July 10, 2026 Roundup: The Asymmetry of Understanding

Brian Cubellis | Chief Strategy Officer

Free. Every week. One story that matters, read all the way down.

Bitcoin sits roughly 50% below its all-time high, sentiment is poor, and the critics have reached once more for their favorite verdict: no intrinsic value. But intrinsic value never meant what its modern users think it means. It was always a question about the future, what a thing will be worth and what purchasing power it will afford, and the gap between price and value has always been a measure of what the market has yet to understand.

This week we apply the oldest framework in investing to the most misunderstood asset in the world, and find that while the price has fallen, the deficits have grown, the debasement has continued, and the thesis has only strengthened.

The Asymmetry of Understanding

"It has no intrinsic value."

Few phrases get deployed against bitcoin with more confidence and less examination. The people who reach for it rarely stop to ask what intrinsic value actually meant to the discipline that coined the term, or whether the definition they are leaning on is accurate.

What value investing actually asked

Benjamin Graham, the father of security analysis, defined intrinsic value as the value justified by the facts: assets, earnings, dividends, and definite prospects, as distinct from quotations established by manipulation or distorted by psychological excess. The load-bearing words in that definition are facts and prospects. Cash flows are just one instrument for estimating those prospects when the asset in question happens to be a business. Graham never made them the definition itself.

Strip the concept down to its foundation and intrinsic value asks two questions. What will this thing be worth in the future? And more specifically, how much purchasing power will it afford me? That is the entire discipline of value investing in two sentences. Everything else, the discounted cash flow models, the book value screens, the margin of safety heuristics, is machinery built to answer those questions for one specific asset class: equity claims on productive enterprises.

Over time the machinery got confused with the concept. "Intrinsic value" hardened into "the present value of future cash flows," and anything without cash flows was declared valueless by definition. This is a category error with a long history of embarrassing its adherents. Gold has no cash flows and has preserved purchasing power across five millennia. Farmland stored wealth long before anyone modeled crop yields. Humanity has always assigned durable value to scarce things with useful monetary properties, and markets have always priced them.

Mispricing is an information problem

Here is the second piece of the value investing tradition that gets forgotten. Why would anything ever trade below its intrinsic value in the first place? Graham's answer, and the answer of every value investor since, is that markets misprice assets when market participants misunderstand them. A stock trades at a discount because the market has not done the work. It has not read the filings, has not understood the business model, has not correctly weighed the prospects.

The value investor's entire edge is information asymmetry. You understand something the market does not, and you get paid as understanding spreads and price converges toward value. That convergence has always been the mechanism.

Now apply the same lens to bitcoin.

The most mispriced asset in the world, definitionally

Bitcoin's dollar price at any given moment has always been disconnected from its intrinsic value, and the reason is structural. The share of humanity with a deep understanding of bitcoin's monetary and technological properties, and of its role in a world of unconstrained fiat issuance, rounds to well under 1% by any realistic estimate.

The data bears this out, with an honest caveat up front: every figure that follows is an estimate. The blockchain records addresses rather than people, one person can control dozens of addresses, and a single exchange address can represent millions of customers, so precision is impossible by design. The direction and magnitude of the numbers, however, are not in dispute.

Start with the broadest measure. CoinShares' meta-analysis of more than 20 independent ownership surveys, including work from Cambridge and the Bank of Canada, estimates that roughly 400 million people worldwide have some form of bitcoin exposure, about 5% of the global population. But exposure reveals very little about understanding.

The Cornell Bitcoin Research Project surveyed more than 25,000 people across 25 countries and found that while roughly 90% recognize bitcoin, only 13% could explain its core features, including the fixed supply of 21 million coins. The single most important fact about the asset, the property from which everything else follows, is unknown to the overwhelming majority of people who can name it, and to a meaningful share of the people who own it.

