The Simpler Trade: Digital Credit Risk Analysis

Glenn Cameron | Global Head, Onramp Institutional

Why a Treasury Income Ladder + Direct Bitcoin Ownership Beats Digital Credit on Every Metric That Matters

Strategy's STRC is a $10.7 billion perpetual preferred stock marketed as money-market-like and backed by bitcoin. 82.7% of it is held by retail. The Simpler Trade is Onramp's structural and credit risk analysis of the instrument and the broader Digital Credit category, with the bitcoin and Treasury alternative that outperforms STRC on every metric.

The 77-page analysis covers the capital structure of Strategy's STRC, the dividend ratchet mechanism, the credit model methodology and its 5,000-path simulation outputs, the path-dependency math that makes STRC permanently impairable even on bitcoin paths that recover, and the 20/80 bitcoin and Treasury alternative that delivers more income, more terminal wealth, and zero counterparty risk on the same underlying bitcoin path.

Key findings:

STRC's structural risks scale inversely with bitcoin's performance. At a 10% bitcoin CAGR, the credit model produces a 12.3% probability of formal default, a 21.9% probability of dividend deferral, and a 50.7% probability of at least one forced bitcoin sale during the 8-year cycle. The same scenarios are structurally unremarkable for direct bitcoin holders. STRC is most fragile in exactly the bitcoin paths the asset itself absorbs without consequence.

The damage from a single cyclical drawdown is asymmetric and may not reverse. At a 15% bitcoin CAGR, STRC has a 44.6% probability of ending below $85 even on bitcoin paths that recover to new highs. A bitcoin holder's terminal wealth depends only on where the asset ends up. An STRC holder's outcome is path-dependent, because the structural mechanisms that protect the dividend in calm conditions become the mechanisms that consume the holder's principal in stress.

The dividend is funded by issuing new shares, not earnings. Strategy's software business produces approximately $477 million in annual revenue against total preferred dividend obligations now exceeding $1.2 billion. The dividend ratchet has embedded $268 million in permanent annual obligations after seven monthly increases from 9% to 11.5%, and the rate has only ever moved in one direction. The funding channel only functions while STRC trades above par.

The institutional buyer the marketing names cannot exist as both informed and rational. Insurance mandates, pension liability matching, and yield-starved fixed-income desks cannot underwrite the credit profile of an unsecured perpetual preferred layered on a bitcoin treasury without structurally understanding bitcoin first. Any institution that does the work allocates to spot bitcoin instead. The buyer that does exist, in the cap table, is 82.7% retail.

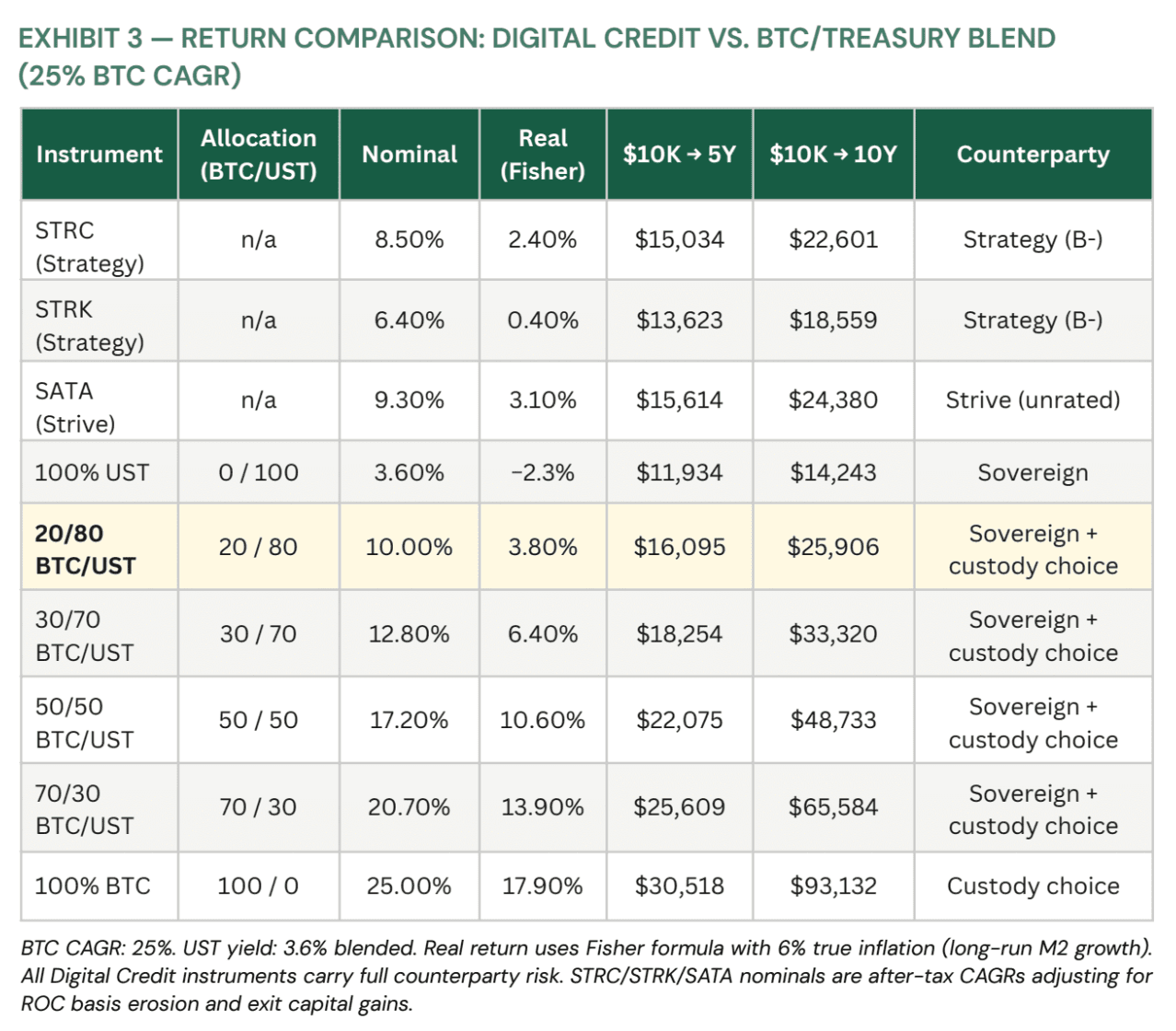

The simpler trade beats STRC more frequently as bitcoin compounds faster. Across 5,000 simulated paths at 25% CAGR, the 20/80 portfolio of bitcoin and Treasuries wins 64.4% of the time. Across the full range of tested scenarios, the win-rate moves from 48.6% at 10% CAGR to 69.7% at 30%, while STRC's structural stress probabilities move in the opposite direction.

The executive brief gives you the high-level case in 17 pages. The full report gives you the methodology, the stress walkthrough, and the steelman section engaging with the strongest STRC defenses.

"STRC carries the counterparty risk of a bank, the custody risk of an exchange, and the opacity of a hedge fund, attached to an asset whose entire purpose was the elimination of all three." — From 'Built on Sand'