June 30, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

This week's brief examines the May crash in tokenized Anthropic and OpenAI exposure, where investors learned that a token claiming to track private-company stock is only as good as the company-approved ownership record behind it. The Radar follows the same ownership-and-infrastructure theme across on-chain lending, stablecoin issuance, AI chip challengers, coding-agent economics, tariffs, gold reserves, and geopolitical precedent.

In May, a digital token called "Anthropic" traded at a price implying the company was worth more than a trillion dollars. Then Anthropic said the shares behind those tokens did not legally exist, and the price of those tokens fell by nearly half in a day. The tokenization boom is rediscovering, fast, why a century of securities law exists.

A Receipt for Nothing

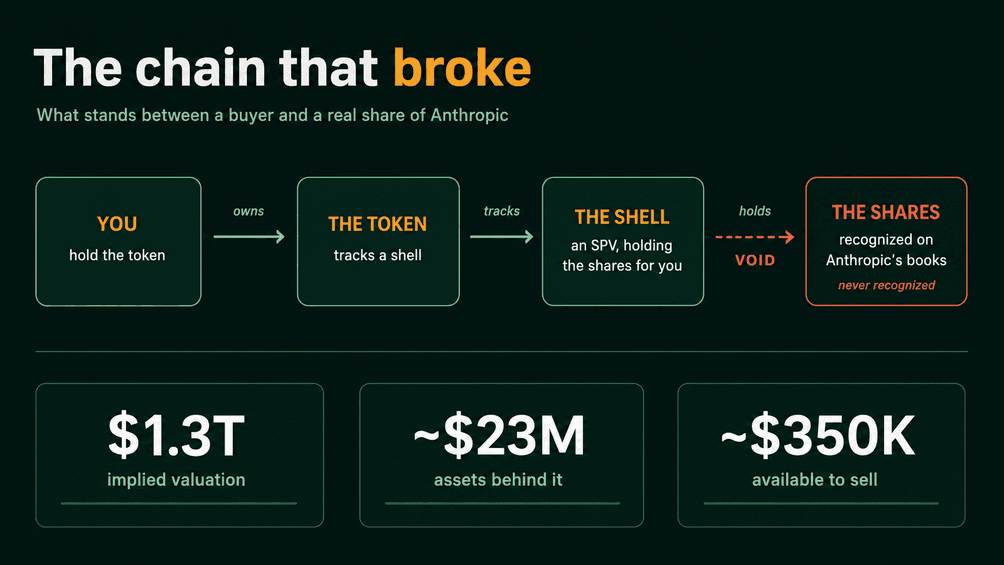

On the morning of May 13, 2026, you could buy a token on the Solana blockchain called Anthropic. It traded actively, it had a price chart, and at its peak that price implied that Anthropic, the maker of Claude and one of the fastest-growing companies in the world, was worth more than 1.3 trillion dollars. Then Anthropic updated a page on its own website. Any transfer of its stock that the company had not approved, it said, was void. Not disputed, not voidable. Void. The buyer would not be recognized as a shareholder and would hold nothing. Within a day the token had fallen close to 40 percent, and the OpenAI token trading beside it fell about as far. What thousands of people believed they owned, the company said they had never owned at all.

The token came from a platform called PreStocks, and the way it was meant to work is worth following slowly, because the whole story sits in the plumbing. You bought a token on Solana. The token was meant to track a special purpose vehicle, a shell company set up to hold an asset for a group of investors. The shell was meant to hold real Anthropic shares. And those shares were meant to be recognized on Anthropic's own books. Four links in a chain: holder, token, shell, recognized shares. The companies confirmed that the last link had never existed. Anthropic does not allow shell companies to hold its stock, and any transfer into one is void under its rules. The chain ended in mid-air, and everything hanging from it fell.

The shell was rarely even a single clean layer. Because a company has to approve who holds its shares, the workaround that grew up in the private markets was the special purpose vehicle, and then vehicles nested inside other vehicles. A PitchBook analyst described the result as layers of shell companies stacked on layers of fees, each layer taking a cut and each one adding another joint where the structure could fail. The token at the far end was only ever as sound as the weakest link behind it, and the buyer usually could not see the links at all. The interface showed a clean price going up. The structure underneath was a tower of intermediaries, the bottom of which rested on a permission that had never been granted.

