5/29/26 Roundup: The Quiet Funeral of the Native Token

Brian Cubellis | Chief Strategy Officer

May 29, 2026

This week David Hoffman, co-founder of Bankless and one of Ethereum's most visible advocates, sold all his ETH and wrote a careful case for it. He was writing about Ethereum. His admission exposes the whole altcoin complex, and the value-accrual story that was always marketing.

Below we unpack why the rotation never ends, why TradFi is absorbing the rails while leaving the ethos behind, why centralization wins the jobs these networks were sold to do, and why it all points back to the one asset that was never part of the argument. Followed by our standard Chart, Quote, and Podcasts of the Week.

The Quiet Funeral of the Native Token

Every so often a "crypto believer" walks to the edge of the same admission and stops short. David Hoffman is the latest. The Bankless co-founder spent nearly nine years building a career and a public identity on Ethereum, and on May 26 he published a careful case for selling his ETH, "Why I Sold My ETH."

What he gave up was narrow. He still believes a public-chain token can capture its network's value. He has only decided that ETH is not the one that will. So he turns to the tokens he thinks capture it better, Solana and NEAR and the chains priced on fees and burns, convinced there is a contest to win and that Ethereum lost it. The contest is the fiction. That is the part he has not reached.

Look at what capturing value means for the tokens Hoffman now prefers. A token priced on the fees its chain collects is equity on throughput. It moves with how much the chain gets used, the way a share price moves with a company's results, but there is no company underneath and no claim on earnings. It trades as if those things existed anyway. Ethereum giving its value to its ecosystem and Solana keeping more of its own ultimately come to the same conclusion. Neither coin is money. Hoffman wrote an essay refining his position inside a premise that was never true.

The premise survives because it was never an economic claim. It was the condition of the sale. A token gets created so the people who created it have something to sell. The claim that it captures the network's value is what makes it sellable. The premine, the foundation allocation, the round priced at a fraction of a cent, the listing, the unlock schedule that meters insider supply into retail demand over years. Value accrual is the story told on top. Once the early money is out at a markup, the token has done the only thing it was built to do, and the design stops needing it to do anything else. A decade of altcoin launches that perpetually decline in BTC terms shows exactly that.

The institutions building the serious version of on-chain finance confirm this reality. Banks and asset managers tokenizing Treasuries and issuing stablecoins are building permissioned ledgers and taking from the technology only the parts that work. Settlement in seconds. Programmable cash. Delivery against payment in a single step. One shared record that ends the reconciliation between firms. None of it needs a public network. None of it needs a token, and none of it ever did. What they wanted was the modernized database. Decentralization, even a purely theatrical version, is the part they refuse, because regulated assets require someone who can reverse an error, freeze a theft, and answer a subpoena.

A stablecoin and a tokenized Treasury are the same thing structurally, a token its issuer redeems against assets held off-chain. The permission lives at the asset layer, not on the rail, and the issuer who controls the redemption answers to a government. However "trustless" the chain underneath, the claim riding on it is not.

