The New Money Stack: The Institutional Digital Asset Infrastructure Map

Glenn Cameron | Global Head, Onramp Institutional

Published March 2026 | Onramp Research

The financial system is being rebuilt layer by layer. Settlement, custody, compliance, payments, asset management, and every layer in between now has a digital-native alternative that is faster, cheaper, and more transparent than the legacy infrastructure it replaces. But for institutional allocators, the landscape remains fragmented, fast-moving, and difficult to navigate.

The New Money Stack documents the full institutional digital asset infrastructure as it exists in March 2026. Ten layers. From the base settlement network to the regulatory framework being constructed around it. For each layer, the report identifies the key players, the market data, the competitive dynamics, and the structural shifts that matter for capital allocators.

It is written for CIOs, family offices, RIAs, and institutional decision-makers who need to understand what already exists, who is building it, and where the gaps remain.

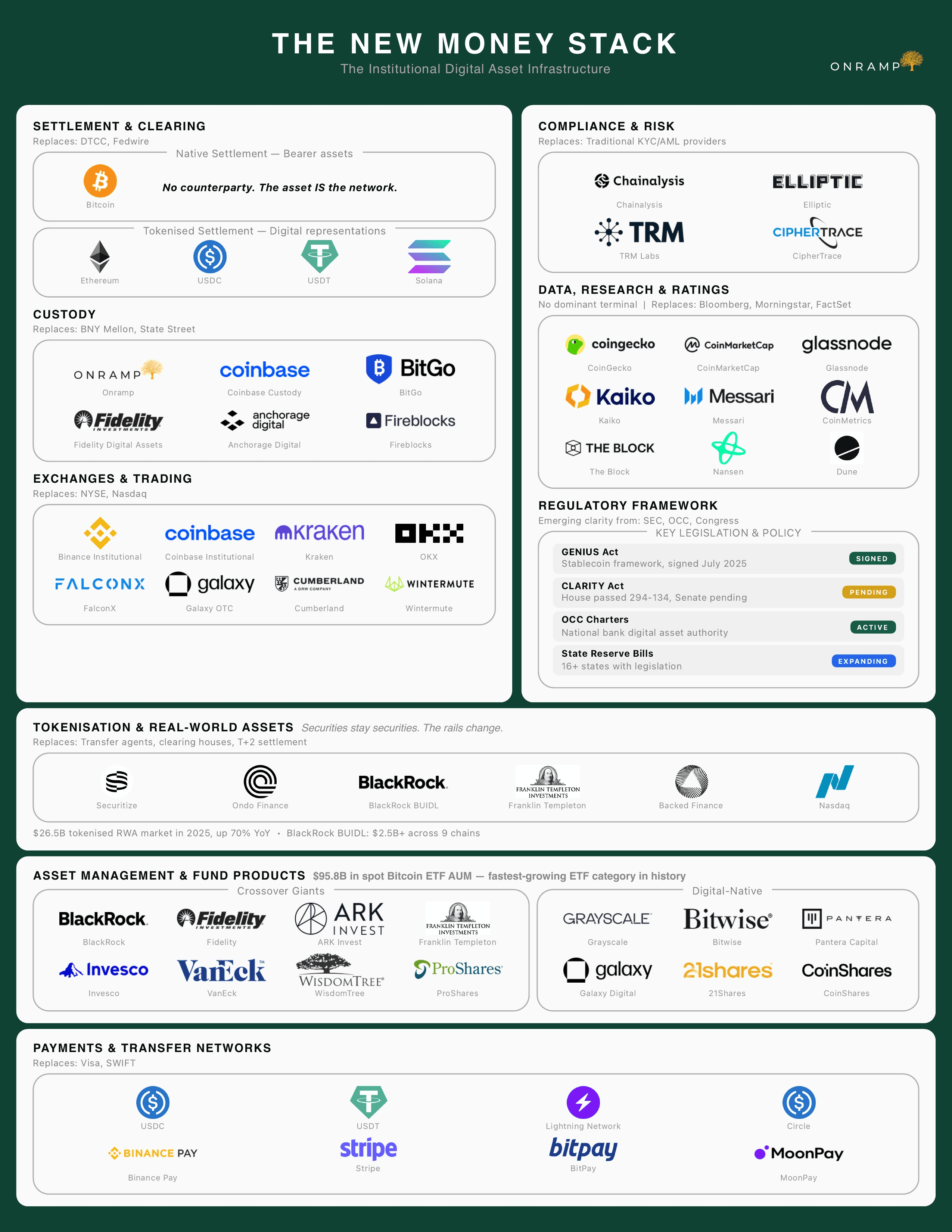

Settlement and Clearing

Bitcoin settled approximately $28 trillion on an annualized basis in 2025, matching the combined volume of Visa and Mastercard. Settlement is final in minutes rather than the T+1 or T+2 of traditional rails. The network has never experienced downtime.