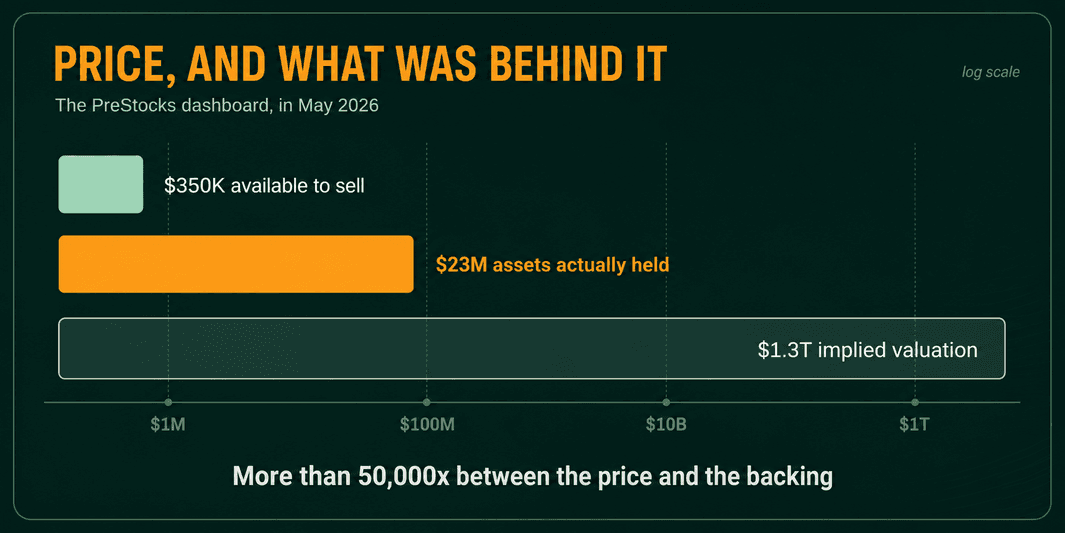

Beneath the legal problem sat a second one. PreStocks said every token was backed one for one by real shares, but it had never published the audits it promised at launch, and the figures that were visible did not inspire confidence. At one point the platform's own dashboard implied Anthropic was worth more than 1.3 trillion dollars while the vehicle behind the tokens held about 23 million dollars in assets. That is a gap of more than fifty thousand times. The pool of money actually available for anyone who wanted to sell came to roughly 350 thousand dollars. So a believer who had doubled his money on paper could not have taken it out, because when confidence breaks, everyone tries to leave through the same narrow door at once and the people who hesitate get nothing. The token had a price. It did not have much of anything behind the price.

