July 7, 2026 Weekly Market Brief

Glenn Cameron, CFA · Global Head of Onramp Institutional

The Fed's new leadership is betting that AI will push prices down, letting it cut rates before measured inflation falls. This week's brief sets that assumption against the data: the buildout is raising the prices households pay and borrowing so heavily it now competes with the Treasury for the same pool of savings. It closes on why bitcoin, the one asset in the picture asking no one for capital, is positioned for a repression that funds everyone else at the saver's expense. The Radar covers the UK's new digital-asset rulebook, bitcoin's looming BIP-110 flag day, the Open USD stablecoin coalition, Meta's move into renting compute, a cracking US jobs number, and an energy war, an Arctic scramble, and a strained NATO summit.

The Federal Reserve's new doctrine rests on a single assumption: artificial intelligence will push prices down, so the policy rate can be cut before measured inflation falls. So far the opposite is happening. The AI buildout is raising the prices households pay, and it is borrowing so heavily that it now competes with the Treasury for the same pool of savings. This week we set the assumption against the data.

The assumption doing the work

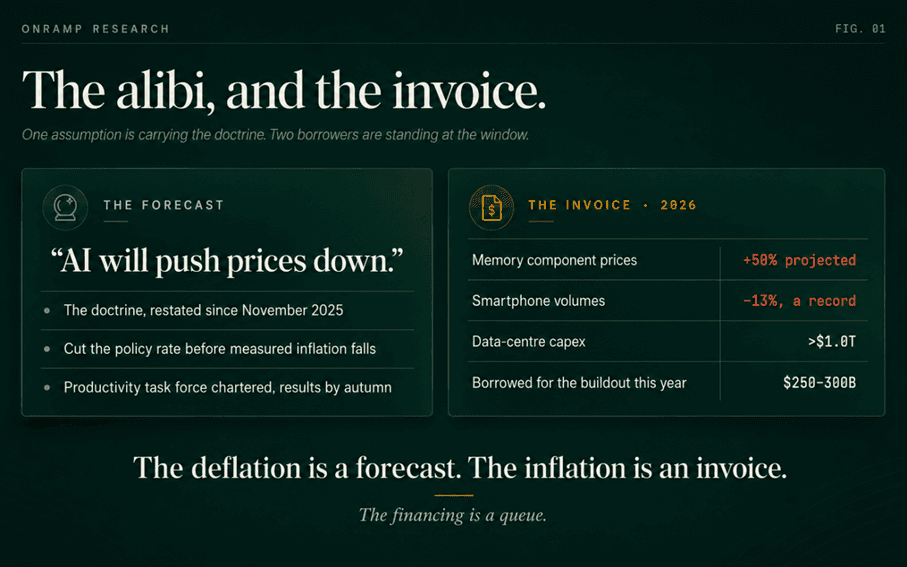

Kevin Warsh has made one economic claim more often than any other. In a November 2025 Wall Street Journal op-ed, at his April 21 confirmation hearing, and repeatedly since, he has argued that AI will be a significant deflationary force, raising productivity and strengthening American competitiveness. The claim matters because of what it permits. If prices are going to fall on their own, the Fed can cut rates before measured inflation falls. Our May 26 brief mapped the five mechanisms being assembled to absorb federal debt at suppressed real yields. The AI claim is what makes that policy defensible in public. It is the alibi.

