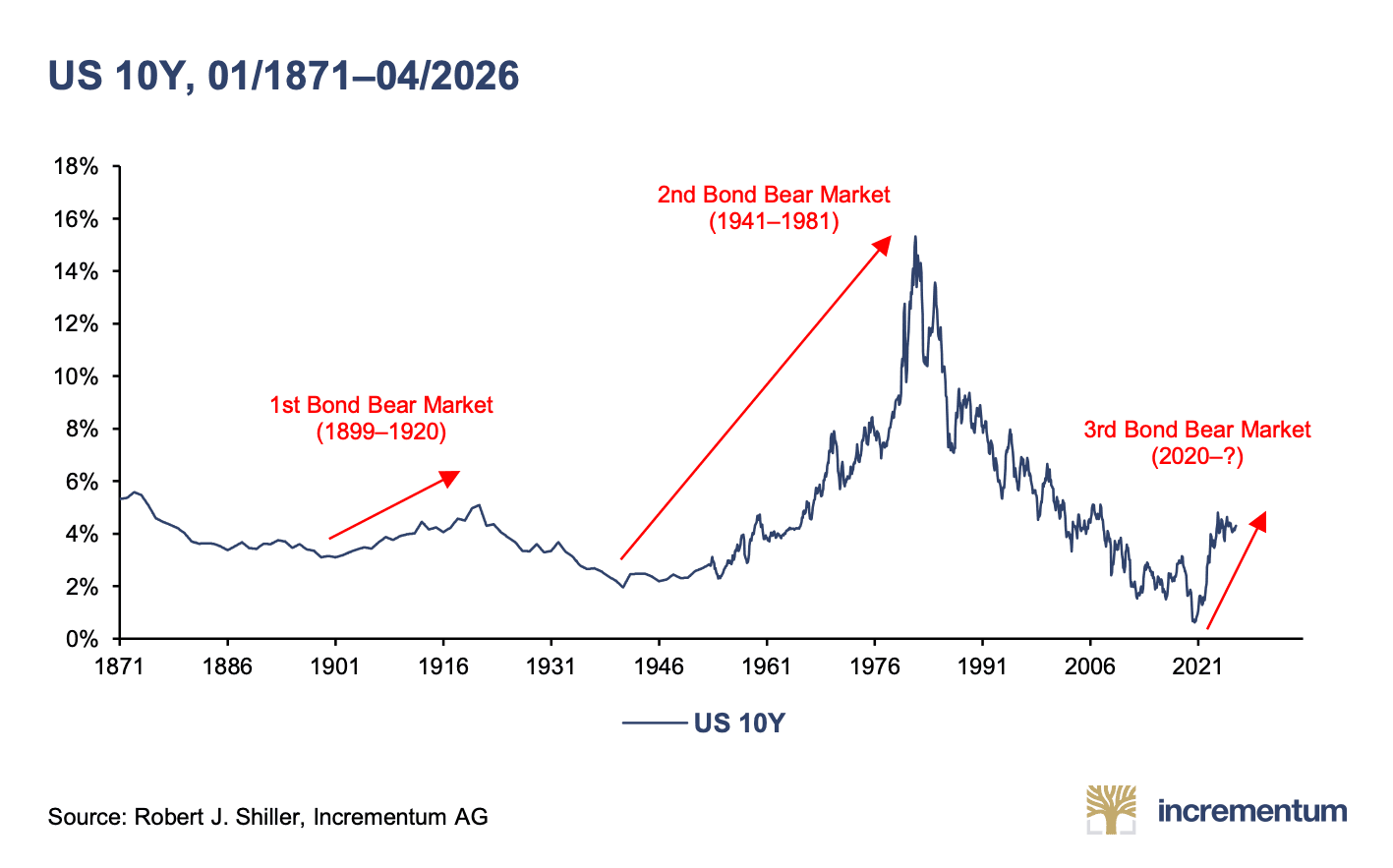

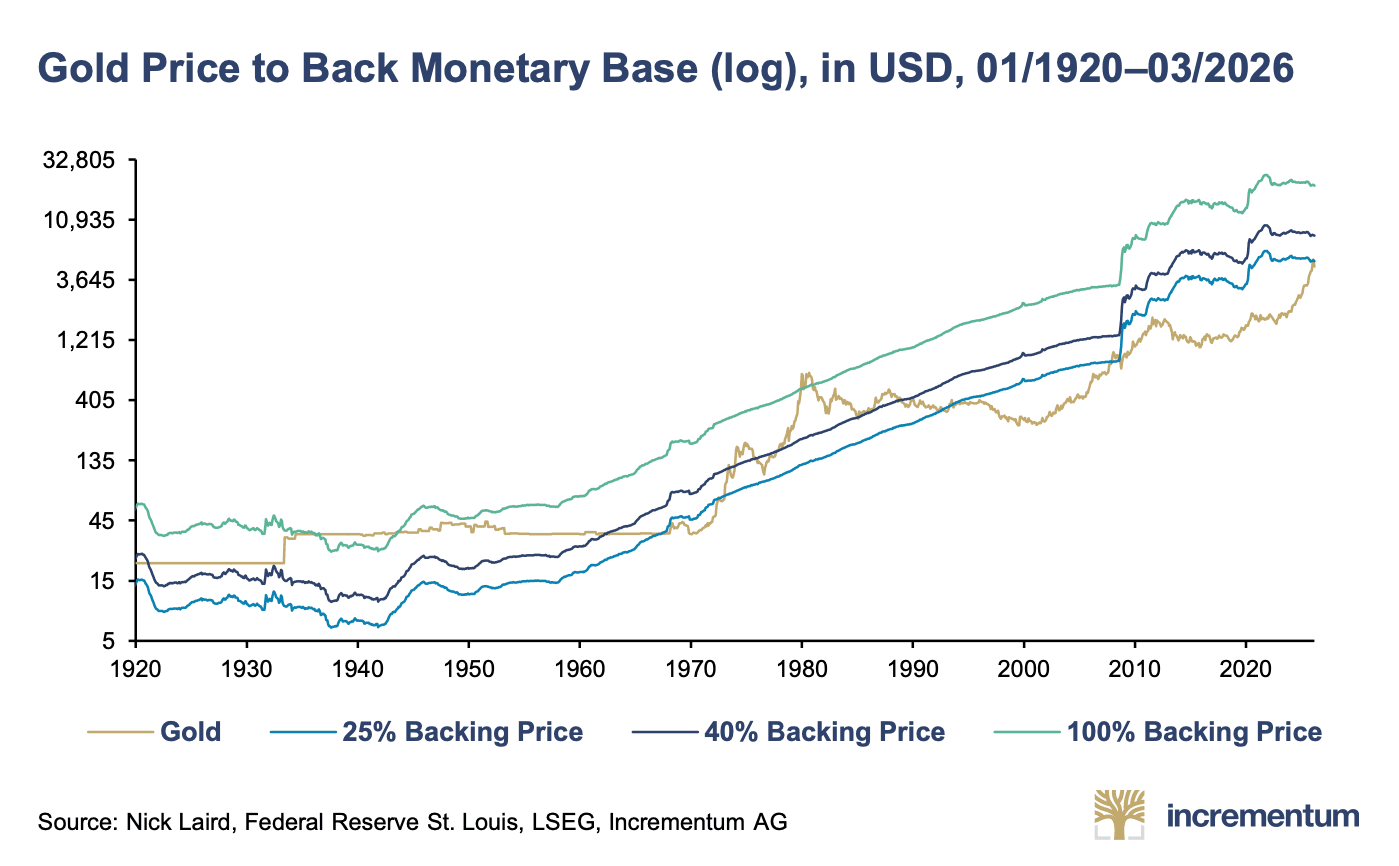

The bond market is telling a story this month that the equity market and the commodity market have been telling for longer. The post-1980 monetary regime, in which sovereign debt of developed economies functioned as the unimpeachable foundation of every portfolio in the world, is ending. Not tomorrow and not dramatically. The way these things always end, which is slowly and then all at once, in a series of repricings that look manageable in isolation and structural in aggregate.

The hard assets that compete with sovereign debt for that foundational role are the assets to own through the transition. Gold has moved. Bitcoin has not, yet. The one that has not is the asset with the asymmetric setup and the properties that the next monetary order will demand. Permissionless, digitally native, censorship-resistant, fixed in supply, and proven across every test the world has been willing to run.

That is the opportunity.

CHART OF THE WEEK