Stablecoins settled $33 trillion in total volume during 2025, growing 72% year over year. USDC processed $18.3 trillion and USDT processed $13.3 trillion. Stablecoin market capitalization reached $306 billion by year end.

The report draws a critical architectural distinction between native settlement (bearer assets where the asset and the network are the same thing) and tokenized settlement (digital representations that carry counterparty risk by design).

Custody

Digital asset custody now offers more architectural diversity than traditional custody. The report compares three models head to head.

Multi-Institution Custody (MIC) distributes private keys across multiple independent institutions. No single entity can move funds unilaterally. Onramp is the provider in this category. Multi-Party Computation (MPC) splits a single key into encrypted shares across servers, offering speed and flexibility but introducing single-vendor risk. Fireblocks and Anchorage are the primary MPC providers. Hardware Security Module (HSM) custody stores keys in tamper-resistant hardware, a battle-tested approach used by BitGo, Fidelity, and Coinbase.

Coinbase custodies Bitcoin for 8 of 11 spot Bitcoin ETFs, creating concentration risk the market has not yet fully priced. BitGo received OCC approval as a national trust bank in December 2025.

Exchanges and Trading

Centralized exchanges processed $86.2 trillion in perpetual trading volume in 2025. Institutional Bitcoin spreads have narrowed from 50 to 80 basis points in 2022 to under 5 basis points on major venues. Decentralized perpetual exchanges grew 346%, reaching $6.7 trillion. Hyperliquid, a decentralized exchange, now ranks in the top 10 globally by perpetual volume.

Asset Management and Fund Products

Spot Bitcoin ETFs hold $95.8 billion in assets under management across 12 competing products, making this the fastest-growing ETF category in history. BlackRock's IBIT alone holds $70.6 billion, representing 73.7% of total AUM. Fee compression is already underway, with products ranging from 0.15% to 0.25%.

Tokenization and Real-World Assets

The tokenized real-world asset market reached $26.5 billion in 2025, growing 70% year over year. BlackRock's BUIDL tokenized Treasury fund surpassed $2.5 billion across nine blockchains. Securitize operates as both an SEC-registered broker-dealer and transfer agent, tokenizing for BlackRock, Apollo, Hamilton Lane, and KKR. Nasdaq has filed with the SEC to trade tokenized securities alongside traditional stocks.

Ninety percent of tokenized value is concentrated in US Treasuries and private credit. The asset classes that institutional allocators already understand are moving on-chain first.

Payments and Transfer Networks

Stablecoin volume in 2025 roughly doubled Visa's annual volume. B2B stablecoin payments surged 733% year over year, with Asia accounting for 60% of flows. The report identifies a critical emerging dynamic: AI agents require payment rails that operate without human identity, merchant accounts, or traditional KYC. Three competing fiat protocols have launched (OpenAI, Google, Mastercard), all requiring human identity. The Lightning Network does not.

Compliance and Risk

Blockchain analytics has grown into a $6 billion-plus industry that did not exist eight years ago. Chainalysis provides analytics to over 100 government agencies and 500-plus private sector clients. The compliance tooling available for on-chain transactions now exceeds what exists for traditional wire transfers, where senders, receivers, and intermediary banks often operate in opacity.

Data, Research, and Ratings

This is the single biggest infrastructure gap in the stack. Traditional finance has Bloomberg as a single source of truth. Digital assets have 80-plus fragmented providers, no standardized ratings framework, and no institutional-grade terminal that aggregates everything. The report profiles Glassnode, Kaiko, CoinMetrics, Messari, Nansen, and Artemis across institutional readiness, API access, and pricing.

Regulatory Framework

On March 17, 2026, the SEC and CFTC jointly established a formal token taxonomy for the first time in either agency's history. Five categories were created: Digital Commodities (CFTC), Digital Collectibles (neither agency), Digital Tools (neither agency), Payment Stablecoins (OCC and state regulators), and Digital Securities (SEC). Only one of the five categories falls under SEC securities regulation. The GENIUS Act was signed in July 2025 establishing the stablecoin framework. The CLARITY Act passed the House and remains pending in the Senate.