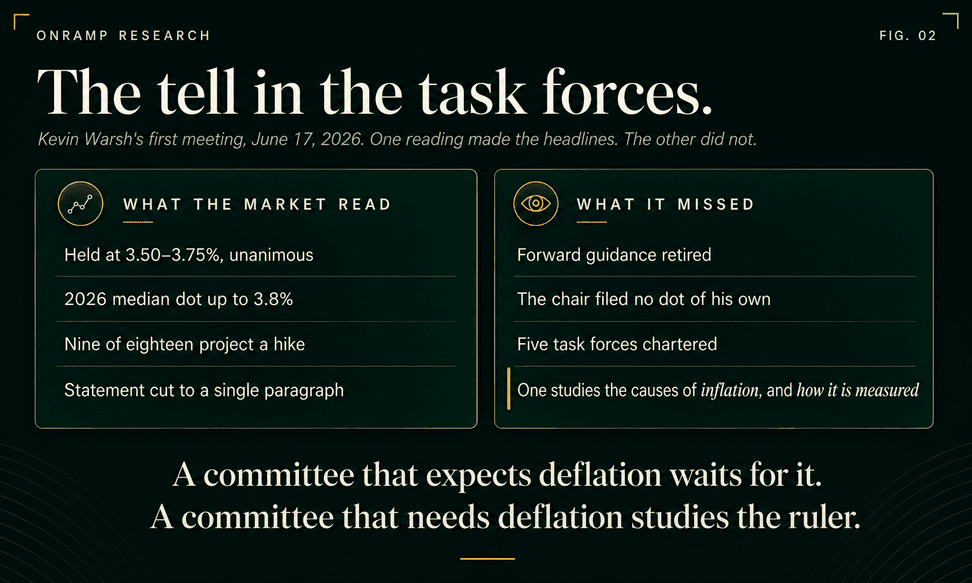

His first meeting as Chair, on June 17, read like the opposite of that agenda. The committee held the funds rate at 3.50 to 3.75 percent by a unanimous vote. The median projection for end-2026 rose from 3.4 percent in March to 3.8, and nine of eighteen participants pencilled in at least one hike. Warsh reaffirmed the 2 percent objective and told reporters the committee will deliver price stability. Markets took the hawkish reading and moved on.

However, as always, the devil is in the detail and it barely received one line in the press coverage and definitely deserves more attention. Warsh announced five task forces: on operations, communications, data sources, productivity and the labour market, and the causes of inflation. The inflation group, he said, will examine how inflation is measured. He declined to submit a rate projection of his own. The FOMC statement was cut to a single paragraph and forward guidance was dropped. Set against the May 26 architecture, none of this reads as hawkish. The first mechanism in that architecture was the doctrine. The second was measurement. The doctrine now runs the Fed, and the measurement of inflation review has a committee, a mandate, and a reporting date this autumn.

The distinction matters. A central bank that expects deflation can wait for the numbers to fall on their own. A central bank that needs deflation to justify a rate path it has already chosen starts reviewing how inflation is "measured". The one sentence of unqualified self-praise in the June statement was for Warsh's assumption itself: productivity growth and capital investment are strong. Which brings us to what that capital investment is doing to prices.