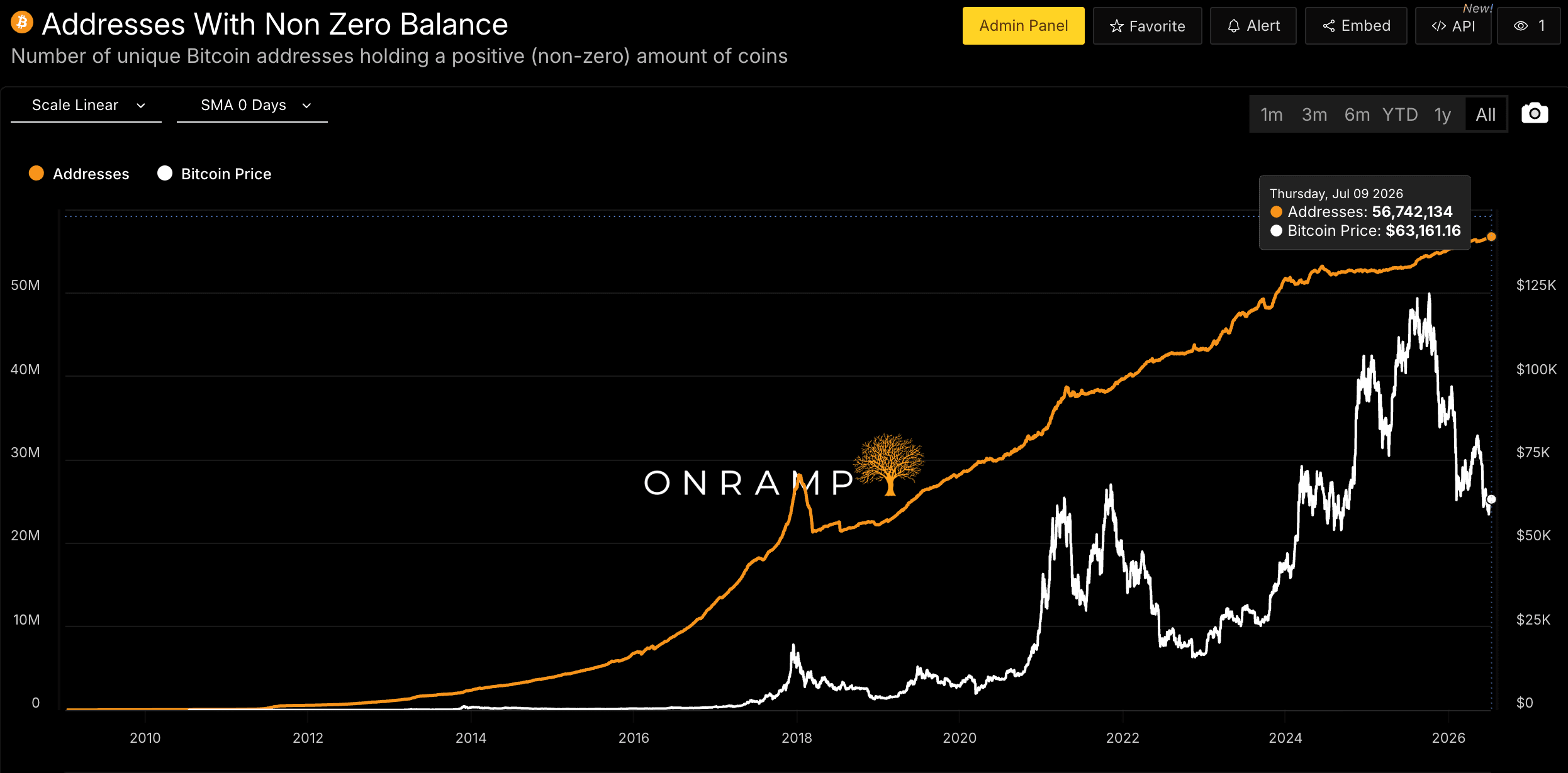

Non Zero BTC Balances; Onramp Terminal

Move from awareness to conviction and the numbers collapse. Here the measurement shifts from survey estimates of people to what the blockchain itself records, which is a much narrower lens. On chain, roughly 57 million addresses hold any bitcoin at all. Of those, the best estimates suggest only 4 to 5 million addresses hold at least 0.1 BTC, a reasonable proxy for someone who has done some amount of research and committed material savings, and fewer than 1 million hold a full coin, a population thinned further once exchanges and custodians are accounted for.

UBS counts roughly 2.2 billion adults with a net worth above $10,000, the realistic addressable market for a savings technology. Against that base, the cohort holding a meaningful position in the scarcest monetary asset ever created amounts to roughly 0.2% at the generous end, and against the full global population of 8.2 billion it rounds to 0.06%.

If price converges to value as understanding spreads, and the population with genuine conviction rounds to roughly 0.2% of the addressable market, then bitcoin's dollar price at any moment reflects the current state of global bitcoin education far more than it reflects the properties of the asset. The market can only price what its participants comprehend.