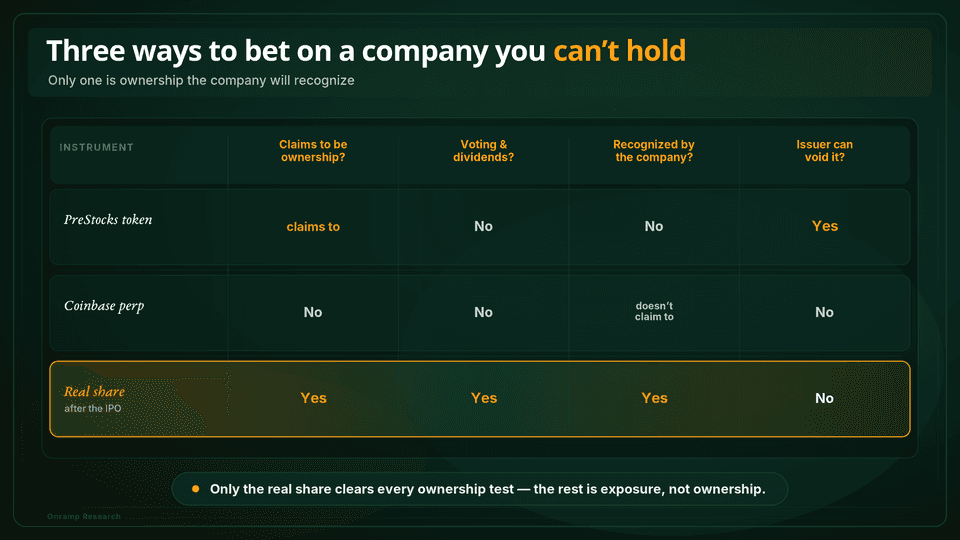

Some platforms reached for the defense that they held the shares directly, with no shell in between. When a version of this fight reached Robinhood last year, the firm insisted that its vehicle owned 75 million dollars of OpenAI stock outright, with no SPV and no intermediary. OpenAI's answer was that it had never authorized Robinhood to offer any exposure to its shares in the first place. That exchange is the heart of the whole matter, and it is why the question people usually ask, is this a regulated platform, turns out to be the wrong one. The question that actually decides whether you own anything is narrower and much harder to answer: did the company put its approval of this specific transfer in writing? If it did not, the wrapper does not matter. Direct or pooled, licensed or not, an unapproved transfer of private stock is void, and a token built on a void transfer is a token built on air.

Here is the part that reaches past one platform. The reason an ordinary person cannot simply buy a share of OpenAI or Anthropic is not that the technology to do it is missing. It is that shares in a private company are wrapped in restrictions the company itself controls. Nothing changes hands without the company's written consent, and the company's own register of shareholders, its cap table, is the only record that counts. You can put a share inside a token. You cannot put the company's permission inside a token. Owning a piece of a private company is not an object you hold; it is an entry the company agrees to make. A token can copy that entry, trade it, chart it and borrow against it, and the company can still say the entry was never valid in the first place, and be entirely within its rights.

This is not a new problem. It is a very old one that markets spent decades learning to solve. Before the 1930s, American markets were thick with paper that nobody could verify: certificates of dubious backing, and claims that changed hands faster than anyone could confirm them, including the bucket shops where people wagered on share prices without owning a single share. The securities laws written after the crash built the dull, essential machinery that answers one question: who owns this, and may they sell it. The machinery is invisible precisely because it works. A transfer agent keeps the official list of a company's owners and changes it only when a transfer is valid. A clearing system makes sure that when stock moves, the record of ownership moves with it. The cap table is not a marketing document; it is the legal answer to the question of who owns the company, and if it ever comes to a courtroom, the judge will look at that record and very little else. None of it is exciting, and all of it exists so that the thing you believe you bought is the thing you actually have. Tokenization, in its hurry, has talked itself most of the way back to the world before that machinery existed. The Anthropic token was a 1920s instrument wearing a 2026 interface: lively trading stacked on top of an ownership claim that no authority would confirm.

None of this means the people buying were foolish, or that the impulse behind it is wrong. The grievance underneath all of it is legitimate. In the United States you generally have to earn more than 200 thousand dollars a year, or hold more than a million in assets, before you are even allowed to buy into a private company, a line that is meant to protect small investors and in practice reserves the best early returns for people who are already wealthy. Meanwhile the companies on the far side of that line have become the main event of the decade. Anthropic's revenue, measured on an annual basis, climbed from around 9 billion dollars at the end of 2025 to roughly 30 billion by the spring, and Amazon has committed as much as 25 billion to it; the two firms together are valued near 1.8 trillion dollars. When both go public, probably before the end of this year, it will be one of the largest movements of private wealth into public hands in market history, and the strategist Tom Lee has already warned that the sheer supply of stock could be enough to jolt the broader market later in the year. People can watch all of this happen and are told they may not take part until the insiders have had their turn. A product that promises to open that door early is answering a real unfairness. And tokenization does have a legitimate end of the pool: properly authorized, fully custodied tokens for public stocks already trade, and the private companies run sanctioned sales of their own. OpenAI organized a board-approved tender last October in which more than 600 current and former staff sold 6.6 billion dollars of stock, with every transfer signed off by the company. The technology is not the fraud. The unauthorized wrapper around it is. The two companies were not closing the door on people cashing out; they were nailing shut the side doors while leaving the front one open.