What the buildout is doing to prices

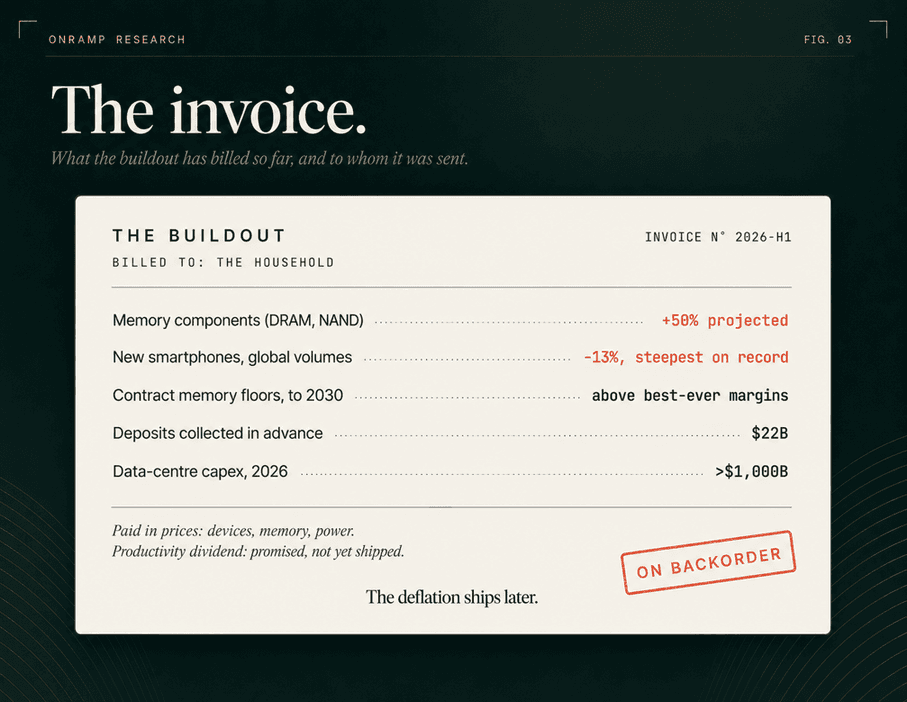

In late June, Micron's quarter reporting explained 2026. The company disclosed sixteen strategic customer agreements: five-year, take-or-pay contracts running from 2026 through 2030, with binding volumes and rigid pricing. Customers have posted $18 billion in cash deposits and $4 billion in letters of credit as guarantees, $22 billion of committed money. Each contract carries a price floor, and management set those floors at levels that would produce gross margins above the best quarter in the company's history. The guidance was blunt: memory demand will exceed supply beyond 2027. Capital spending rises from $27 billion this fiscal year to a projected $45 billion next year.

The consumer pays for this. IDC now forecasts the largest year-on-year decline in the history of the smartphone market, down 13 percent in 2026 to the lowest volumes in a decade, because memory producers redirected output to the data centres and handset makers could not get parts at workable prices. Deloitte's industry outlook projects price increases of roughly 50 percent for key memory components by the middle of the year. Dell'Oro raised its global data centre capex forecast above $1 trillion for 2026, and one of the reasons it gave was the rising cost of memory. The spending is now large enough to push up the price of its own inputs.

Electricity tells the same story. Microsoft has disclosed an $80 billion backlog of cloud orders it cannot fill because the power is not available. None of this disproves the eventual deflation. Every major technology buildout has followed the same sequence: it drives up the price of its inputs before it drives down the price of everything else. The railways made steel and land expensive before they made distance transport cheap. The real question is not whether the productivity gains will arrive. It is which phase policy is being set against, and who carries the monetary cost in between the phases.

In 2026 the household's experience of AI is a more expensive phone, a more expensive laptop, a higher power bill, and if Warsh's doctrine holds, a lower return on savings, all justified by deflation that has not shown up yet. The forecast of deflation may prove right over the long term, but the price increases are already here.