The gold benchmark

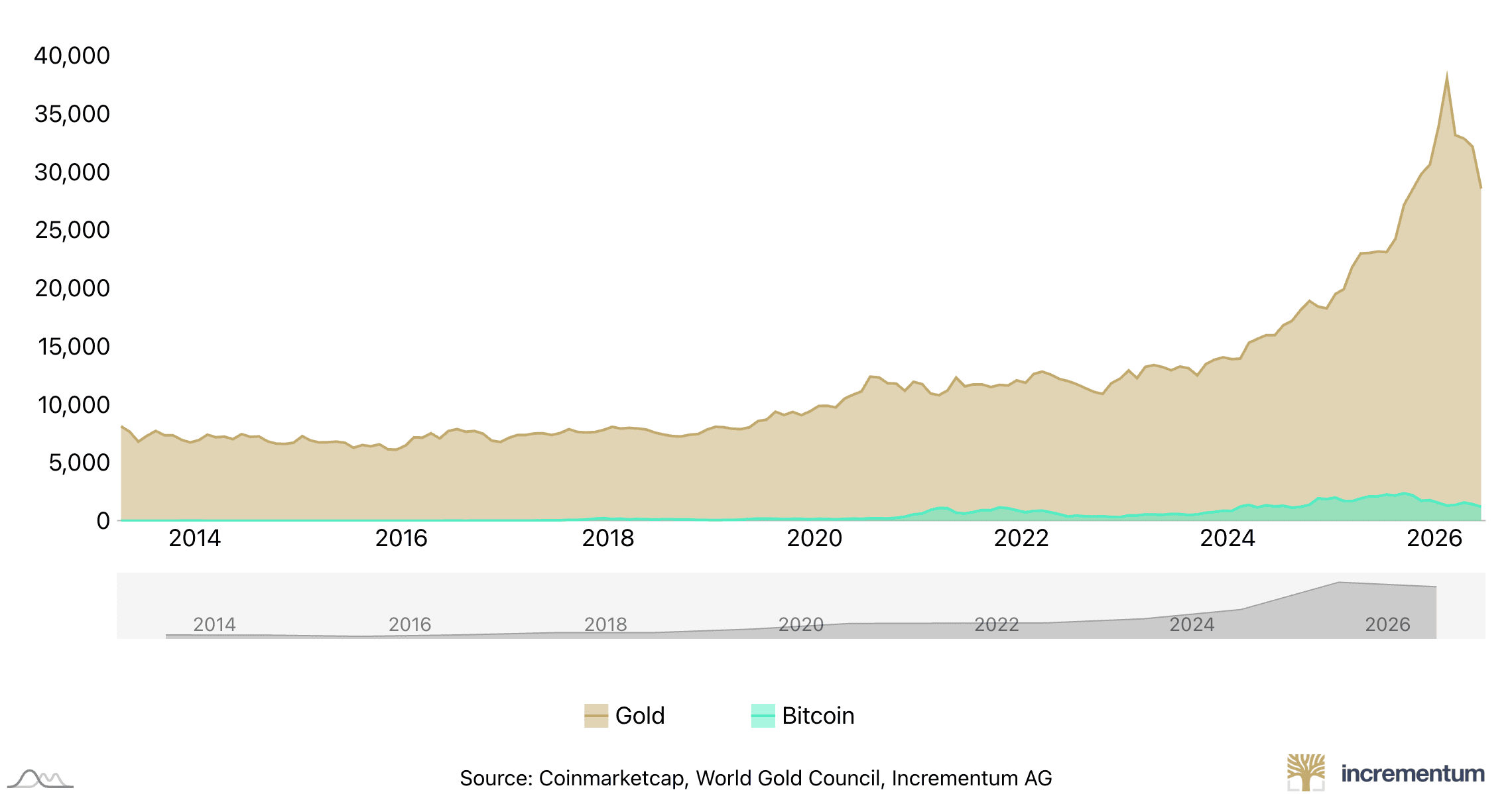

Consider the counterfactual. Suppose everyone who currently holds gold understood that bitcoin possesses every monetary property that makes gold valuable, scarcity, durability, fungibility, divisibility, and improves on gold decisively in verifiability, portability, and the credibility of its supply schedule. Gold's above-ground supply grows roughly 1.5 to 2% per year and expands further whenever price incentivizes marginal mining. Bitcoin's terminal supply is fixed and enforced by the most powerful computing network ever assembled. Under full information, one could argue that bitcoin should trade at gold parity as a floor (~$1.5 million per BTC).