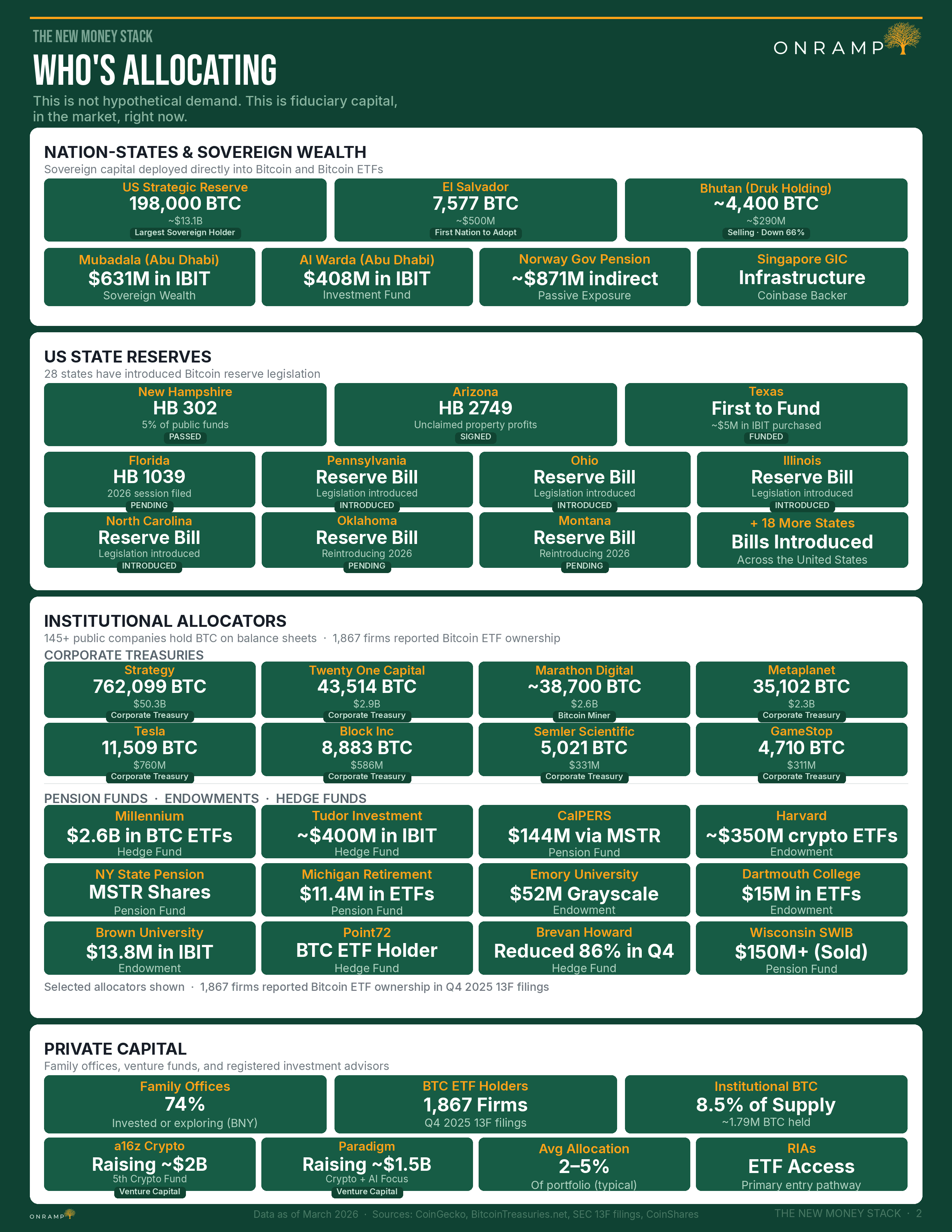

Who Is Allocating

The report documents fiduciary capital already deployed across every institutional category. The US Strategic Reserve holds 198,000 BTC (approximately $13.1 billion). El Salvador holds 7,577 BTC. Mubadala and Al Warda in Abu Dhabi hold over $1 billion combined in IBIT. Twenty-eight US states have introduced Bitcoin reserve legislation.

Strategy (formerly MicroStrategy) holds over 762,000 BTC. More than 145 public companies hold Bitcoin on their balance sheets. 1,867 firms reported Bitcoin ETF ownership in Q4 2025 13F filings. Pension funds including Wisconsin, CalPERS, Michigan, and the New York State Pension have taken positions. Harvard, Brown, Emory, and Dartmouth endowments have all allocated. Seventy-four percent of family offices are invested or exploring allocation.

Where the Value Settles

The report concludes with a structural argument. The infrastructure is real. Every layer is being rebuilt on faster, cheaper, more transparent rails. But infrastructure is plumbing. Value flows through plumbing. It does not rest there.

There is exactly one layer in the entire stack where the asset and the network are the same thing. Where there is no counterparty, no issuer, no registrar, and no one who can change the rules. Where supply is fixed by mathematics, not by committee. That layer is Bitcoin.

Upcoming Research in This Series

This report is the first in a series from Onramp Research. Upcoming publications include the Custody Architecture Map (MIC vs MPC vs HSM), AI Commerce Payment Rails, the Stablecoin Stack (GENIUS Act Edition), the Bitcoin ETF and Asset Manager Universe (Q1 2026 13F analysis), the Allocator Map, and the State and Sovereign Bitcoin Reserve Tracker.