The second borrower

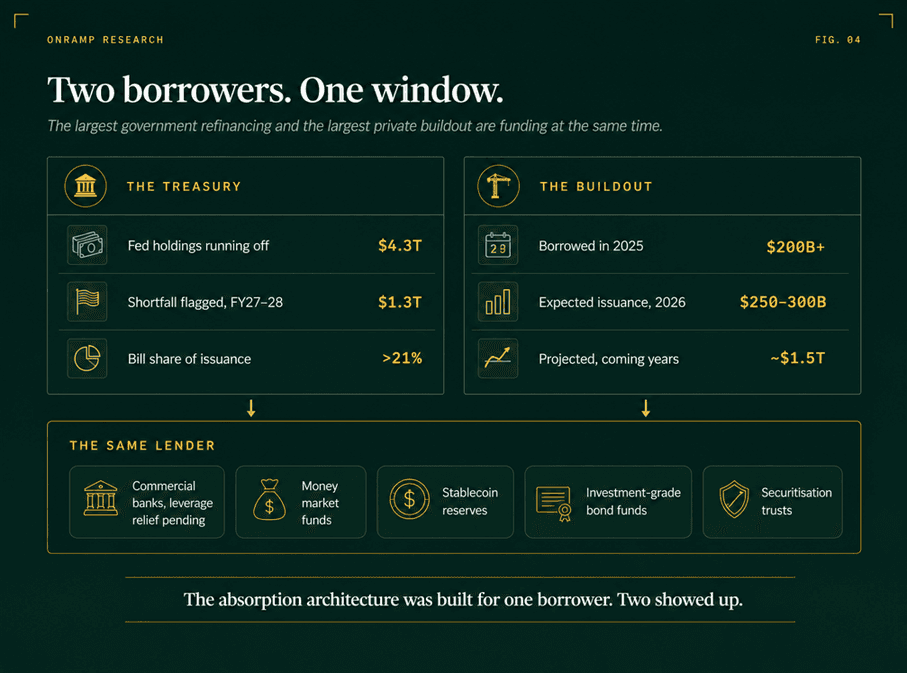

The buildout has outgrown the cash that funds it. Capital spending at the large platforms, before dividends and buybacks, reached roughly 94 percent of operating cash flow in 2025 by one Wall Street estimate, up eighteen points in a year. The marginal dollar is now borrowed. AI-related companies and projects raised at least $200 billion in the debt markets last year, a figure widely regarded as an undercount because many of the deals were private. Morgan Stanley expects $250 to $300 billion of issuance from the hyperscalers and their joint ventures in 2026 alone. Over the next few years, Morgan Stanley and J.P. Morgan both arrive at roughly $1.5 trillion of new technology debt, and J.P. Morgan notes that every market, public and private, will need to be tapped to fund it. Securitisation of data centres is projected at $30 to $40 billion a year. Goldman's baseline estimate for the full buildout is near $7.6 trillion of capital between now and 2031.

Set that against the US government's borrowing calendar. From the May 26 brief: $4.3 trillion of Treasuries rolling off the Federal Reserve's balance sheet into private hands for as long as Warsh decides to shrink the Fed's balance sheet; a $1.3 trillion funding shortfall flagged by the Treasury Borrowing Advisory Committee for fiscal 2027 and 2028; bills already above 21 percent of issuance. The buyers on the other side of both calendars are the same institutions: investment-grade bond funds, commercial banks whose leverage constraint is being relaxed, money market funds, and stablecoin issuers. The 2026 capital market is being asked to finance the largest peacetime government refinancing and the largest private infrastructure programme in history at the same time, out of the same pool of savings.