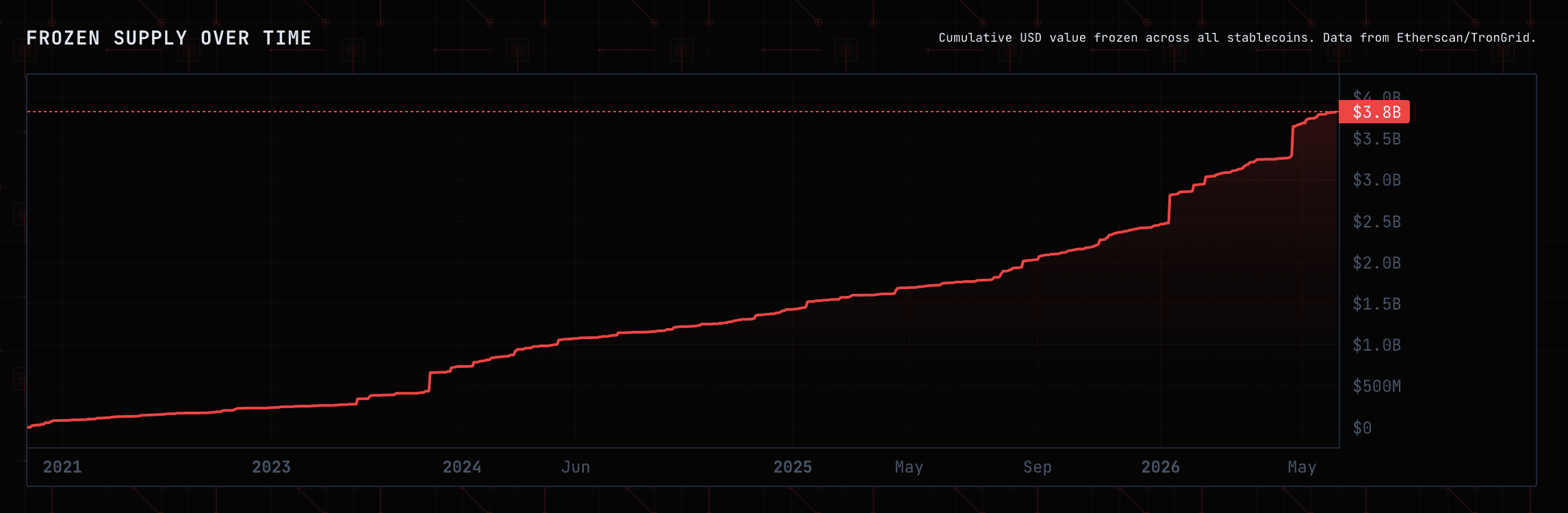

April 23 showed it plainly. Acting on OFAC and US law enforcement information, Tether froze 344 million dollars of USDT in two Tron addresses tied to Iran's central bank, blacklisting the tokens at the contract level so they cannot move. It was the largest single stablecoin freeze on record, and the Treasury added the addresses to its sanctions list days later.

One asset is not part of this argument at all. Bitcoin has no ecosystem to leak value into and no faster chain to lose a fee war to. No issuer can switch it off, because there is no issuer. Its token carries the value because the token is the reason the network exists rather than a fee skimmed from someone else's activity. Nothing runs downstream to applications. Nothing stands behind it for a court to reach. The premium stays because the whole design exists to hold it and the fixed supply anchoring it answers to no one. That is the property the rest of the field spent ten years trying to fake with burns and buybacks and revenue charts, and the one property that cannot be added after the fact.

The number that mattered this week sat under the noise. Bitcoin Core development rose sharply in 2025, with developer mailing-list traffic up about 60% year over year and contributors rising to 135 from 112, after several years of decline. The asset that never had to capture fees or outbuild a rival to be worth anything is the one pulling builders back. That reads as durability added to a network that already does its one job, not work done to defend a price.

Hoffman is half finished. He sold the token that would not accrue value and bought the ones that will not either, still chasing what was never there. A native token was a way to sell. The value it promised was the story that sold it. The funeral is already underway, and no one has noticed, because there is no body. There never was. Only a story, and people have quietly stopped telling it.

CHART OF THE WEEK

"So, for a third straight month, personal spending is running above personal income. This isn't sustainable, given the level/rate of personal savings. Eventually, the credit card is maxed, the savings are gone, and the consumer finally rings the bell."

— Robert infra on X

QUOTE OF THE WEEK

"If most people still do not understand digital money (bitcoin), you think that digital credit (a derivative of digital money) is more likely to help more people understand bitcoin than it is to confuse them? Let's just be honest about that logic."

PODCASTS OF THE WEEK

Bitcoin's Bottom Is In — But Saylor Is The Risk | Vijay Boyapati

The Last Trade: Vijay Boyapati, author of The Bullish Case for Bitcoin, joins to argue the bottom is in on what he calls a relatively shallow bear market, why the $100K-era whale distribution into ETF hands sets up a stronger base for the next run, what Charles Schwab onboarding 40 million clients through a Bitcoiner-led trading platform means for adoption, the Clarity Act expected to pass in the next month or two, and where Michael Saylor's stretch preferred-share strategy is starting to add real risk to Bitcoin.

Morgan Stanley Now Recommends 4% Bitcoin Across $7T | James Seyffart

The Last Trade: James Seyffart of Bloomberg joins to break down the sentiment divergence between beaten-down crypto Twitter and a TradFi apparatus that's finally all in, Morgan Stanley launching MSBT at a market-low 14 bps with a 2-4% Bitcoin recommendation across 17,000 advisors and $7T+ in assets, Mike Wilson's 60/20/20 portfolio call adding 20% gold, and why the boomer diamond hands held through the drawdown while the basis trade collapsed from 10%+ to under 5%.

Iran Just Turned the World's Most Important Waterway Into a Bitcoin Market

Final Settlement: Liam, Brian, and Michael cover Onramp's $12.5M Series A, Iran's Bitcoin-denominated Hormuz Safe insurance platform, the Clarity Act's passage through the Senate Banking Committee, Hyperliquid's USDC pivot and partnership with Coinbase, Standard Chartered's acquisition of Zodia Custody, Gemini's mounting losses, and Prime Trust's $970M lawsuit against Swan Bitcoin.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis