Built on Sand

Michael Tanguma | Chief Executive Officer

Five Layers of Risk

Five Foundational Flaws

Why Digital Credit Collapses From the Ground Up

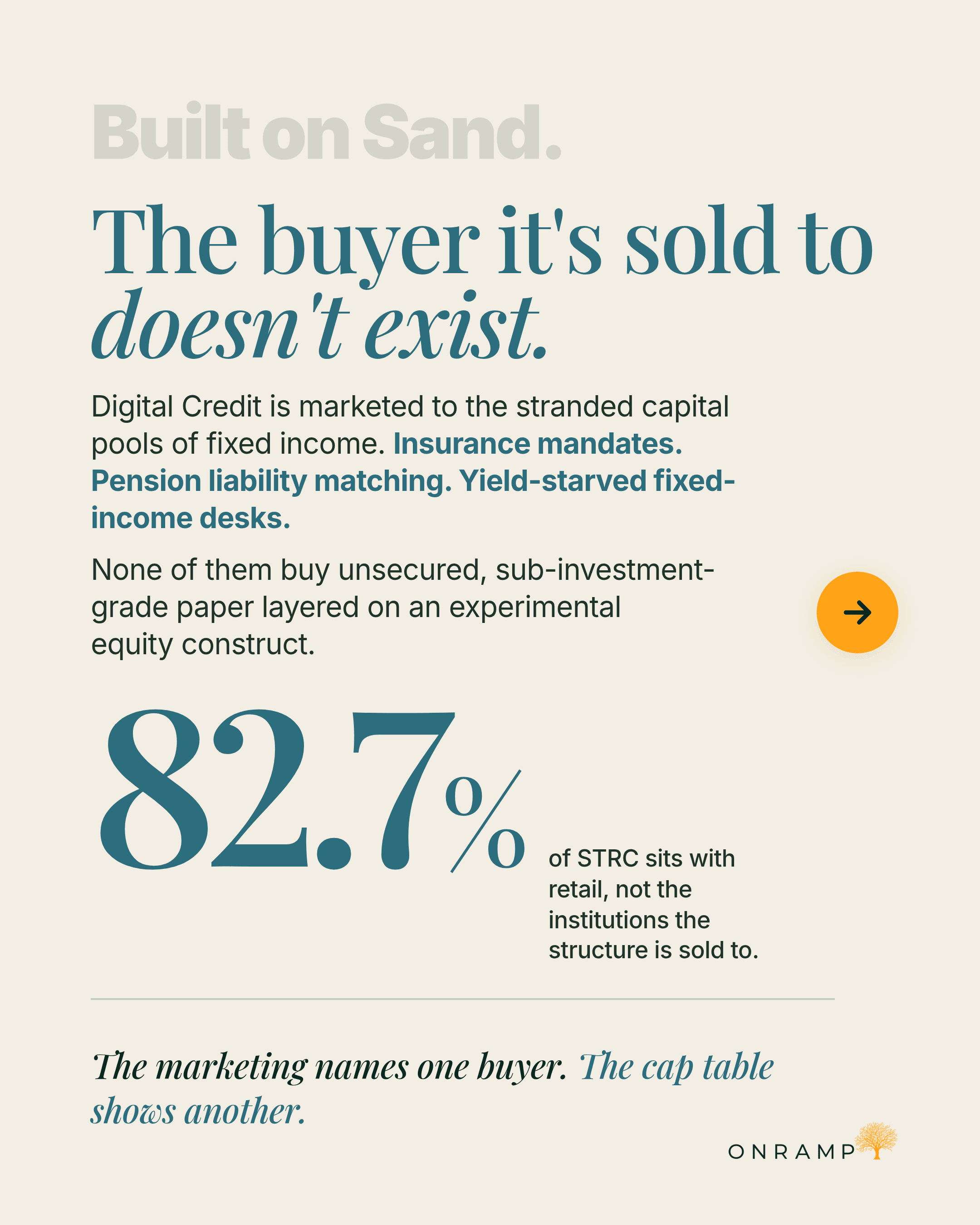

82% of STRC is held by retail. The product is being sold as a money-market-like instrument backed by bitcoin, paying 11.5% tax-free.