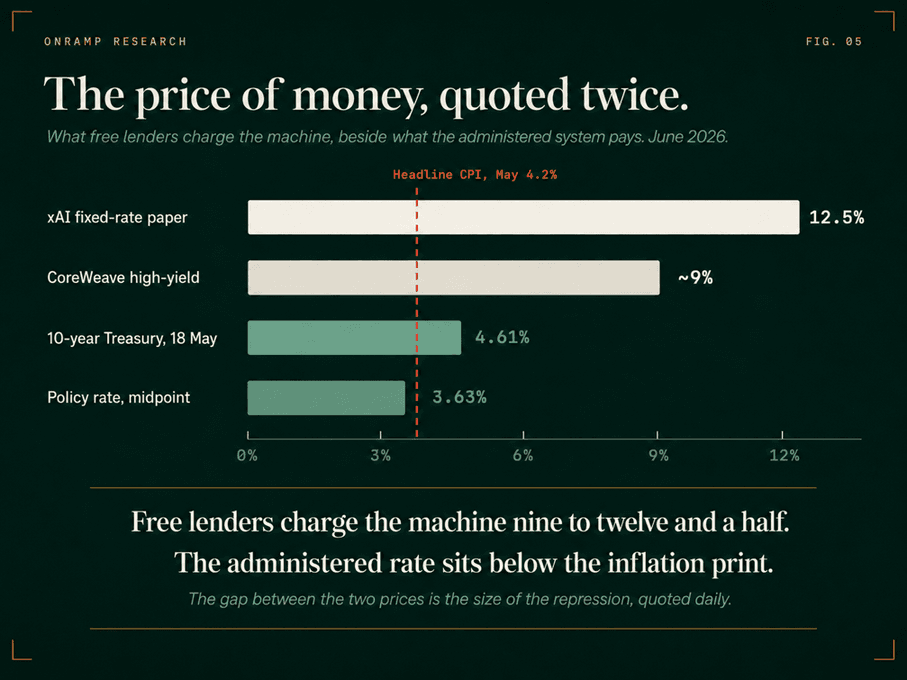

The market has already shown what it charges when it can set the price freely. xAI's fixed-rate debt carries a 12.5 percent coupon. CoreWeave borrowed at close to 9 percent. The administered side looks very different: the most recent CPI print of 4.2 percent for May, and the 10-year Treasury stood at 4.46 percent at the July 2 close, a real yield of roughly a quarter of a point against the same print.

One borrowing market is quoting two very different prices for money, nearly nine points apart at the extremes. That gap explains why the absorption architecture has to work through regulation rather than choice. No saver would voluntarily hold the capped instrument while the uncapped one exists, so the plumbing directs them: leverage relief points the banks at Treasuries, the GENIUS Act points stablecoin reserves at bills, and the shift toward short maturities points the money market funds at the front end.

This is where the two stories we are comparing meet. The AI buildout is not a side story to the financial repression architecture. It is the competing bid for the same savings, and it is this competing bid that is the reason the repression architecture is being constructed. Warsh's deflation doctrine is what allows both borrowers to be financed at once: it justifies the lower policy rate that keeps the Treasury's cost of funds down, while the AI borrowers pay whatever the market demands. Only one of the two pays a market rate.

The precedent

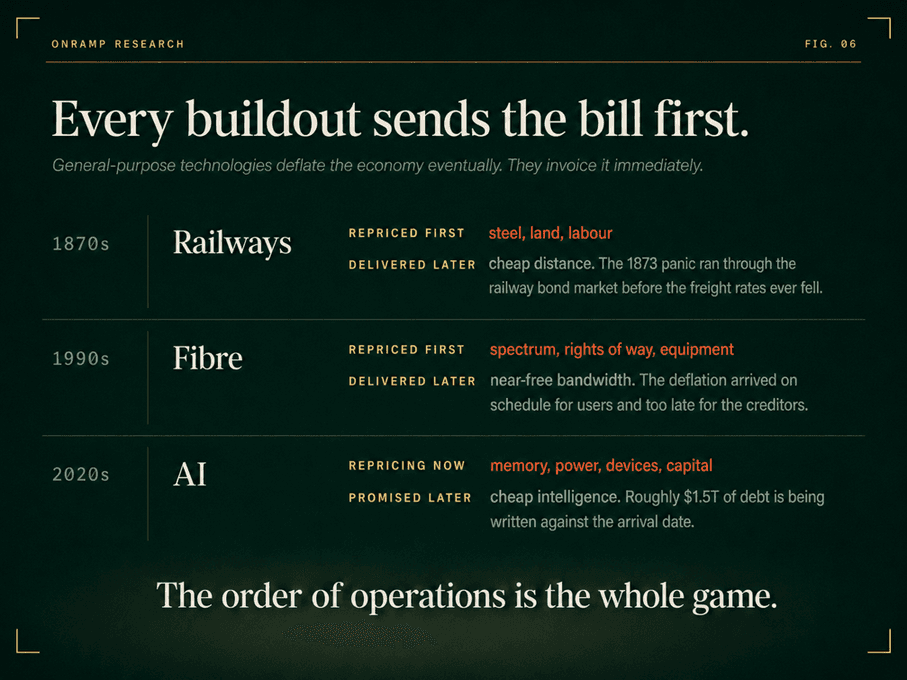

The pattern of costs arriving before benefits is as old as industrial capitalism. The railway boom drove up steel, land and labour years before it brought down the cost of moving goods, and the panic of 1873 went through the railway bond market long before freight rates reached their eventual lows. The fibre boom of the 1990s delivered exactly the bandwidth deflation it promised, and the creditors who financed it went through default and restructuring before the benefit reached the wider economy. In both cases the technology worked. The timing ruined the lenders.