Then, a few weeks later, the market did something almost refreshing in its honesty. On June 22, Coinbase began offering perpetual futures on OpenAI and Anthropic to its customers outside the United States. A perpetual future makes no pretense that you own anything. It is a bet on a number, settled in a stablecoin, that carries no shares and no rights of any kind, and Coinbase states this in plain language. The contracts trade around the clock and track an index of the company's estimated valuation rather than a share price, because there is no settled share price to track yet. Coinbase has run this play before: when it offered the same kind of contract on SpaceX, it simply converted the bet into an ordinary per-share contract the moment SpaceX filed to go public in June, and Binance rolled out its own versions in the same stretch. None of these pretend to be ownership, which is their main virtue and, for an inexperienced buyer, their main danger, because a leveraged bet on the guessed-at value of a company that will not publish real numbers for months is a trap of a different kind, and an honest label does not make the position safe. But it is at least the right label. So the same two companies now have two kinds of product trading on them at once: one that calls itself ownership and is not, and one that admits it is only a wager. The wager is the more honest of the two. Both exist for exactly the same reason, to give people exposure to a company they are not allowed to hold, and the only thing separating them is whether the label tells the truth.

The May crash exposed something that the coming wave of AI public offerings is about to make impossible to ignore. There is a difference between owning a thing and owning a claim on a thing that someone else is able to cancel. A share is the second kind. It lives on a register the company keeps, and the company can decide your slice of it is not there. So, on closer inspection, is almost everything people call an asset. The house you own is an entry in a public deed registry. The money in your bank account is not money you are holding; it is the bank's promise to pay you, and it stands behind the bank's other obligations if the bank goes down. Even gold in a vault is, on paper, a claim on the custodian who stores it. Each of these works because a chain of institutions agrees to honor a record, and each one can be frozen, lost, or denied if a link in that chain decides otherwise. Tokenization took the feeling of the rare exception, an object in your possession that is simply and finally yours and needs no one's permission, and wrapped that feeling around an ordinary permissioned claim. That mismatch is the entire story of the Anthropic token. It behaves like something you hold in your hand right up to the moment the issuer says otherwise, and at that moment it becomes a receipt for nothing. The only instruments where the token in your possession actually is the asset, where no one can post a sentence on a website and erase what you hold, are the ones with no issuer standing behind them who could.

This particular episode comes with an expiry date. When OpenAI and Anthropic finally list, the perpetual futures will convert into ordinary share contracts, an authorized market will open, and the tokens still standing will either be backed by real, recognized stock or be revealed as the claims on nothing they always were. But the lesson will outlast the headline, because the next asset to be tokenized will run straight into the same wall this one did. You can wrap a claim in a token and send it around the world in seconds. You cannot tokenize away the person who gets to decide the claim is void. So the right question to ask of anything sold to you as a piece of something is the plainest one in finance, and the May crash answered it in a single word. If the issuer says no, what do you actually hold? For most of what is being tokenized today, the answer is a receipt, and a receipt is worth precisely as much as the willingness of the other party to honor it. The list of assets that need no one's permission to stay yours is a short one, and the stock of a private company has never been on it.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

When the ledger forecloses

The newest idea in digital-asset lending is a loan the blockchain itself enforces. A standard proposed for the XRP Ledger this week would let institutions borrow against tokenized assets, with the chain holding the collateral and liquidating it automatically, no banker required. The pitch is efficiency. The catch is that every credit system ever built leans on a human who can pause or forbear in a falling market. Automated liquidation deletes that brake, and synchronized selling at machine speed turns a price wobble into a cascade. When MakerDAO tried this in 2020, a crash and a lagging price feed cleared loans at zero.

Everyone is printing a dollar now

With the GENIUS Act's full rules taking effect July 18, every large institution wants to issue its own dollar. Western Union has launched a stablecoin, Japan's three megabanks are building a yen one, JPMorgan is running dollar tokens on a public chain, and Bank of America, Citi and Wells Fargo have circled a joint coin. The prize is the float and the payment rails. The risk sits inside the banking system: Bank of America's chief warns up to six trillion dollars of deposits could drain out of banks and into stablecoins, and deposits are what banks lend against.

The clock on Q-Day

A quieter threat to bitcoin moved closer this year. Research from Google and Caltech sharply cut the computing power thought needed to break the cryptography that guards a wallet, pulling a once-distant "Q-Day" toward the end of the decade. Roughly 711 billion dollars sits in exposed addresses. The fix is the fight: a proposal to freeze the most vulnerable coins, many of them Satoshi's, has split developers between those who would act now and those who say breaking the rule that no one can touch another's coins is worse than the threat itself.