None of those words survives contact with the structure long term.

STRC is a perpetual preferred equity. It has no maturity. It has no bitcoin pledged behind it. The 11.5% is discretionary and has only ever moved up because the price keeps slipping below par. The "tax-free" classification is the IRS confirming Strategy has no earnings to distribute. The "money-market-like" framing applies to an instrument that has none of the properties that constitute a money market fund.

The most sophisticated financial engineering on the planet cannot rescue what's underneath. And once you start examining the foundation, every claim made on top of it begins to come apart.

The structure has five layers of risk. They sit on top of each other in a specific order. The order matters.

Layer 1: The Foundation Is Custody

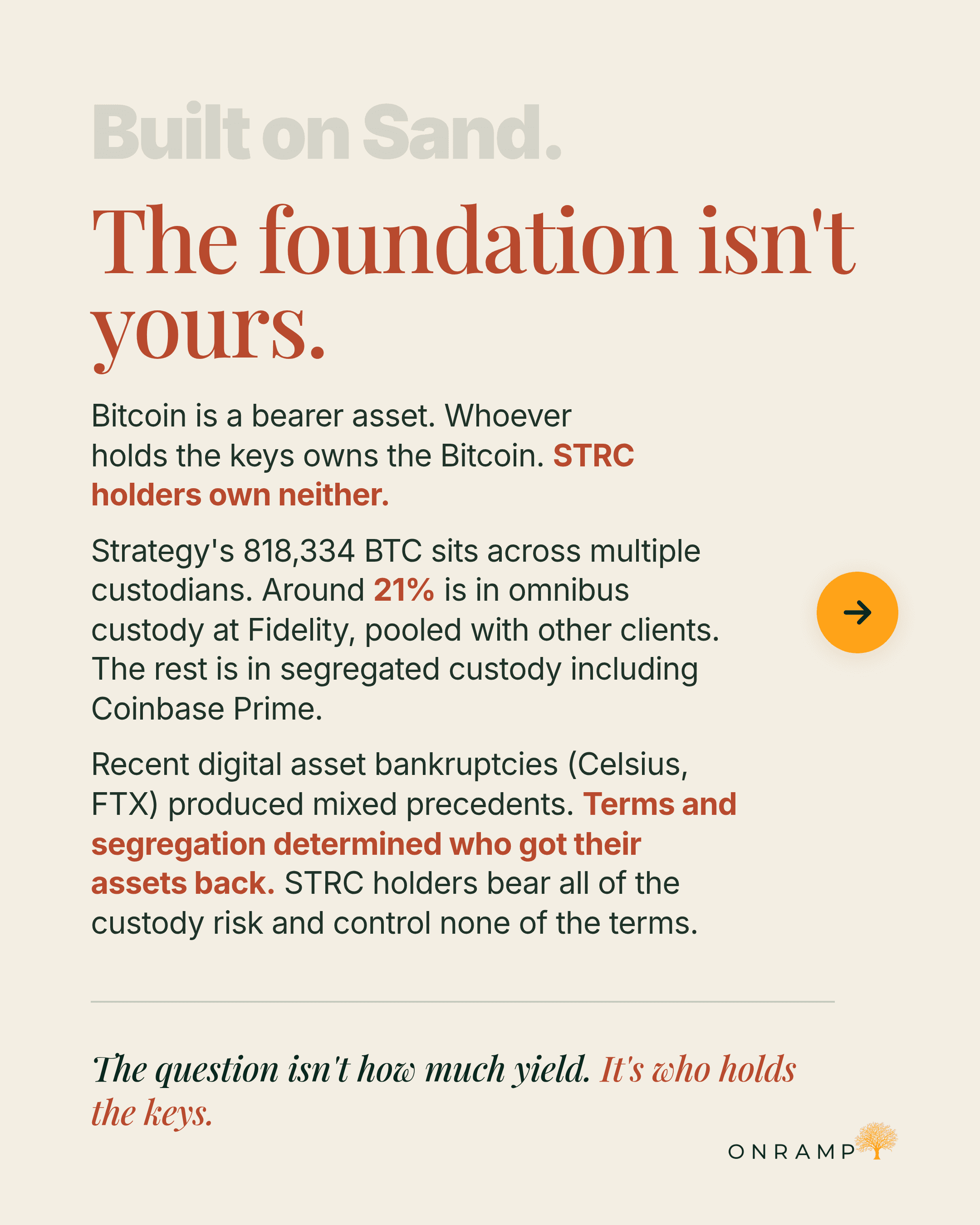

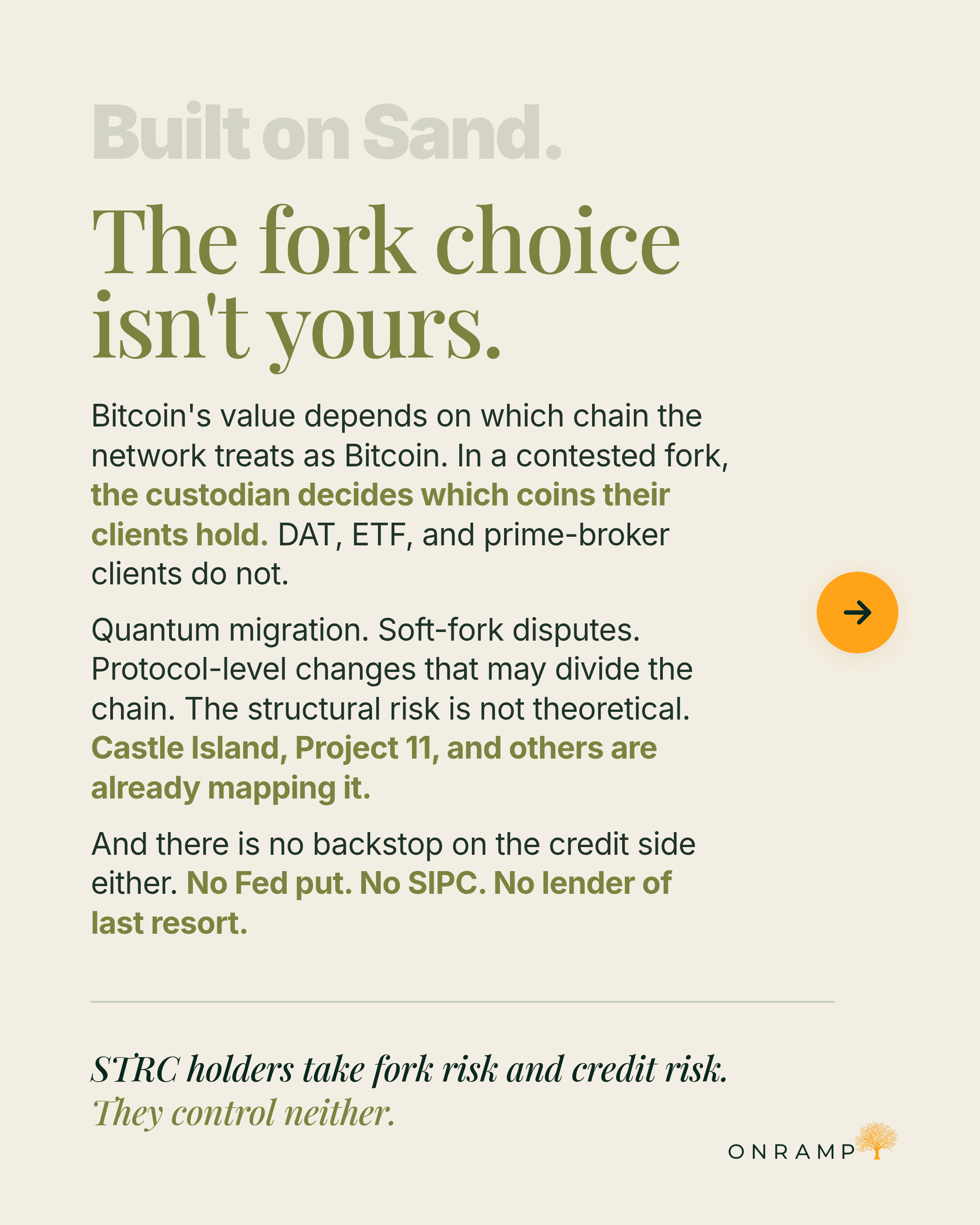

A bearer instrument is something whose ownership is determined by possession itself. No registry. No permission. No counterparty whose performance is necessary for the asset to remain whole. Bitcoin is a digital bearer asset. Whoever holds the keys owns the bitcoin.

Every other property bitcoin is known for descends from this one. The fixed supply matters because no counterparty can dilute it. The portability matters because no intermediary can block it. The censorship resistance matters because no jurisdiction can override it. Strip the bearer property and bitcoin becomes indistinguishable from any other database entry maintained by any other institution.

The wrapper industry has spent the last several years reintroducing intermediation into the holding of bitcoin while keeping some amount of price exposure intact. Digital Credit is the most aggressive iteration of that project. And every product in the category presupposes that custody is a settled question.

It is not.

Strategy holds 818,334 bitcoin. Where it sits, who holds the keys, what jurisdiction governs the accounts, and what happens if a custodian has a bad day, are the ground the entire structure stands on. None of these questions have settled answers. None of them are being raised in the conversations where STRC is being sold.

The best architect, the best structural engineer, and the best general contractor will refuse to build on a foundation nobody has verified. STRC is the skyscraper. Custody is the foundation. The foundation has not been poured.

This is not specific to STRC. The spot ETFs hold the underlying through the same set of custodians, in the same legal regimes, with the same untested precedent. The DAT complex sits on the same ground. What changes from product to product is the number of layers above the foundation. What does not change is the foundation itself.

Layer 2: The Construct Itself Has Never Existed Before

Closed-end funds have existed for a century. We know how they behave. We know they trade at a discount to NAV unless there's an active reason for the premium. We know what happens when the manager stops adding value. The economics are settled.

A Digital Asset Treasury company, considered honestly, is a closed-end fund. It owns a basket of assets, in this case bitcoin. It is run by a team taking salaries. It carries leakage in the form of management costs, debt service, and dividend obligations. Its shares trade at a premium or discount to net asset value.

But STRC is not a closed-end fund. It is a perpetual preferred sitting on top of a closed-end fund, sitting on top of an operating business, sitting on top of $8.2 billion in senior debt, sitting on top of bitcoin. And here's what nobody says out loud. This construct has never existed before. There is no historical precedent for a perpetual preferred backed by a digital bearer asset, funded through at-the-market issuance of common equity, layered on top of an operating business that does not generate enough revenue to cover the dividends.

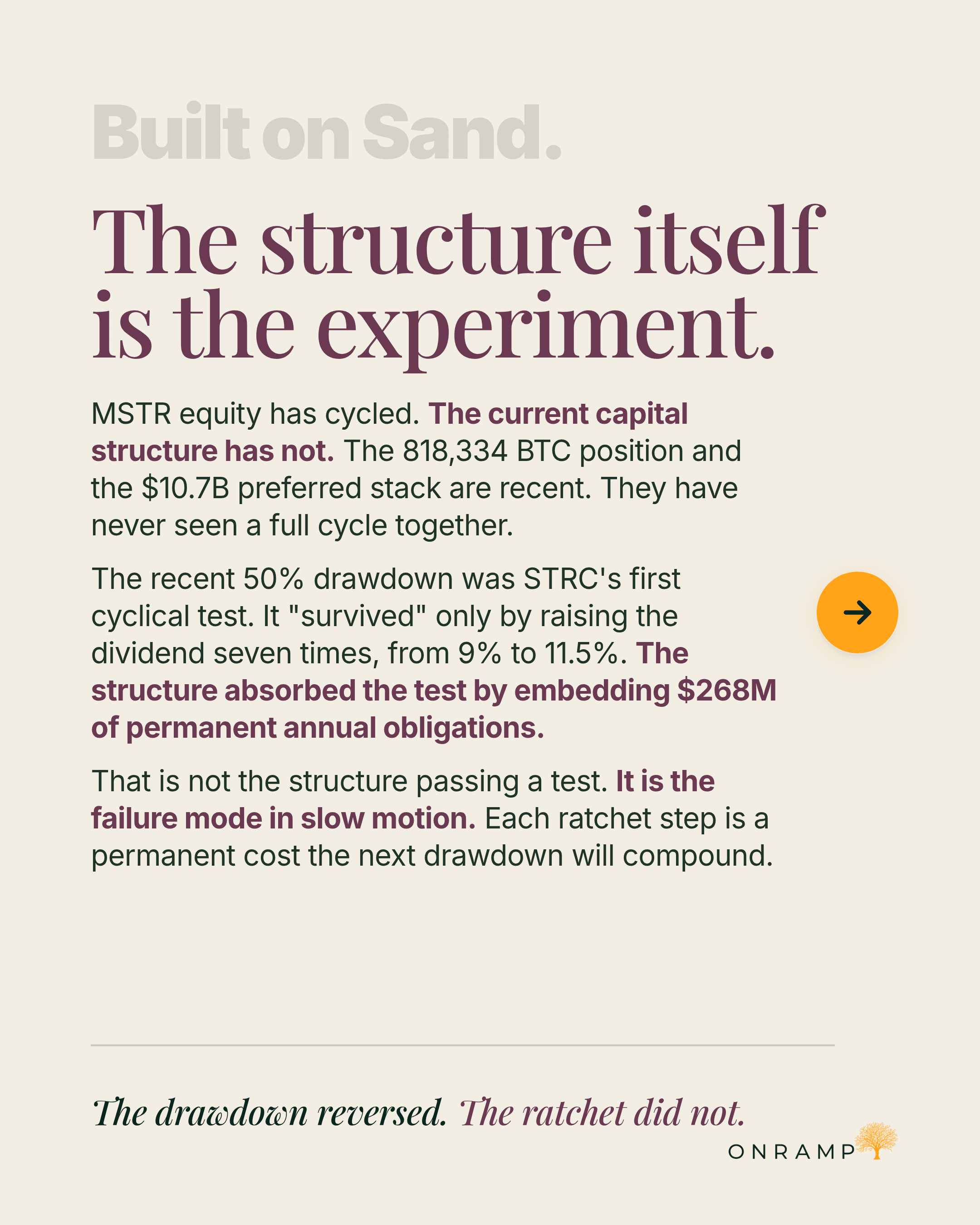

MSTR equity has gone through a full bitcoin cycle. The current capital structure has not. The 818,334 bitcoin position and the $10.7 billion preferred stack are recent. They have never been tested together through a full cycle.

The recent 50% bitcoin drawdown was STRC's first cyclical test. The structure absorbed the test only by raising the dividend seven times, from 9% to 11.5%, embedding $268 million of permanent annual obligations in the process. The bitcoin drawdown has reversed. The ratchet did not. The structure now faces every future drawdown with permanent costs the last drawdown forced it to accept.

A capital structure that survives volatility only by adding permanent obligations is a structure with a finite number of cycles in it. STRC has consumed one of them and has no mechanism for recovering the cost. That is not a credit profile. That is a slow-motion insolvency that has not named itself yet.

Layer 3: Governance Sits at Board Discretion

This is the layer almost nobody discusses. It is also where the holder has the least protection.

Read the prospectus. The board can reduce the dividend. The board can suspend the dividend. The board can defer the dividend. Redemption is at the company's sole discretion. There is no maturity date. There is no covenant that protects the holder from any of these outcomes. The 11.5% rate is, in the company's own language, "subject to monthly adjustment and may be significantly lower."

Holders are buying a product whose every economic feature is exposed to discretionary decisions made by a management team whose primary stated mission is to acquire more bitcoin. When the dividend obligation conflicts with the bitcoin acquisition strategy, which one will the board prioritize? The prospectus tells you. Every option in a stress scenario is theirs.

This is not theoretical. This is contractual. A bond holder has covenants. An investment-grade credit holder has indenture protections. STRC holders have a perpetual claim on a corporation that retains every option to modify the terms of the claim at its own discretion. The 11.5% is a posture. The structure is the actual instrument.

Layer 4: The Buyer the Marketing Names Cannot Exist

Here is the part I have thought about most. Take the two realistic buyers and run the math.

A buyer with meaningful capital does not need 11.5% from a leveraged wrapper to round out their cash flow. They already have Treasuries, money markets, investment-grade credit, and a portfolio that throws off income. The reason to hold bitcoin in this case is precisely that the asset is not being relied on for current cash. The holder can withstand the volatility because nothing day-to-day depends on the asset's near-term price. Buying STRC trades a clean position in a bearer asset for an unsecured claim on a corporation, in exchange for yield that was not needed and counterparty risk that previously did not exist.

A buyer who depends on the income to live cannot afford a nine-month-old preferred with a discretionary dividend, no maturity date, and four layers of claims sitting above it. The rational instrument for that buyer is a 5% coupon from a money market or an investment-grade bond. The yield is lower on paper. But the entire reason the income-dependent buyer exists as a category is that they cannot be wrong about the return of capital.

The product does not improve the position of the buyer who has capital. And it does not protect the buyer who needs the income. The data on who actually owns it confirms what the analysis implies. 82% retail. Not the institutions or family offices the marketing was rhetorically built for. Individuals who, in most cases, have not been given the full picture of risk.

The institutional buyer the marketing names is not just empirically absent. The buyer is logically impossible.

Pension liability matching, insurance mandates, and yield-starved fixed-income desks cannot underwrite the credit profile of an unsecured perpetual preferred layered on a bitcoin treasury without structurally understanding bitcoin first. And any institution that does the work to understand bitcoin reaches the same conclusion every time. The rational allocation is to the spot asset, with clean custody, sized to portfolio risk tolerance.

The institution that has done the work does not buy STRC. The institution that has not done the work cannot underwrite STRC. The named buyer cannot exist as both informed and rational at the same time.

So what is left. The buyer who actually exists is the buyer who has not yet figured out that volatility is the feature of the asset, not a flaw to be engineered around. People with speculative bitcoin exposure looking for what they think is a “risk-free” way to diversify. They end up buying a structurally riskier instrument than the bitcoin they already hold.

That misinformation is not incidental to the trade. The trade depends on it.

A trade with no rational institutional buyer ends up where the friction is lowest. The friction is lowest where the buyer is least equipped to evaluate what they are buying. Reaching that buyer required describing STRC in language that fits instruments it has nothing in common with.

"Backed by bitcoin" implies collateralization. STRC holders have no direct lien on any bitcoin. They hold an unsecured preferred equity interest in a corporation that happens to own bitcoin. The $8.2 billion in senior creditors are paid first.

"Money-market-like" describes an instrument that has none of the properties that make a money market what it is. Money markets are short-duration, principal-stable, and held in segregated, claim-clear arrangements. STRC is perpetual, pays a discretionary dividend, has no maturity, and offers no obligation on the issuer to ever return the holder's $100. The only exit is the secondary market at whatever price it trades.

"Tax-free" is the IRS confirming Strategy has no earnings to distribute. Every dollar received reduces cost basis. After 8.7 years, basis hits zero and every subsequent dollar becomes immediately taxable as a capital gain. The effective after-tax yield is closer to 8.8%, not 11.5%.

"Low volatility" describes the chart, not the instrument. The apparent stability is manufactured by seven consecutive defensive dividend raises, each one a response to capital flight. The Sharpe looks excellent until the tail event arrives. The structure embeds short volatility. It pays well in calm conditions and breaks badly when conditions change.

The marketing language is doing the work the structure cannot. It borrows the vocabulary of instruments that are clear, segregated, principal-stable, and risk-bounded, and applies it to an instrument that is opaque, subordinated, principal-permanent, and risk-unbounded. The buyers receiving this language are the buyers least equipped to test it. The language is calibrated to that fact.

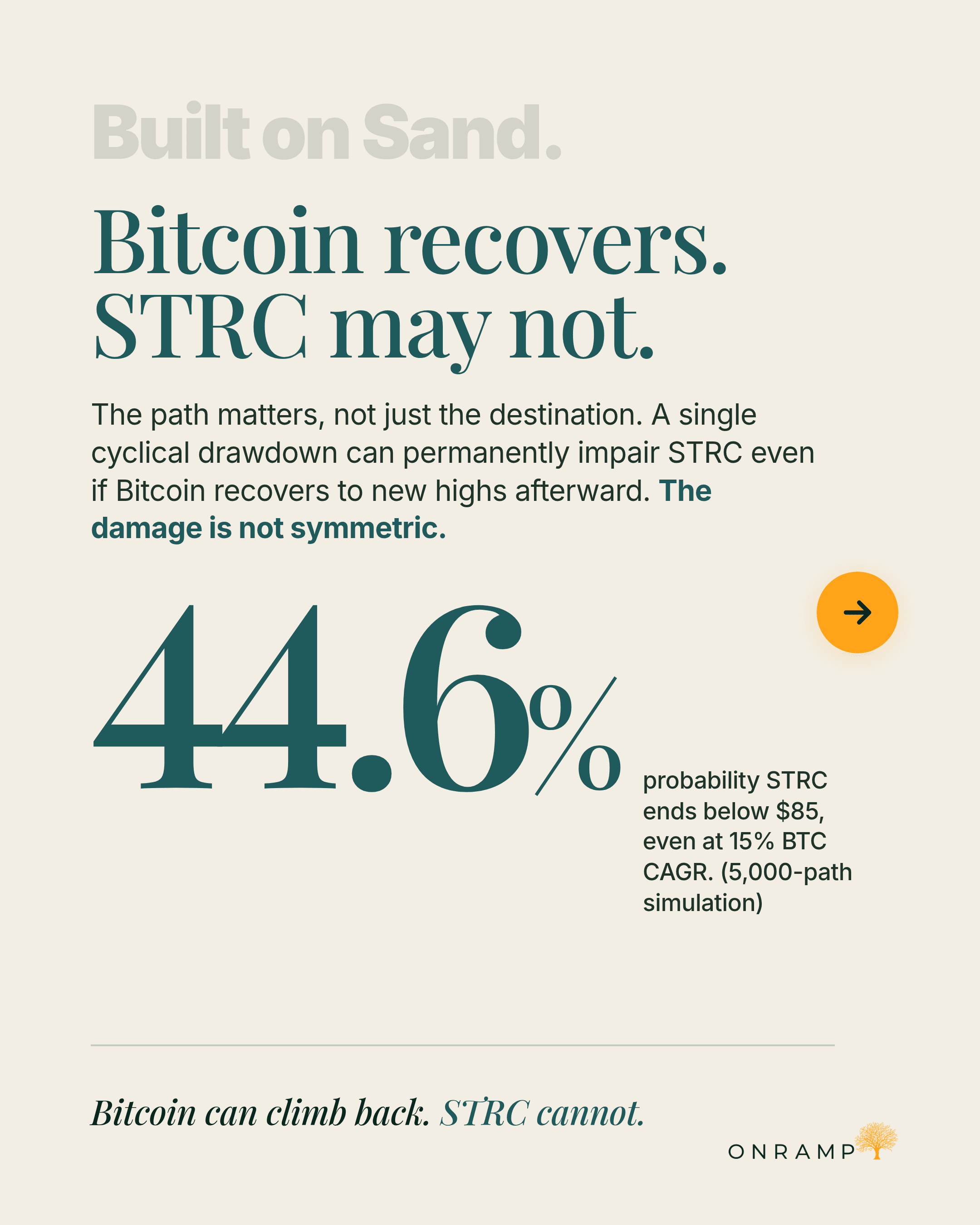

Layer 5: The Damage Path Is Asymmetric and Permanent

A bitcoin holder's terminal wealth depends on where bitcoin ends up. The path between here and there does not matter. A bitcoin held through a 70% drawdown that ends at a new all-time high is worth what bitcoin is worth at the end. The path is incidental.

An STRC holder's outcome is path-dependent. The same drawdown that bitcoin recovers from can permanently impair STRC. The structural mechanisms that protect the dividend in calm conditions become the structural mechanisms that consume the holder's principal in stress. A dividend ratchet. A forced bitcoin sale. A dividend deferral. Each is a defensive response that protects Strategy as the issuer at the cost of impairing the holder's claim.

Even on a bitcoin path that ends well, STRC may not. At a 15% bitcoin CAGR, a conservative long-run estimate, a structural credit model calibrated to Strategy's current capital structure produces roughly a 45% probability that STRC's terminal price ends below $85, an 18% probability of at least one year of dividend deferral, and a 46% probability of at least one forced bitcoin sale during the cycle.

The bitcoin holder absorbs the volatility and recovers. The STRC holder absorbs the volatility through the issuer's balance sheet and may not recover at all. The damage is not symmetric between asset and wrapper. And it is not symmetric between the recovery path bitcoin takes and the recovery path STRC is structurally capable of.

What Is Actually Being Sold

Bitcoin's value as outside money is a separate asset from its price exposure, and arguably the more important one. Outside money sits outside the financial system. Holding it gives the holder portability across jurisdictions, resistance to seizure, independence from the banking system, and the ability to self-settle without permission. These properties have monetary value. They are why central banks are accumulating gold. They are why bitcoin exists.

Converting spot bitcoin into STRC caps the holder's upside at the dividend rate, removes the asset's bearer property, and replaces it with a claim settled through the legal system of a single jurisdiction, dependent on the performance of multiple custodians, the solvency of the issuer, and the continued cooperation of capital markets. None of these dependencies existed in the spot position. All of them have been introduced in exchange for an income stream that surrenders every dollar of appreciation above 11.5%.

The holder takes on bitcoin's downside through the issuer's balance sheet, gives up bitcoin's upside above the coupon, and loses the optionality entirely. STRC carries the counterparty risk of a bank, the custody risk of an exchange, and the opacity of a hedge fund, attached to an asset whose entire purpose was the elimination of all three.

The Foundation Has Not Been Tested

The skyscraper has held. STRC has traded around par for most of its short life. The dividend has been paid. The at-the-market issuance has cleared. The capital structure has held.

The conditions that would test the foundation have not arrived. The custodians have not had a bad day. The capital markets have remained open. The dividend has not been deferred. None of the stress vectors that would surface the structure's actual weight-bearing capacity have shown up at once.

When they do, and history suggests they will, the questions that have been deferred will be answered swiftly, and they will be answered for the entire wrapper complex at once. STRC, the DATs, and the spot ETFs all sit on the same foundation. What breaks one breaks all of them.

The right move was always the same. Hold the asset directly. Real custody. Distributed keys arranged so that no single failure can compromise the holding. The asset does the work.

The wrapper, in every iteration the industry has produced, does not improve on the asset. In its most aggressive iterations, it actively degrades what the asset was built to be.

Full structural and credit analysis publishing this week.