The 2026 version has one feature neither precedent had: the US government is borrowing at an extraordinary rate at the same time. The 1946 to 1974 repression our May 26 weekly brief traced worked partly because the private sector was deleveraging while the government's debt was being inflated away. Savings had nowhere else to go. The 2026 version asks the state's absorption machinery to work while the private sector levers up into a single technology at 9 to 12.5 percent. That is the gap in the precedent, and it is why Warsh's inflation measurement task force matters more than the dot plot. If the deflation is late and yields still have to be held down, the adjustment of course will happen in how inflation is measured. How convenient!!

If the revenue is late

The counterarguments deserve a fair hearing. The platforms doing most of the borrowing are the most profitable companies in history, and much of the spending is still funded from cash. The take-or-pay contracts make this cycle different from the fibre glut: capacity is being sold before it is built, not after. The Fed's own projections show inflation falling to 2.3 percent next year. All of that may hold.

But June showed how the market behaves when the assumption merely wobbles. Broadcom reported record AI revenue, up 143 percent, and held its 2027 outlook rather than raising it. Roughly $1.3 trillion came off the global chip complex in a single session and the Nasdaq fell 4 percent. Three weeks later a second selloff took 10 percent off Korea's main index in a day and tripped its circuit breaker, before Micron's results turned the market around. None of this followed an earnings miss. It followed next year's guidance that failed to deliver an expected acceleration. The people building these systems are candid about the stakes. Anthropic's chief executive has warned that a single year of missed revenue projections could bankrupt a frontier lab, at a valuation near $965 billion, and OpenAI is reported to be weighing a delay to its listing because of demand concerns at a $1 trillion valuation. If the revenue disappoints, the debt does not go away. It sits in the same banks, bond funds and securitisation trusts that the Treasury architecture is filling with government paper. Two absorption programmes are running through one set of balance sheets.

Where this leaves bitcoin

Let me start with an honest observation. The buildout has been drawing capital away from bitcoin as well. The US spot funds just posted their worst month since launch, with $4.5 billion of June outflows, and bitcoin trades a little more than half below its October high while AI borrowers pay 12.5 percent for money. The buildout has outbid everyone this year: households for components, the Treasury for savings, and bitcoin for investment flows.

That leaves three crowded parties, and policy will rescue exactly one of them. The financial repression architecture we described in our May 26 weekly brief is the rescue: the Treasury gets funded at a suppressed rate, and the household pays for it through returns held below inflation. Bitcoin is the one asset in this picture that is not asking anyone for capital and does not depend on the deflation arriving on time. Fixed supply, no coupon to defend, no revenue forecast to hit. Holding it is not a bet that AI fails. It is a claim on what happens to money if the productivity gains arrive later than the policy that was justified by them. In the last repression, the assets that performed were the ones whose supply could not be expanded to absorb the flows. That does not change because there are two borrowers.

What to watch

The task force reports. Warsh wants most of them concluded by the autumn. Any change to how inflation is measured will matter more than any single rate decision.

The July CPI internals. Core goods will show whether memory costs are passing through into device prices. Electricity prices will show the grid supply demand effect on inflation.

The quarterly refunding, late July. A treasury bill share of total issuance above 22 or 23 percent confirms the shift toward short maturities is operational.

The AI issuance calendar. Hyperscaler investment-grade deals, data centre securitisation volumes, and secondary spreads on the highest-coupon names. Widening spreads would mean the private borrower is starting to lose access.

The listings. OpenAI and Anthropic going public would put the largest supply of new paper in years in front of the same investors.

Micron's floors. Whether contract memory prices hold at floors set above prior peak margins. If they hold, that is five years of hardware inflation agreed in advance.

Conclusion

Every component of this story is public. Warsh's op-ed on AI driven deflation, the transcript of him selling the same doctrine is on the Senate transcript, the task forces were announced from the podium, the take-or-pay contracts are in a press release, the issuance projections are in bank research, and the refinancing calendar is in the TBAC minutes. What has not been done, in any analysis I have seen, is to put them all together.

The correct version of the Warsh doctrine says AI will lower prices later. The data says it is raising them now. The financing shows the state and the AI buildout borrowing from the same lenders, and the financial repression architecture decides which of them gets funded at a rate no free market lender would accept. The savers who fund it carry the difference.

If the productivity gains arrive on schedule, Warsh's doctrine will look prescient. If they are late, the rates will be held down anyway, and the new "better measurement" of inflation will do the reconciling. Either way, Warsh's assumption is carrying more weight than any number in any projection.

Sources: Federal Reserve FOMC statement, Summary of Economic Projections and press conference transcript, June 17, 2026; Warsh confirmation testimony, April 21, 2026, and Wall Street Journal op-ed, November 2025; Micron fiscal Q3 2026 results and public reporting on its strategic customer agreements; IDC smartphone forecasts and Deloitte's 2026 semiconductor outlook as reported; Dell'Oro Group data centre capex report, June 2026; Bloomberg reporting on AI debt issuance with Morgan Stanley and J.P. Morgan projections; Goldman Sachs Global Institute build-out estimates, 2026; TBAC minutes, May 2026; public reporting on xAI and CoreWeave debt terms, the June 2026 equity drawdowns, OpenAI listing timing, and US spot bitcoin fund flows. Figures approximate where noted; projections are the cited institutions' own.

The Radar

What matters this week across digital assets, AI, and global markets.

Digital Assets & Regulation

The UK writes its rulebook

Britain has set out the rules for its digital-asset market, and the bet is openness. On June 30 the Financial Conduct Authority published its final framework, letting overseas venues serve UK customers through locally authorized branches and allowing non-UK stablecoins to circulate, a deliberate contrast with Europe's more walled-off regime. Firms face capital and market-abuse rules, and retail customers gain access to the ombudsman for the first time. The gaps are real: which foreign jurisdictions qualify is undefined, DeFi is unresolved, and the regime does not bind until October 2027.

Bitcoin's data war nears a flag day

A slow-burning fight over what belongs on the bitcoin blockchain is coming to a head. Last October the Bitcoin Core v30 software lifted the cap on arbitrary data in a transaction from 83 bytes to 100,000, and the backlash hardened into BIP-110, a proposal to force the limit back for a year. Miner support fell short, so backers are pushing a user-activated route: around early August, opted-in nodes begin rejecting non-compliant blocks, targeting activation near September 1. With only a small share of nodes enforcing it, Adam Back and Jameson Lopp warn the attempt could split the chain.

A coalition comes for the stablecoin giants

The stablecoin business just came under attack from within. On June 30 a group of 140-plus companies, Visa, Mastercard, Stripe, Coinbase and BlackRock among them, unveiled Open USD, a dollar token that costs nothing to mint or redeem and shares the interest on its reserves with the firms that use it. That undercuts the model, where issuers like Circle keep the yield on the Treasuries behind the coin, and Circle's shares fell more than 17 percent. The fight is now over who keeps the yield, not who issues the dollar.

AI & Financial Infrastructure

Meta turns landlord

Meta wants to rent out its AI hardware. Bloomberg reported July 1 that it is building a cloud business, Meta Compute, to sell its spare data-center capacity and its models, competing with Amazon, Microsoft and Google. Meta has committed roughly 183 billion dollars to AI infrastructure but earns little from its own models, so renting compute, as CoreWeave does, is one way to make the spend pay. The winners may be whoever owns the data centers, not whoever has the best model.