Source: Incrementum

Today gold's market capitalization sits around $29 trillion against bitcoin's roughly $1.2 trillion. The market currently prices bitcoin at roughly 4% of an asset it is, at minimum, equivalent to. That gap is the information asymmetry expressed in dollar terms.

And to be intellectually honest, even gold trades below its own intrinsic value. Most people do not understand sound money. They do not know why gold held purchasing power for five thousand years while every fiat currency in history has decayed or died. Gold benefits from a track record so long that people trust the conclusion without grasping the mechanism. Most people accept that gold is valuable without being able to articulate why. Bitcoin does not yet enjoy that inherited trust, which means its case has to be learned rather than assumed. Learning takes time. It also, once it happens, tends to stick.

Why the knowledge compounds

Skeptics will grant the framework and then ask the obvious question: if bitcoin is valuable because of its properties, what stops the next bitcoin from diluting it?

History already ran that experiment, thousands of times, and the results are unambiguous. Anyone can copy the code, and thousands have. What nobody has managed to copy is the credibility, because bitcoin's launch conditions were unrepeatable. There was no pre-mine, no insider allocation, no founder equity. Satoshi released the network into a world where everyone had access to it and essentially nobody cared, it traded at effectively zero for months, and then he disappeared without ever cashing in.

You cannot recreate an environment of universal indifference now that the entire world has heard of the category. Every subsequent launch faces the bootstrapping paradox in reverse. Attention arrives before neutrality can be established, and insiders position themselves accordingly. The incentive structure of every post-bitcoin token guarantees it.

The graveyard tells the rest of the story. Thousands of altcoins promising superior technology have failed to sustain a monetary premium. Seventeen years of intermediaries and engineered yield schemes collapsing, while the protocol underneath produced its next block, on average, every ten minutes. Far from discrediting bitcoin, these failures function as the curriculum. Each collapse teaches the market, painfully and permanently, to distinguish the asset from the industry that grew up around it, and to understand which properties actually matter.

This is why the education only moves in one direction. Understanding bitcoin is a one-way function. Once someone genuinely grasps the supply schedule, the launch history, and the incentive structure, they rarely unlearn it. Meanwhile the other half of the curriculum writes itself. Every deficit, every debt ceiling standoff, every round of monetary expansion makes the ills of fiat money more legible to more people.

The conclusion the framework demands

Which brings us to the present moment. Bitcoin sits roughly 50% below its all-time high. Sentiment is in the gutter, the tourists have left, and the obituaries are running again, adding to a tally that already sits in the hundreds across bitcoin's seventeen years. If you believe price and value are the same thing, this looks like failure. If you understand the framework laid out above, it looks like something else entirely.

Ask the value investor's questions of this moment. Has anything changed about what bitcoin will be worth in the future, or the purchasing power it will afford? The supply schedule is intact. The network continues to produce blocks roughly every ten minutes. The properties that constitute its intrinsic value are exactly where they were at the high. What has changed is the world around the asset, and it has changed in one direction. Deficits are larger, debt service is heavier, and the currency debasement that forms the other half of bitcoin's investment case has continued without pause.

The thesis sits unchanged while the conditions that produce the thesis keep deteriorating, which means the drawdown has widened the gap between price and value rather than closed it. A 50% decline against a strengthening thesis is the persistent disconnect described above, temporarily exaggerated. For the informed, sats are simply on sale.

And the informed know how this particular chapter ends, because it has been written before. Bitcoin will once again fail to die, and its survival will do what every prior survival has done. It will mint a new class of students. People who watched the obituaries pile up will ask the only question that matters: why didn't it die? That question is the top of the funnel. It leads to the supply cap, then to the launch history, then to the incentive structure, then to the monetary properties, and it ends where it always ends, in understanding and ultimately adoption. The drawdown that convinces the uninformed to leave is the same event that recruits the next cohort of the informed.

All bitcoin adoption, and therefore all bitcoin price appreciation, is a function of education spreading. The understanding of what makes it decentralized, secure, and finite. Digital sound money. The best savings technology ever engineered. The intrinsic value question, asked properly, was always about future purchasing power, and on that question a credibly finite asset in a world of infinite currency issuance has an answer no discounted cash flow model was ever equipped to give.

The spread between price and value closes one student at a time.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis