June 19, 2026 Roundup: New Chair, Old Gravity

Brian Cubellis | Chief Strategy Officer

Free. Every week. One story that matters, read all the way down.

Kevin Warsh chaired his first Fed meeting on Wednesday and held rates at 3.5 to 3.75 percent, as expected. He cut the statement to a third of its length, dropped forward guidance, kept his own dot off the plot, and the new forecasts walked back the cut the Committee expected in March. Most of the coverage landed in one place, that a president who wanted a rate-cutter got a hawk.

But the hawkishness is mostly a credibility exercise. Warsh talked up price stability while the balance sheet he inherited has been buying Treasuries again since December. With federal debt nearing 40 trillion dollars, the path bends back toward easier money, and a firm opening mainly buys him room to get there on his own schedule. Followed by our standard Chart, Quote, and Podcasts of the Week.

New Chair, Old Gravity

Wednesday afternoon the Federal Open Market Committee left its target range for the federal funds rate at 3.5 to 3.75 percent, where it has sat since the central bank eased by three-quarters of a point late last year. The decision was a foregone conclusion. The interest of the day was Kevin Warsh, running his first meeting since being sworn in on May 22 as the seventeenth Chair of the Federal Reserve, a week after Jerome Powell's term in the role came to an end.

Warsh arrives with a profile unlike most of his recent predecessors, having sat on the Board during the 2008 crisis, come up through Morgan Stanley rather than the academy, and reached the job without a doctorate in economics. He had promised something close to a regime change in his confirmation hearings, and the first evidence of it was on the page before he spoke.

The policy statement ran roughly 130 words, down from the three hundred and more that had become routine under Powell. The forward guidance that markets had picked over line by line for a decade was gone, dismissed as poorly suited to the present moment. Warsh described what remained as a plain account of the facts, and he carried the same economy into the press conference, telling one reporter he had nothing to add beyond the statement itself. He declined to submit his own projection to the dot plot. He announced five task forces to reexamine the machinery of policy, covering communications, the balance sheet, the data the Fed leans on, the effect of new technologies including artificial intelligence on employment, and the framework the Fed uses to define and pursue price stability.

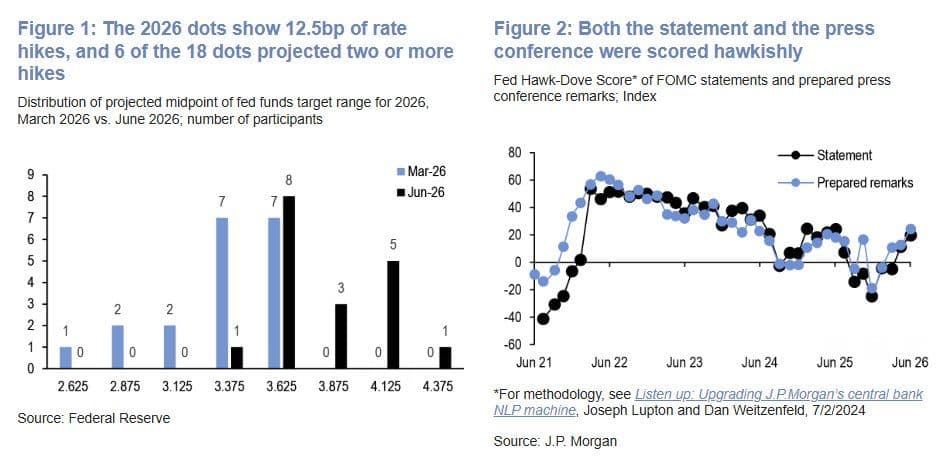

The projections that came with the decision moved in a hawkish direction. In March the median participant still expected a cut this year and a year-end rate near 3.4 percent; this time the median rose to 3.8 percent, and nine of the participants who submitted forecasts now pencil in at least one hike before December, where three months ago not a single one did. J.P. Morgan's language model, which scores these communications for tone, marked both the statement and the prepared remarks as hawkish. Markets took the cue. Two-year Treasury yields jumped sixteen basis points to 4.21 percent, their highest in more than a year, the dollar posted its best day in almost twelve months, equities slipped, and gold gave back more than two percent.

So the story wrote itself, and most of the desk notes filed by the close on Wednesday told it the same way. The president put Warsh forward expecting quick cuts, and at one point joked that he would sue his Chair if they did not come. Instead the new Chair came out sounding like the hawkish governor he was fifteen years ago, refused to flinch, and let the market reprice toward a hike. The conclusion drawn almost everywhere was that Warsh had announced his independence.

The Entry Fee

That reading is incomplete rather than wrong, and the more useful way to look at the meeting is to ask what the hawkishness was for. Warsh inherited a credibility problem that is partly the Fed's, since inflation has run above target for five years, and partly his own, since he was installed by a president who wanted him to cut and said as much in public. Before he can ease without markets treating it as capitulation to the White House, he has to establish that he is nobody's instrument. A hard, plain, hawkish first outing is how that credibility gets banked. It is the entry fee for the freedom to do later what the numbers will eventually call for, and to have it read as data rather than politics.

Once you hold the meeting up to that light, the dovish material is easy to find, sitting in plain sight under the stern delivery. Start with the decision to withhold his own dot. A Chair set on a higher path could have planted a hawkish marker in the projections and anchored the Committee to it. Warsh left his line blank, which keeps his own hands free and commits him to nothing. The end of forward guidance works the same way, and it cuts in both directions at once. Retiring the language stripped out the easing bias that had lingered in the old statements, which reads as hawkish, but it also frees the Chair to pivot whenever he likes without breaking a prior promise, which is the more durable advantage. A central bank that has guided to nothing can turn on a single data print and owe no one an explanation.

The framing of the inflation itself is the largest tell. The statement attributes the price pressure to supply shocks in particular sectors, energy chief among them, after the conflict with Iran and the disruption around the Strait of Hormuz drove fuel costs sharply higher earlier in the year. Blaming supply rather than demand is the classic groundwork for patience, because supply shocks are the kind of inflation a central bank is supposed to look through rather than crush. Oil has already come well off its highs, and if energy keeps normalizing while the Fed has spent the spring describing the inflation as an energy story, the path to calling the problem largely solved is a short one.

Warsh paired all of this with heavy emphasis on data dependence and a stated preference to let markets respond to incoming data rather than to Fed signaling, which is another way of saying he has committed to react and to nothing else. Even his defense of the two percent target carried a hinge. Asked whether he would reconsider it, he said no, but added that he saw no reason to revisit it until the Fed had reestablished its ability to deliver it, which quietly concedes that the target is a subject for another day once credibility is back in hand.

There is also a quieter lever that the rate decision tends to overshadow, and it is already pointed toward easing. The Fed stopped shrinking its balance sheet at the start of December and, ten days later, instructed the New York desk to begin buying Treasury bills again, presented as routine purchases meant to keep bank reserves ample as the economy grows. Whatever the intent behind the label, the Fed's Treasury holdings have climbed by close to 300 billion dollars since then, and its footprint in the market is expanding rather than shrinking. Warsh reaffirmed the ample reserves policy in his statement and set up a task force to study the balance sheet, so the purchases carry on under him. Rates are the lever everyone watches, and the balance sheet is where liquidity is quietly being added even now.

Monetary Gravity

None of this is to claim Warsh is secretly dovish by temperament, or that a hike this autumn is off the table. The point is structural, and it explains why a meeting that read as hawkish on the surface leaves every door to easier money open underneath. It also fits the constraint he cannot talk his way out of. Gross federal debt now stands near 39 trillion dollars and is on course to cross 40 trillion before the year is out. Net interest on that debt is running at roughly a trillion dollars a year, having already passed what the country spends on national defense and trailing only Social Security among federal outlays, and as a share of the economy it has reached a level not seen since the early 1990s. Every basis point of higher-for-longer rates compounds that burden as the Treasury rolls older, cheaper debt into new issuance at today's yields. A central bank truly free to fight inflation would not have to weigh the solvency math of the government that chartered it. This one does, and the gravity of that arithmetic pulls in one direction over any horizon that matters.