AI & Financial Infrastructure

The challengers to Nvidia arrive

Nvidia's grip on AI chips drew its first serious challengers this week. Qualcomm unveiled a data-center processor built for the low-power demands of AI agents, signed Meta as a customer, and bought a startup whose software rivals CUDA, the code moat that locks developers into Nvidia; its stock jumped 15 percent. Amazon said its own silicon now runs at a 20-billion-dollar annual rate, growing 100 percent a year. The threat is less to Nvidia's sales, still rising, than to the assumption that one company owns the future of computing.

The coding agents start charging

The hottest corner of AI is software that writes software, and it is starting to charge for it. Cognition, maker of the Devin coding agent, raised a billion dollars at a 26-billion-dollar valuation. OpenAI bought a startup to strengthen Codex, its rival tool, now past five million weekly users. GitHub is moving its Copilot to metered, pay-per-use billing. The shift from free demo to priced product is the real test: it will show whether anyone will pay enough to justify valuations built on the promise that agents replace engineers.

Who pays for the build

The bill for the AI build is starting to unsettle investors. Oracle, one of the most aggressive spenders, had its worst week on the market since the dot-com crash of 2001, on fears about how it is all being financed. Hyperscalers will spend roughly 600 billion dollars this year, increasingly funded by debt: Amazon's capital budget now exceeds its operating cash flow, sending it to the bond markets for the first time in years. The wager is that revenue arrives before the interest does.

Geopolitics & Markets

The tariff wall, rebuilt by other doors

America's tariff wall was struck down, and the administration is rebuilding it through other doors. In February the Supreme Court ruled the sweeping "Liberation Day" tariffs illegal, forcing the refund of some 166 billion dollars to more than 330,000 businesses. A 10 percent stopgap now expires around July 24 unless Congress acts, and the trade office has proposed a fresh set, justified on forced-labor grounds, that would touch 99 percent of imports, with a hearing July 7. Through all of it the effective tariff rate sits near its highest since the 1940s.

The quiet exit from the dollar

While markets watched stocks, central banks kept quietly leaving the dollar. A record 43 percent of them plan to add gold this year, and the BRICS bloc now holds 17.4 percent of the world's official gold reserves, up from 11.2 percent in 2019. The trigger was 2022, when the West froze Russia's reserves and taught every government that dollars held abroad can be switched off, while gold cannot. Even after a sharp pullback from January's record near 5,589 dollars an ounce, the buying has not stopped. A slow vote, in metal, against the reserve currency.

Running the neighborhood

Six months after US forces seized Venezuela's Nicolas Maduro and flew him to a New York jail, Washington effectively runs the country, and its oil is flowing again, more than a billion dollars' worth so far. The operation has hardened into a doctrine: great powers manage their own backyards. It exposed Russia, which could do nothing for an ally, and has rivals recalculating. The worry voiced from Kyiv to Taipei is the precedent, that a large country can now indict and remove the ruler of a smaller neighbor, and call it law enforcement.

The Week in Numbers

| Indicator | Reading |

|---|---|

| US bank deposits that could shift to stablecoins | $6T |

| Tariffs the Supreme Court ordered refunded | $166B |

| US effective tariff rate, highest since the 1940s | ~11.8% |

| Cognition's valuation after its new raise | $26B |

| Amazon's in-house AI-chip annual run rate | $20B |

| BRICS share of official gold reserves, from 11.2% in 2019 | 17.4% |

| Central banks planning to add gold this year, a record | 43% |

| Size of the stablecoin market the banks are chasing | $240B |

What to Watch This Week

| Date | Why it matters |

|---|---|

| July 7 | The US trade office hears its proposed forced-labor tariffs, which would touch 99 percent of imports. |

| July 18 | The GENIUS Act's full stablecoin rules take effect, opening the gate for bank-issued dollars. |

| July 24 | The 10 percent stopgap tariff expires unless Congress extends it, the cliff that sets the near-term rate. |

Keep reading — it’s free

Enter your email to unlock the full analysis and get Onramp’s research — the week’s essential bitcoin news, analysis, and data — delivered free. Unsubscribe anytime.