The jobs number cracks

The AI build is colliding with the job market. US employers added just 57,000 jobs in June, about half what forecasters expected and the weakest in four months. Unemployment fell to 4.2 percent, but only because people left the workforce, not because hiring was strong. How much of the slowdown is AI is the live debate: tech firms are cutting staff and automating entry-level office work, though June's losses were concentrated in seasonal leisure and hospitality. Either way, hiring has stalled.

Washington reaches for the frontier

The US government wants to look inside the most powerful AI models before the public does. An executive order signed June 2 sets up a voluntary process, due by August 1, under which developers of designated "frontier" models would give agencies up to 30 days' access before release to probe them for cyber weaknesses. It stops short of any license or approval. Supporters call it light-touch next to Europe's rules; skeptics say such "voluntary" cooperation tends to become the norm. Either way, the state is now inside the lab.

Geopolitics & Markets

Ukraine's energy war

Ukraine has turned its war on Russia into a war on Russian fuel. Kyiv's home-built drones have hit most of Russia's largest refineries and, by its own count, knocked out roughly 42 percent of refining capacity, triggering a fuel crisis, rationing across dozens of regions and Moscow importing gasoline. Russia answered again overnight, striking 34 sites across Ukraine and cutting power in several regions, days after an attack that killed 30 in Kyiv. Neither side is relenting: as Ukraine chokes the fuel funding the war, Russia escalates its strikes on Ukrainian cities. A mutual war on infrastructure, with no ceiling in sight.

The scramble for the Arctic

The Arctic is turning into contested ground, and it is straining an old alliance. Denmark barred US officials from its long-running Fourth of July celebration this year, a pointed snub after Washington's repeated push to control Greenland, the Danish territory Trump has said America needs. Melting ice is opening new sea lanes and exposing minerals; Russia has rebuilt its northern bases and China calls itself a "near-Arctic" power. Beneath the theatrics is a harder claim, that strength, not treaties, decides who holds the top of the map. Allies must plan around it.

NATO meets under strain

NATO's leaders gather in Ankara this week with the alliance more divided than it has been in years. On the table is roughly 80 billion dollars in aid for Ukraine, alongside fresh pressure over spending and the shadow of a US relationship allies no longer take for granted, from tariff threats to the fight over Greenland. Trump, fresh from a nearly 90-minute call with Putin, is due to meet Zelensky. The real question is not any single pledge but whether the alliance still holds together when its most powerful member treats it as optional.

The Week in Numbers

| Indicator | Reading |

|---|---|

| Bitcoin's new data-carrier limit, up from 83; BIP-110 would reverse it | 100,000 bytes |

| Bitcoin nodes now running Knots, the reversal camp | ~23% |

| Circle's stock drop after the Open USD launch | -17% |

| Size of the stablecoin market Open USD is chasing | ~$300B |

| US jobs added in June, about half what was expected | 57,000 |

| Meta's committed AI-infrastructure spend | $183B |

| Russian refining capacity Ukraine says it has knocked out | ~42% |

| Denmark's annual subsidy to Greenland, now a flashpoint | $630M |

What to Watch This Week

| Date | Why it matters |

|---|---|

| July 7-8 | NATO's summit in Ankara, where allies are set to pledge roughly 80 billion dollars in Ukraine aid and Trump will meet Zelensky. |

| This week | Whether Russia's intensifying strikes harden or stall Trump's renewed outreach to Putin. |

| July 17 | The FCA's webinar on Britain's new digital-asset rulebook, as pre-application support for firms opens. |

| Early Aug | BIP-110's mandatory-signaling window, the flag day critics warn could split the bitcoin network. |

| Early Aug | The July jobs report, a test of whether June's hiring slump was a blip or a trend. |

Keep reading — it’s free

Enter your email to unlock the full analysis and get Onramp’s research — the week’s essential bitcoin news, analysis, and data — delivered free. Unsubscribe anytime.