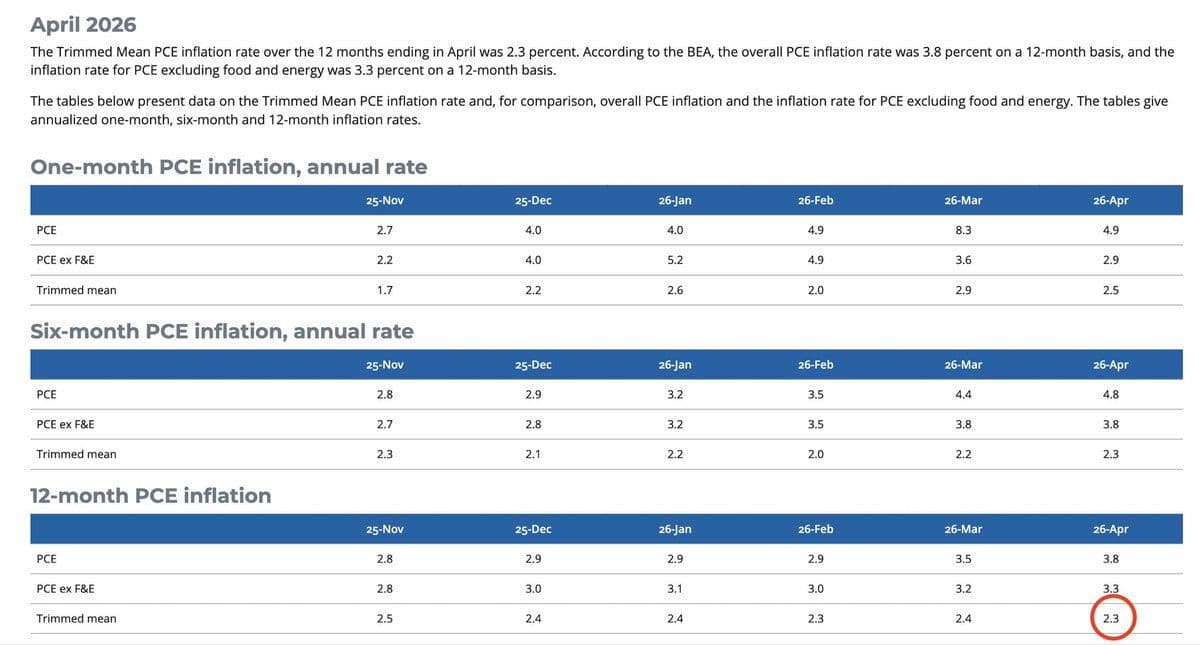

The task forces are worth watching with this in mind, because they double as an apparatus for justifying the turn when it comes. The one on inflation frameworks is the obvious example. Depending on the gauge, inflation today reads anywhere from the 4.2 percent of the May consumer price index, a three-year high and the third straight month of acceleration, down to roughly 2.3 percent on the Dallas Fed's trimmed mean measure, which strips out the largest outliers, energy among them.

A committee that wanted room to cut without abandoning the two percent number could lean on the friendlier measure and call the job nearly done. That is not a forecast, but it is the sort of move a credibility-minded Chair has every incentive to make, and it would change nothing about the dollar's actual path.

The other route to the same place runs through the opposite risk. The selloff on Wednesday was driven by a jump in real rates, with nominal yields rising while market measures of expected inflation fell, which is precisely why gold softened and the dollar firmed. Whether the next few quarters bring sticky inflation or a liquidity scare, the reflex at the end of the road is the same, which is to add liquidity and let the currency give way, whichever direction the danger arrives from.

On Schedule

On the destination, Warsh was unintentionally clear. The argument inside the Fed has never been whether to debase the currency, only how quickly, and a hawk is simply someone who would prefer to do it on schedule.

This is the backdrop against which a fixed monetary standard makes its case, and it needs no view on the October meeting to make it. Gold has held value against fiat and against sovereign bonds for centuries precisely because no committee can vote more of it into existence on short notice, and its standing as the senior risk-off asset is not diminished by one hawkish session or one strong day for the dollar.

Bitcoin carries that same scarcity into a form suited to a digital economy, without gold's costs of storage, assay, and transport, and with a monetary policy that is settled at the level of the protocol rather than decided by a committee, with no chair to confirm it and no target built on the quiet assumption that your savings should lose ground each year by design.

Warsh may well run a plainer and more disciplined Fed, and there is something to respect in the candor of a shorter statement. Discipline of style, though, is not the same as discipline of money, and the institution he now leads is bound to a debt and a mandate that make gradual debasement the path of least resistance. The hawkish first act is exactly what a credible slow play looks like. The destination has not changed, only the pacing, and the reasons to hold a monetary asset no government can print are stronger than ever.

CHART OF THE WEEK

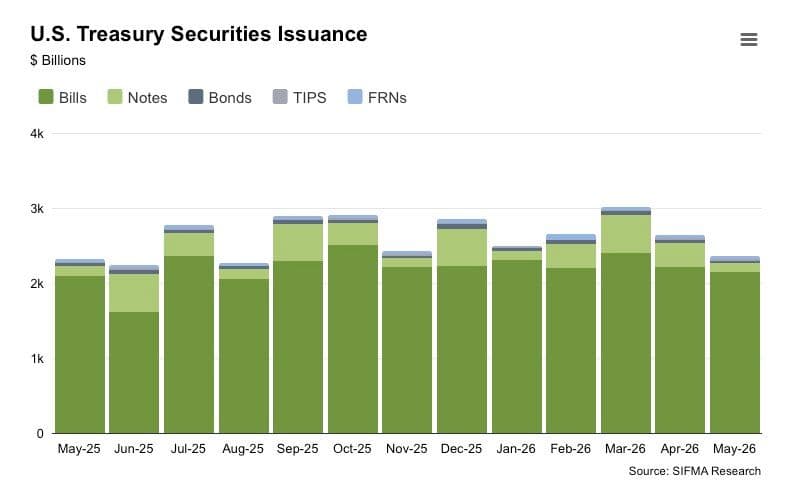

"2026 will see over $30 trillion in debt issuance by the US Treasury. 85% of that debt is <1yr in duration. Even modest hikes would dramatically increase interest expense (as if current levels weren’t bad enough). This is why it’s a high bar for a hike."

QUOTE OF THE WEEK

"I can't give you any guidance on what we're going to do next."

— Kevin Warsh

PODCASTS OF THE WEEK

The AI Trade Is Repeating the Dot-Com Cycle | Mark Yusko

The Last Trade: Mark Yusko, CIO of Morgan Creek Capital Management, joins to call the SpaceX IPO and the broader AI capex wave the greatest bubble in the history of markets, why Elon's $1 trillion XAI revenue promise by 2030 is securities fraud, how DeepSeek is poised to break the AI bubble by doing what OpenAI and Anthropic do for 5 cents on the dollar, why Bitcoin's Metcalf's Law fair value already sits around $125,000 even as price trades closer to $60K, his specific October 5 cycle-bottom call for the next crypto spring, and the brutal truth that the 1986 Tax Act and the rise of the 401k were a heist on the American middle class.

Inside the SpaceX IPO And Why Bitcoin Is the Value Trade

Final Settlement: This week Brian, Michael, and Liam cover the SpaceX IPO and the capital-rotation narrative around Bitcoin, the Bernie Sanders / David Sachs debate over government equity stakes in AI companies, the Zcash inflation bug that allowed unlimited mint for four years before Claude caught it, JPMorgan's tokenized-deposit consortium with Citi, Bank of America, Wells Fargo, and Chase, the Stripe / Visa / MasterCard stablecoin consortium, Morgan Stanley's Galaxy partnership letting high-net-worth clients lend Bitcoin for in-kind ETF conversions, Tether's first gold-backed Visa card, the US sanctioning Iran's largest crypto exchange Nobitex, and the Polymarket MicroStrategy resolution controversy.

CLOSING NOTE

Onramp provides bitcoin financial services built on multi-institution custody. To learn more about our products for individuals and institutions, schedule a consultation to chat with us about your situation and needs.

Until next week,

Brian Cubellis